March 31, 2025

The Spring Market may be the busiest time of the year for housing, but this spring is the most advantageous buying season for house hunters in years.

The 2025 Spring Market

More homes come on the market during the spring than at any other time of the year, inventory rises, demand peaks, and market time climbs.

Spring has arrived. The days are growing longer, birds are happily chirping, temperatures are rising, and trees that lost all their leaves are blanketed with buds of new life. The official first day of spring was Friday, March 20th. It was also the beginning of housing’s Spring Market, the busiest season for real estate.

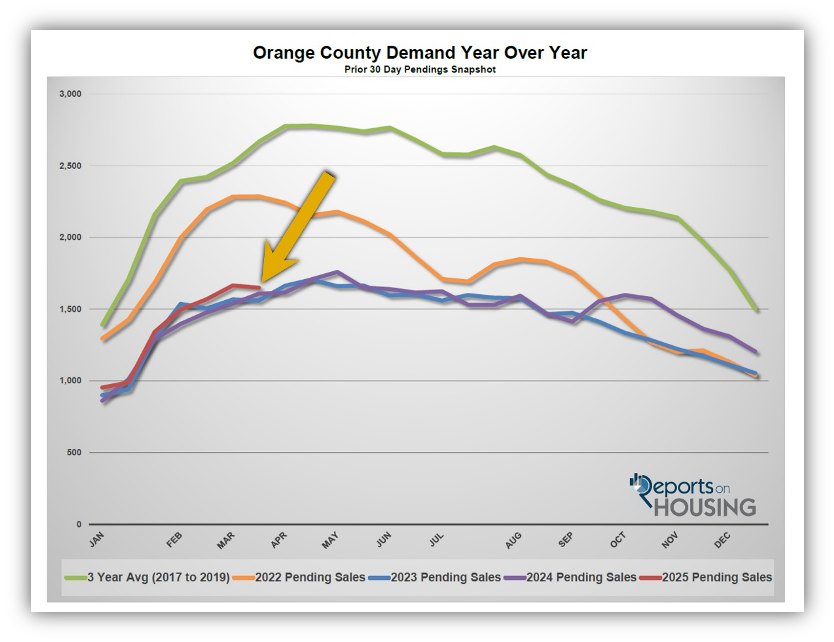

The Spring Market runs from mid-March through May. It is still the Winter Market in early March, which runs from mid-January to mid-March. That is when the inventory does not change much, buyer demand surges onto the scene and rockets higher, and the market speed accelerates rapidly. It sets up the Spring Market. Spring is characterized by a steadily rising inventory, buyer demand that slowly grows, peaks between April and May, and then slowly falls, and the Expected Market Time, the market speed, slowly rises.

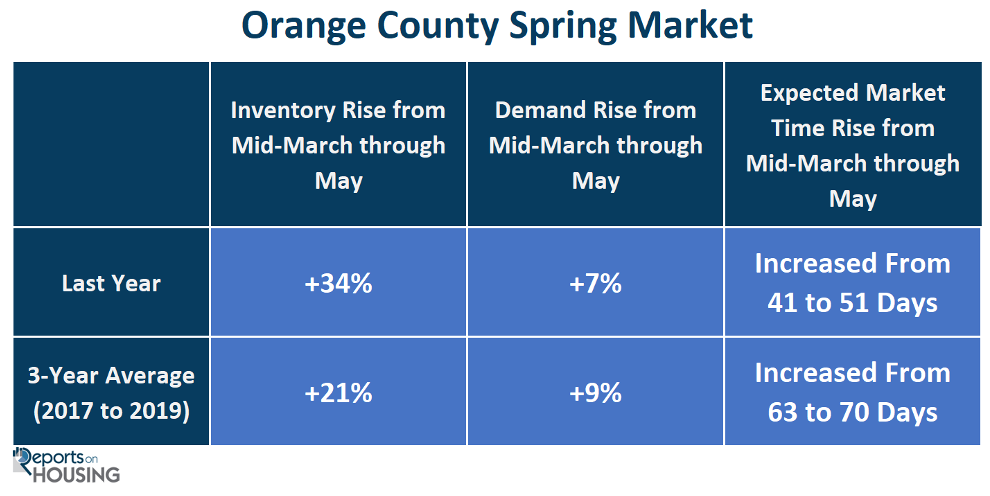

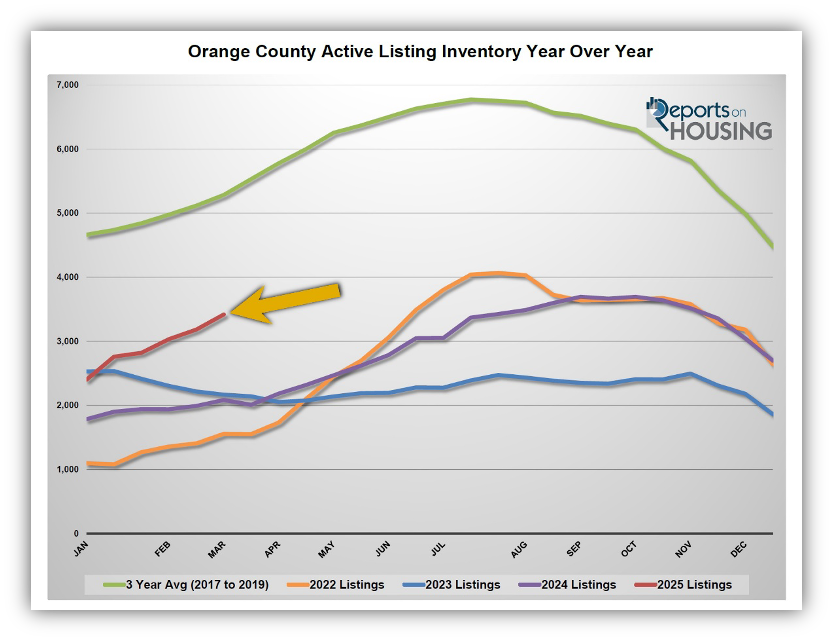

Looking at the 10-year average from 2015 to 2024, an elevated number of homes are placed on the market from March through August. The peak month is May. As a result, the inventory methodically climbs. Due to the high mortgage rate environment, many homeowners have opted to “hunker down” in their homes, unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. Yet, that phenomenon has been slowly fading. So far in 2025, there have been 20% more FOR SALE signs this year than last year, and 42% more than in 2023. These extra homes have accumulated over time, allowing the active inventory to grow in 2024 and 2025. Last year, the inventory expanded from 2,084 in March to 2,786 by the end of spring, up 34% or 702 homes. The 3-year pre-pandemic average (2017 to 2019) grew from 5,286 to 6,370, up 21% or 1,084. This year’s spring inventory started at 3,419, a substantial 64% higher than last year, yet still 35% lower than before COVID.

Demand (a snapshot of the number of new pending sales over the prior month) has accelerated since mid-January. It slowly rises, peaks, and then slowly falls during the spring. Last year, from mid-March through May, it increased by 7% or 102 pending sales, growing from 1,538 to 1,640. The 3-year pre-pandemic average climbed from 2,517 pending sales to 2,738, up 9% or 221. Demand this year started at 1,665 pending sales, 8% higher than last year, but 34% less than before COVID.

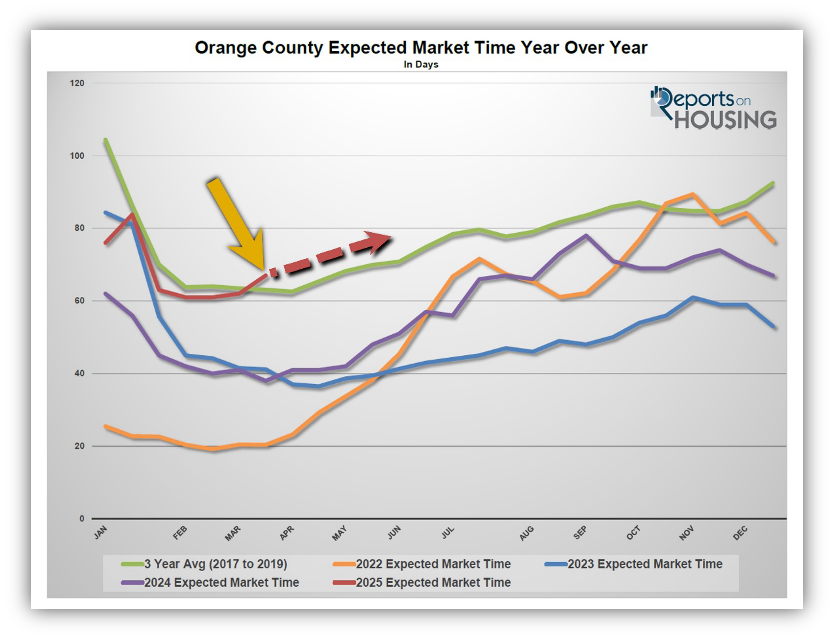

The Expected Market Time (the number of days it takes to sell all Orange County listings at the current buying pace) is based on supply and demand (the active inventory and recent pending sales activity). After dropping to its lowest, fastest level, typically at the start of spring, the market slows slightly from week to week. Last year during the Spring Market, the Expected Market Time decelerated from 41 to 51 days. During the 3-year pre-COVID average, the housing market slowed from 63 to 70 days. This spring started with an Expected Market Time of 62 days.

A 62-day Expected Market Time is the slowest pace since 2019. The slower speed is precisely why in 2025 it is a “buyer’s spring.” Some homes still procure multiple offers and sell nearly instantly, but that is not the case for the housing market as a whole. It depends on the area, the price range, pricing accuracy, condition, location, and amenities. Many homes have been sitting on the market without success. A revealing 50% of the active listing inventory has been on the market for at least one month, and 27% has been sitting for at least two months. Many sellers have been a bit overzealous in pricing their homes. Surprisingly, 30% of all active listings have reduced the asking price at least once. This is relatively high for a market that just transitioned to the Spring Market.

If the inventory grows at the same pace as last year, up 34%, it would climb from 3,419 homes to 4,517. That would be the highest level since 2020, when it finished the spring at 5,044 homes. And, if demand rises by 9% like last year, it would increase from 1,665 pending sales to 1,775, remaining at muted levels similar to the past couple of years due to the high interest rate environment and affordability constraints. That would result in the Expected Market Time increasing from 62 to 77 days, adding 15 days and the slowest pace since 2019’s 85 days to end the spring.

While spring is the busiest time of the year in terms of pending sales volume, the most buyer activity of the year, it is also when more sellers surge onto the scene. As a result, the market slows from week to week. The best time of the year for sellers is suddenly in the rearview mirror. Those homeowners who wait until later in the year, or the sellers who languish on the market due to improper pricing, will be confronted with more seller competition and longer market times. Housing is not as instant as the past several years. Finally, buyers are in a much better position. It is a buyer’s spring.

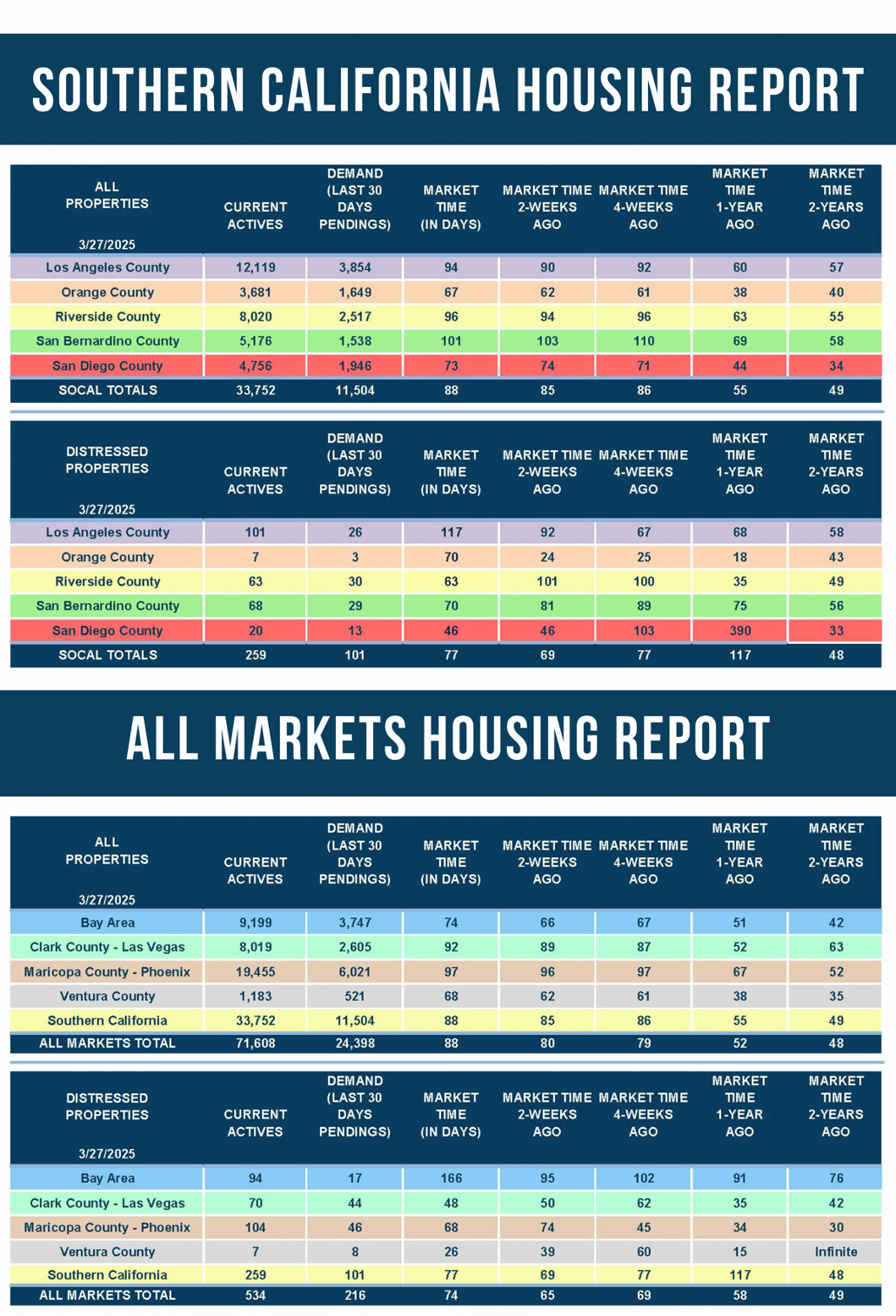

Active Listings

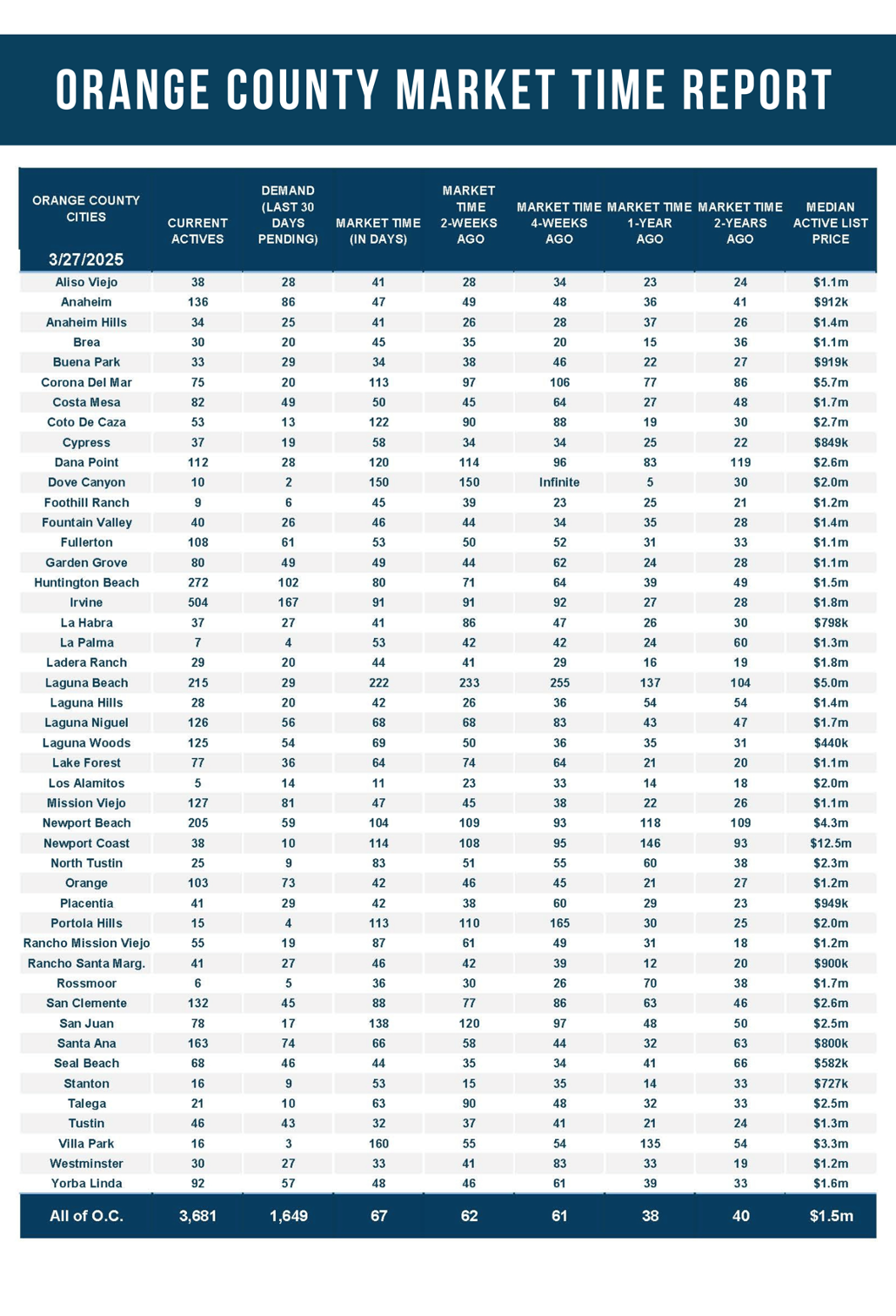

The inventory grew by 8% in the past couple of weeks.

The active listing inventory increased by 262 homes in the past two weeks, up 8%, and now sits at 3,681, its largest rise since mid-January. This is the highest level since last year’s September peak at 3,695 homes. The inventory has risen by 1,280 homes this year, up 53%. That is the largest rise since 2010 when it climbed by 1,618. Last year it grew from 1,785 to 2,010, up only 225 or 13%. With an elevated number of homes coming on the market from March through August, the inventory will continue to rapidly climb throughout the Spring and Summer Markets.

Last year, the inventory was at 2,010 homes, 45% lower, or 1,671 fewer. The 3-year average before COVID (2017 through 2019) was 5,533, an additional 1,852 homes, or 50% more.

Homeowners continue to “hunker down” in their homes, unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. It became a crisis once rates skyrocketed in 2022. For February, 2,459 new sellers entered the market in Orange County, 673 fewer than the 3-year average before COVID (2017 to 2019), 21% less. Last February, there were 2,065 new sellers, 16% fewer than this year. More sellers are opting to sell compared to the previous couple of years.

Demand

Demand dropped by 16 pending sales in the past couple of weeks.

Demand, a snapshot of the number of new pending sales over the prior month, decreased from 1,665 to 1,649 in the past couple of weeks, down 16 pending sales, or 1%, its first drop of the year. With the Spring Market and much more daylight, demand will slowly rise until it peaks between April and May. After peaking, demand will remain elevated but slowly fall during the Spring and Summer Markets. Mortgage rates have bounced around 6.75% for over four weeks, according to Mortgage News Daily. Last year, it bounced around 7% in February and March and then eclipsed 7.5% a few times in April. This year’s lower mortgage rates should translate to a slightly elevated number of pending and closed sales. The market will accelerate even more if rates drop below 6.5% with duration. This would occur if the U.S. economy slows further in the coming months.

As the Federal Reserve has indicated, watching all economic releases for signs of slowing is essential. That is the only path to lower mortgage rates right now. These releases can move mortgage rates higher or lower, depending on how they compare to market expectations. This week is jobs week, with the number of job openings released on Tuesday, and wages and the number of jobs created or lost released on Friday. This is one of the month’s most important economic data points. Next week is the release of the Consumer Price Index (CPI) and the Producer Price Index (PPI), two crucial inflation indicators. It will be a pivotal two weeks for mortgage rates.

Last year, demand was 1,617, with 32 fewer pending sales or 2% less. The 3-year average before COVID (2017 to 2019) was 2,668 pending sales, 62% more than today, or an additional 1,019.

With supply surging and demand dropping slightly, the Expected Market Time (the number of days it takes to sell all Orange County listings at the current buying pace) increased from 62 to 67 days in the past couple of weeks, its slowest reading since mid-January. Last year, it was 37 days, substantially faster than today. The 3-year average before COVID was 63 days, similar to today.

Luxury End

The luxury market slowed in the past couple of weeks.

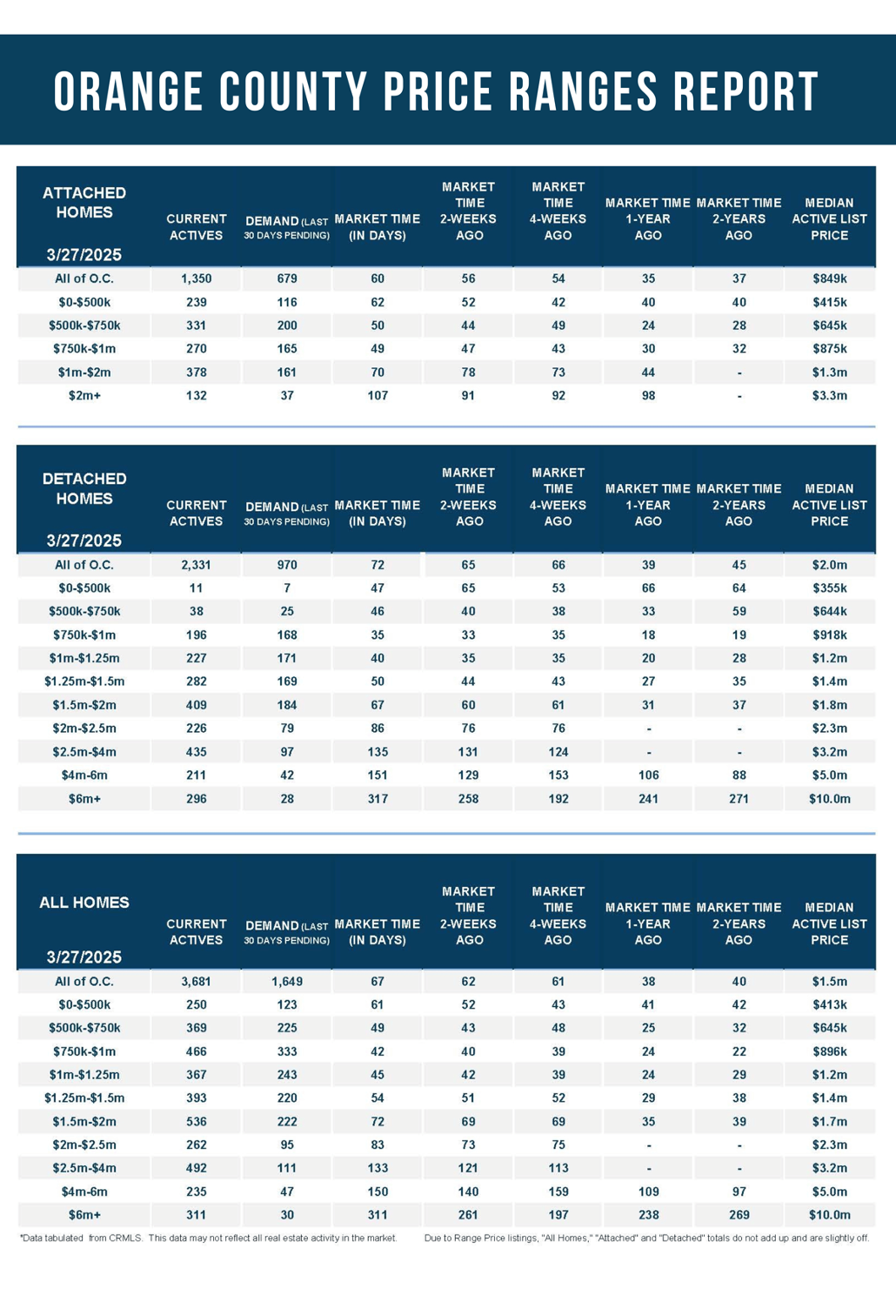

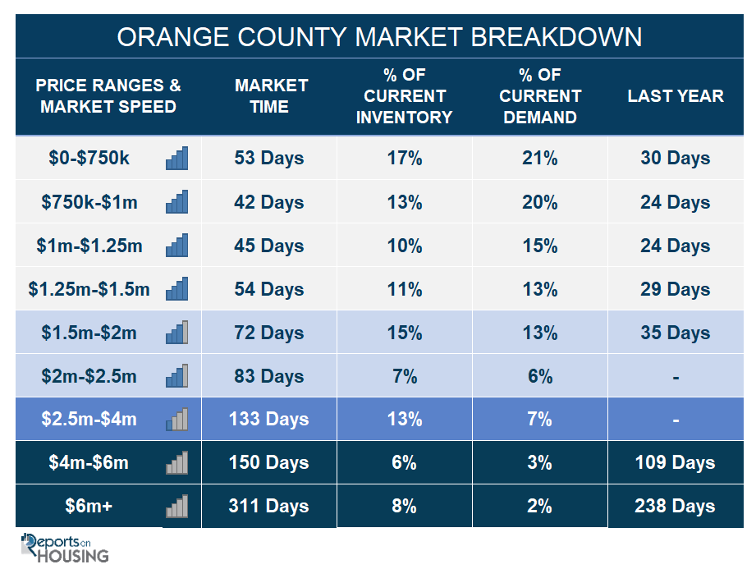

The luxury inventory of homes priced above $2.5 million (the top 10% of the Orange County housing market) increased from 978 to 1,038 homes, up 60 or 6%. Luxury demand decreased by eight pending sales, down 4%, and now sits at 188. The Expected Market Time for luxury homes priced above $2.5 million jumped from 150 to 166 days. Wall Street’s continued volatility is starting to impact Orange County’s luxury market. Four weeks ago, it was 141 days, 25 days faster than today.

In the past two weeks, the Expected Market Time for homes priced between $2.5 million and $4 million increased from 121 to 133 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 140 to 150 days. For homes priced above $6 million, the Expected Market Time increased from 261 to 311 days. At 311 days, a seller would be looking at placing their home into escrow around February 2026.

Orange County Housing Summary

- The active listing inventory in the past couple of weeks increased by 262 homes, up 8%, and now sits at 3,681. In February, 21% fewer homes came on the market compared to the 3-year average before COVID (2017 to 2019), 673 less. Yet 394 more sellers came on the market this February compared to February 2024. Last year, there were 2,010 homes on the market, 1,671 fewer homes, or 45% less. The 3-year average before COVID (2017 to 2019) was 5,533, or 50% extra.

- Demand, the number of pending sales over the prior month, decreased by 16 pending sales in the past two weeks, down 1%, and now totals 1,649, its first drop of the year. Last year, there were 1,617 pending sales, 2% less. The 3-year average before COVID (2017 to 2019) was 2,668, or 62% more.

- With supply surging higher and demand down slightly, the Expected Market Time, the number of days to sell all Orange County listings at the current buying pace, climbed from 62 to 67 days in the past couple of weeks, its slowest pace since mid-January. Last year, it was 37 days, substantially faster than today. The 3-year average before COVID (2017 to 2019) was 63 days, similar to today.

- In the past two weeks, the Expected Market Time for homes priced below $750,000 remained increased from 46 to 53 days. This range represents 17% of the active inventory and 21% of demand.

- The Expected Market Time for homes priced between $750,000 and $1 million increased from 40 to 42 days. This range represents 13% of the active inventory and 20% of demand.

- The Expected Market Time for homes priced between $1 million and $1.25 million increased from 42 to 45 days. This range represents 10% of the active inventory and 15% of demand.

- The Expected Market Time for homes priced between $1.25 million and $1.5 million increased from 51 to 54 days. This range represents 11% of the active inventory and 13% of demand.

- The Expected Market Time for homes priced between $1.5 million and $2 million increased from 69 to 72 days. This range represents 15% of the active inventory and 13% of demand.

- The Expected Market Time for homes priced between $2 million and $2.5 million increased from 73 to 83 days. This range represents 7% of the active inventory and 6% of demand.

- In the past two weeks, the Expected Market Time for homes priced between $2.5 million and $4 million increased from 121 to 133 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 140 to 150 days. For homes priced above $6 million, the Expected Market Time increased from 261 to 311 days.

- The luxury end, all homes above $2 million, accounts for 27% of the inventory and 12% of demand.

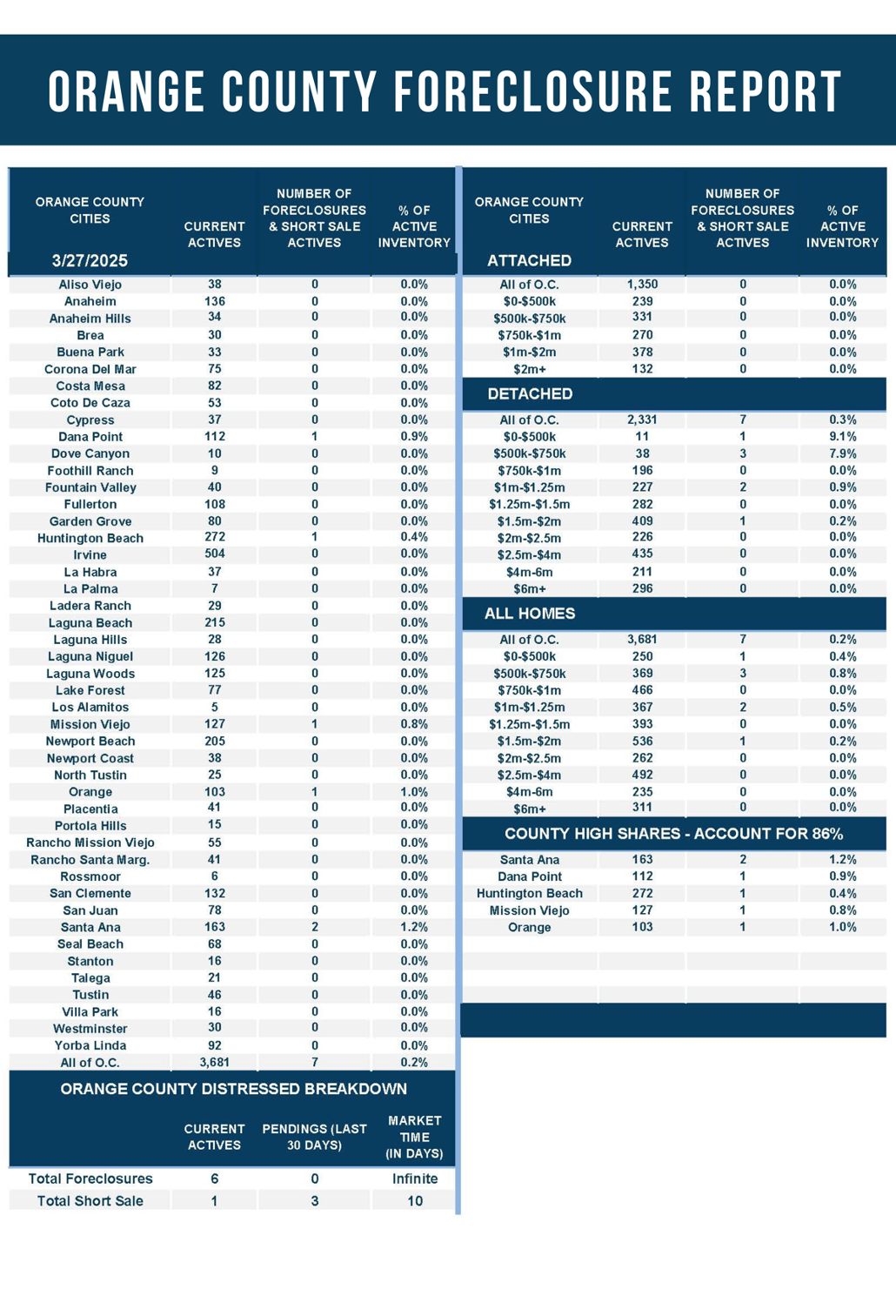

- Distressed homes, both short sales and foreclosures combined, comprised only 0.2% of all listings and 0.4% of demand. Only three foreclosures and two short sales are available today in Orange County, with five total distressed homes on the active market, up one from two weeks ago. Last year, six distressed homes were on the market, similar to today.

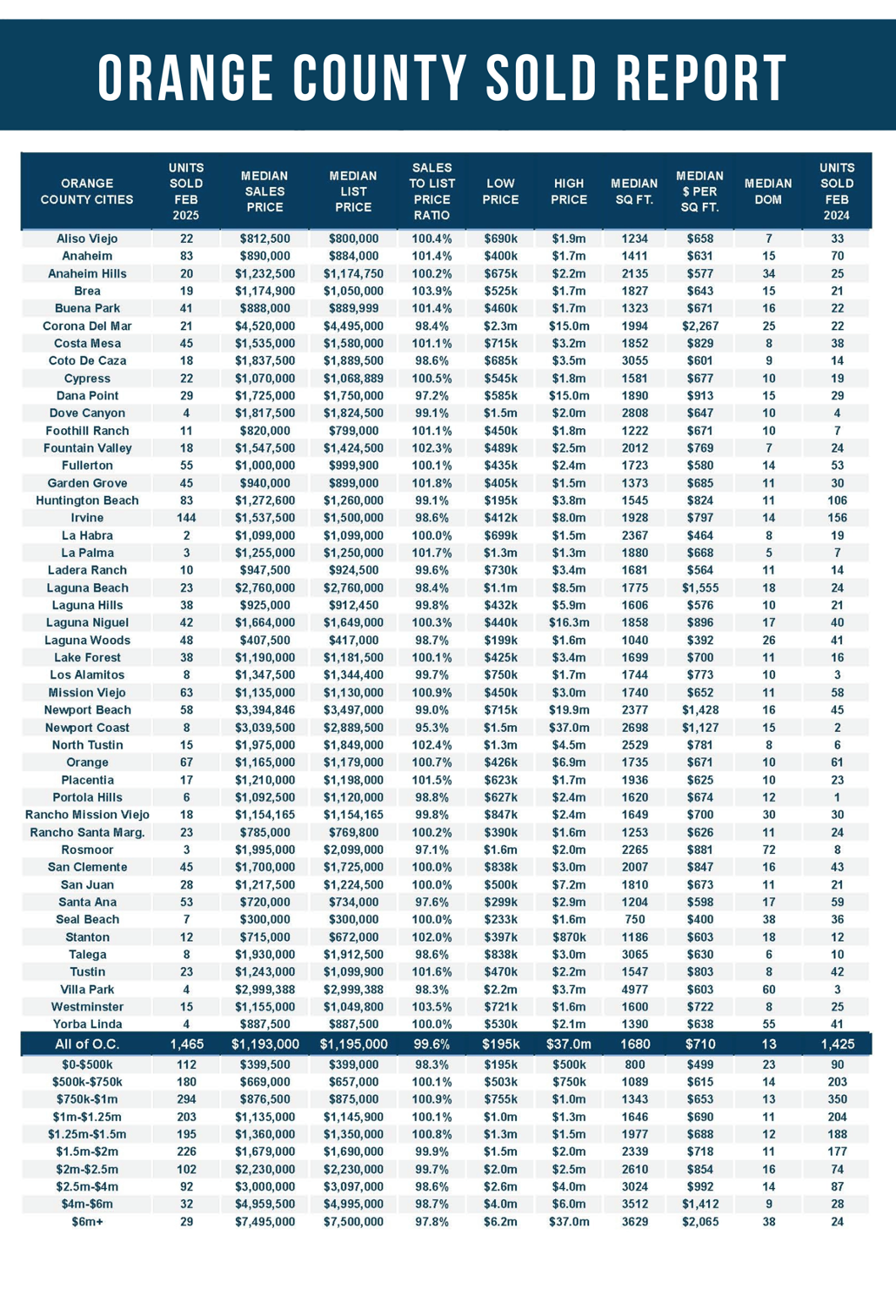

- There were 1,465 closed residential resales in February, up 3% compared to February 2024’s 1,425 and up 16% from January 2025. The sales-to-list price ratio was 99.6% for Orange County. Foreclosures accounted for 0.1% of all closed sales, and Short sales accounted for 0.3%. That means that 99.6% of all sales were good ol’ fashioned sellers with equity.

Have a great week.

Sincerely,

Steven Thomas

Quantitative Economics and Decision Sciences

Copyright 2025—Steven Thomas, Reports On Housing—All Rights Reserved. This report may not be reproduced in whole or in part without express written permission from the author.