April 1, 2024

Comparing today’s inventory and demand levels to prior years reveals the accurate temperature and trends of the current market.

Low Inventory and Demand

Even with low demand, the low inventory has paved the way for a very hot Spring Market.

In planning the day, there are plenty of weather apps and websites to try to figure out the temperature. Based on the information, it may be helpful to pack a jacket or wear shorts. Unfortunately, with all the technology, weather forecasting is not an exact science and often misses the temperature by a mile. It is better to look at a good old-fashioned outdoor thermometer, or the “outside temperature” reading in the car, to gauge the day’s weather accurately.

Similarly, there is no shortage of “economic experts” who look at housing data and attempt to measure the current temperature of the market. Yet, many of these experts are not “housing analysts” by trade and miss the temperature of housing by a mile, unfamiliar with the nuances in the data. Their economic expertise focuses on a different sector of the economy. To accurately determine housing’s strength and its actual temperature, it is best to turn to the data, inventory versus demand.

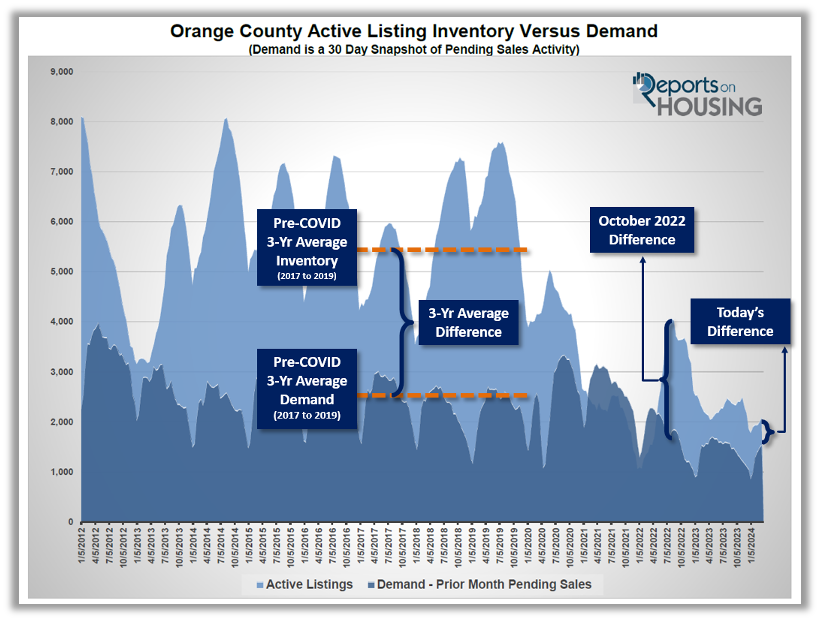

Ever since rates spiked higher in 2022, there has been a tug-of-war between two opposing forces: supply scarcity and an affordability crisis. The lack of homes available to sell favors sellers in the negotiation process, and home affordability dropping to historic lows favors buyers in the negotiation process. As rates spiked higher from 3.25% in January 2022 to eclipsing 7% in October 2022, the highest rate in over 20 years, demand came to a screeching halt, and the inventory climbed. The October 2022 inventory reached 3,677 homes, and demand, a snapshot of the number of new pending sales over the prior month, dropped to 1,270. The difference between supply and demand reached 2,407. In March 2022, when home values were rocketing higher, the inventory was at 1,552, and demand was at 2,286. Demand exceeded supply. From June 2020 through May 2022, the difference between supply and demand was either low or negative. This rare phenomenon resulted in massive home value appreciation for two years. That all ended once rates eclipsed 6% in June 2022 and continued its march higher.

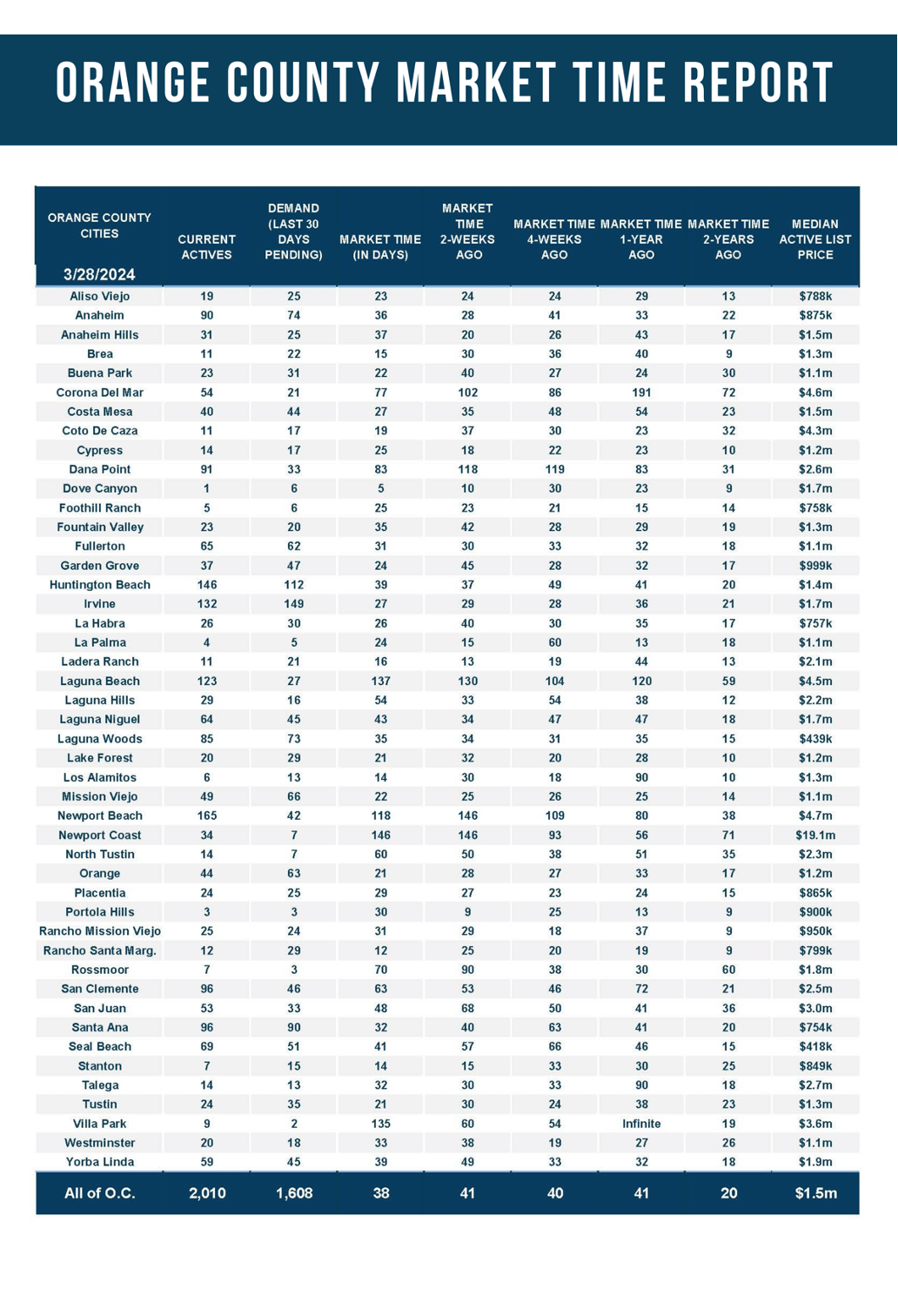

This year, mortgage rates have been bouncing between 6.6% and 7.1% with duration. Rate volatility has diminished dramatically since 2022. With less volatility, demand has risen despite today’s higher mortgage rate environment. Consequently, the difference between the active listing inventory and demand has narrowed. Today, the active inventory is 2,017 homes, demand is 1,617 pending sales, and the difference is only 400.

For a proper perspective, it is best to look at the 3-year average before COVID (2017 to 2019), when the pace of housing felt normal for both buyers and sellers. The 3-year average for active listings to start April was 5,533, and demand was 2,668. The difference was 2,865, considerably larger than today, seven times larger. There may have been a lot more demand back then, but there was also plenty of supply. To accurately determine the temperature of today’s market, matching the low inventory and low demand yields a scorching hot pace.

Today’s Expected Market Time (the number of days to sell all Orange County listings at the current buying pace) is 37 days. At 37 days, Orange County buyers are once again experiencing long lines of buyers at open houses, multiple offer situations, and sales prices above the asking price. This is not due to heightened demand. Unaffordability due to high mortgage rates is inhibiting demand. Instead, it is due to a chronically low inventory and very few available homes to purchase. The 3-year average Expected Market Time before COVID was 63 days, considerably higher than today, and home values rose annually.

Contributing to the low inventory is the lack of homeowners willing to sell, unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. So far this year, from January through March, 6,328 new sellers entered the market in Orange County, 3,376 fewer than the 3-year average before COVID of 10,094, 37% less.

For the housing market to tip in the favor of buyers, the speed of the housing market must cool considerably. Cooler temperatures can only be achieved with a sharp increase in the inventory, which last occurred in 2022 when rates initially surged higher. In 2024, rate volatility has subsided, demand has been climbing, and the inventory has only risen slightly (even falling by 3% in the past couple of weeks).

As long as the inventory level remains considerably lower than pre-COVID levels, housing will continue at its current pace with hot temperature readings.

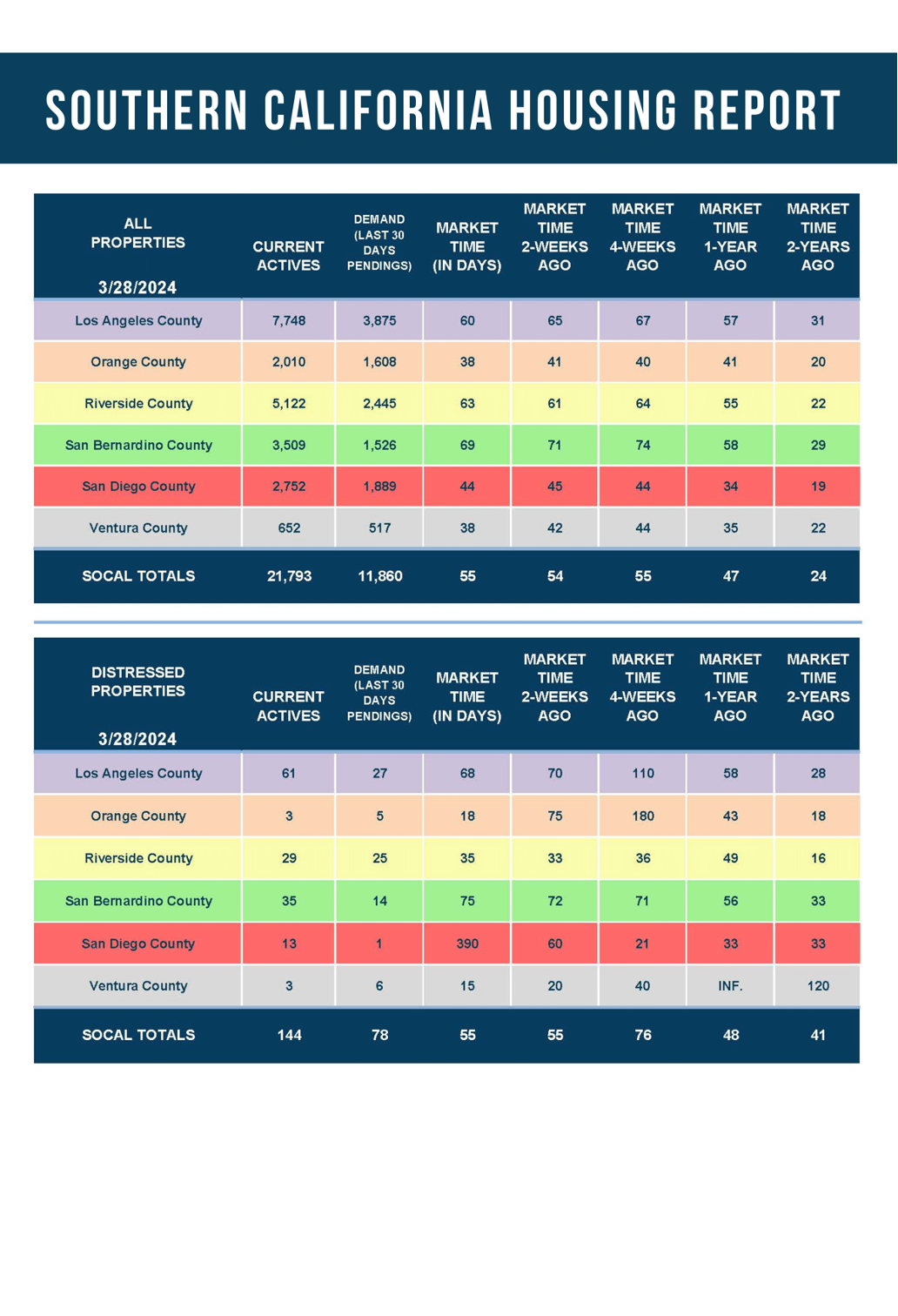

Active Listings

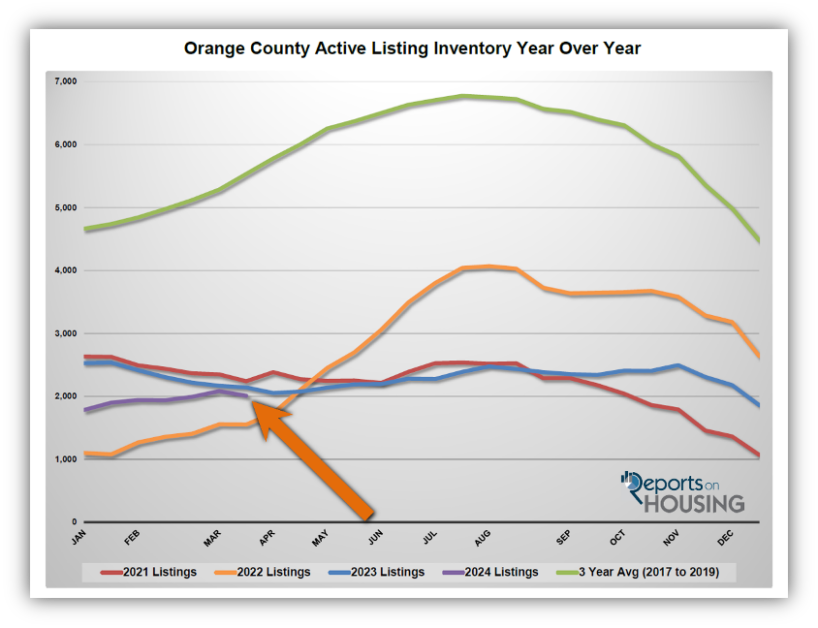

The active inventory decreased by 3% in the past couple of weeks.

The active listing inventory decreased by 67 homes in the past two weeks, down 3%, and now sits at 2,017. This is not a typical Spring Market when both supply and demand rise. Instead, even with rates bouncing around 7%, many buyers are tired of waiting for either prices to come down or rates to drop precipitously. The inventory continues to struggle to grow, partly due to increased buyer demand but also due to a lack of homeowners willing to sell. Too many homeowners opt to stay put and remain in their homes, enjoying their ultra-low, fixed-rate mortgage payments.

Last year, the inventory was 2,142 homes, 6% higher, or 125 more. The 3-year average before COVID (2017 through 2019) was 5,533, an additional 3,516 homes, or 174% extra, more than double where it stands today.

Homeowners continue to “hunker down” in their homes, unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. For March, 2,285 new sellers entered the market in Orange County, 1,623 fewer than the 3-year average before COVID (2017 to 2019), 42% less. Last March, there were 2,136 new sellers, 7% fewer than this year. A few more sellers are opting to sell compared to the previous year.

Demand

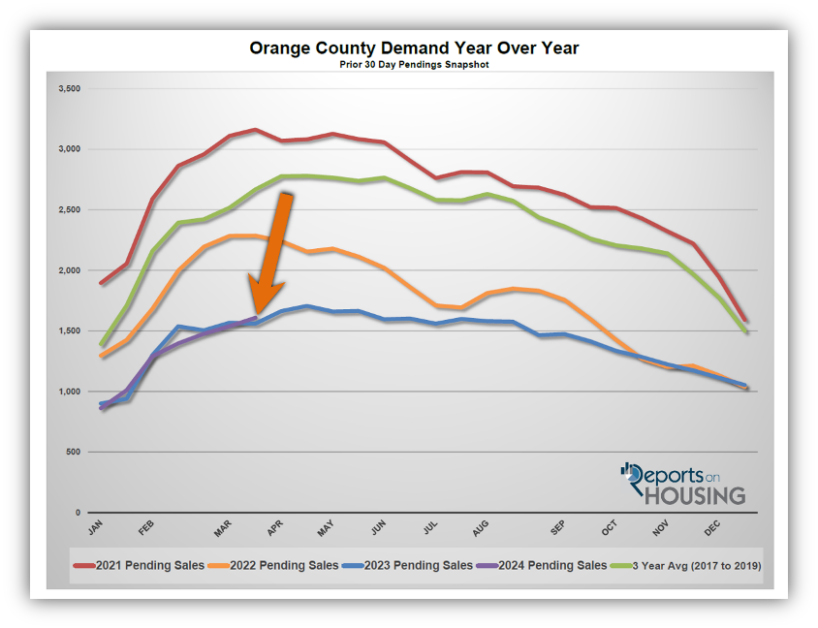

Demand increased by 5% in the past couple of weeks.

Demand, a snapshot of the number of new pending sales over the prior month, increased from 1,538 to 1,617 in the past couple of weeks, up 79 pending sales, or 5%, its highest level since May. Affordability is a real issue in today’s housing market and high mortgage rate environment. Demand is stuck at very low levels. Yet, in matching the small demand readings to the crumbs of available homes to purchase, the market feels extremely hot from the buyer’s perspective. If rates drop in the coming months, as forecasted by many economists, expect even more buyer competition and the market to become even hotter.

Last year, demand was 1,560, 4% less than today, or 57 fewer pending sales. The 3-year average before COVID (2017 to 2019) was 2,668 pending sales, 65% more than today, or an additional 1,051.

With supply falling and demand rising, the Expected Market Time (the number of days to sell all Orange County listings at the current buying pace) decreased from 41 to 37 days in the past couple of weeks, its hottest level since last April. Last year, the Expected Market Time was 41 days, similar to today. The 3-year average before COVID was 63 days, slower than today.

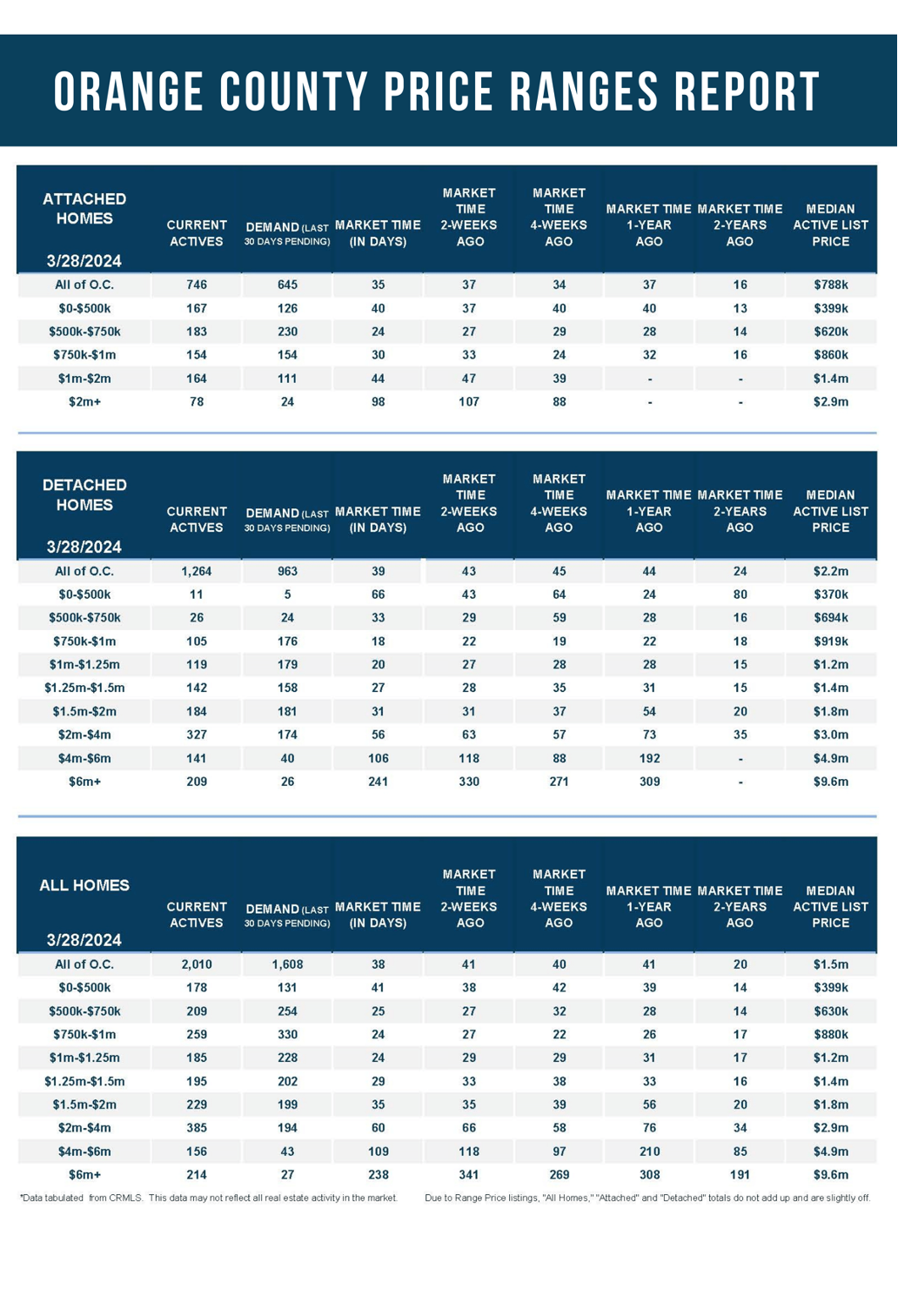

Luxury End

The luxury market improved in the past couple of weeks.

In the past couple of weeks, the luxury inventory of homes priced above $2 million decreased from 759 to 755 homes, down four, or 1%. Luxury demand increased by 29 pending sales, up 12%, and now sits at 264, the highest reading since May 2021. With inventory falling and demand rising, the Expected Market Time for luxury homes priced above $2 million decreased from 97 to 86 days. That is very hot for luxury. The strength of equity markets is fueling the strength of the luxury market.

Year over year, the active luxury inventory is up by 116 homes or 18%, and luxury demand is up by 95 pending sales or 56%. Last year’s Expected Market Time was 113 days, slower than today.

In the past two weeks, the expected market time for homes priced between $2 million and $4 million decreased from 66 to 60 days. For homes priced between $4 million and $6 million, the Expected Market Time decreased from 118 to 109 days. For homes priced above $6 million, the Expected Market Time decreased from 341 to 238 days. At 238 days, a seller would be looking at placing their home into escrow around November 2024.

Orange County Housing Summary

- The active listing inventory in the past couple of weeks decreased by 67 homes, down 3%, and now sits at 2,017. In March, 42% fewer homes came on the market compared to the 3-year average before COVID (2017 to 2019), 1,623 less. 149 more sellers came on the market this March compared to 2023. Last year, there were 2,142 homes on the market, 125 more homes, or 6% higher. The 3-year average before COVID (2017 to 2019) was 5,533, or 174% extra, more than double.

- Demand, the number of pending sales over the prior month, increased by 79 pending sales in the past two weeks, up 5%, and now totals 1,617. Last year, there were 1,560 pending sales, 4% fewer than today. The 3-year average before COVID (2017 to 2019) was 2,668, or 65% more.

- With supply falling and demand rising, the Expected Market Time, the number of days to sell all Orange County listings at the current buying pace, decreased from 41 to 37 days in the past couple of weeks, its lowest level since last April. It was 41 days last year, similar to today. The 3-year average before COVID (2017 to 2019) was 63 days, slower than today.

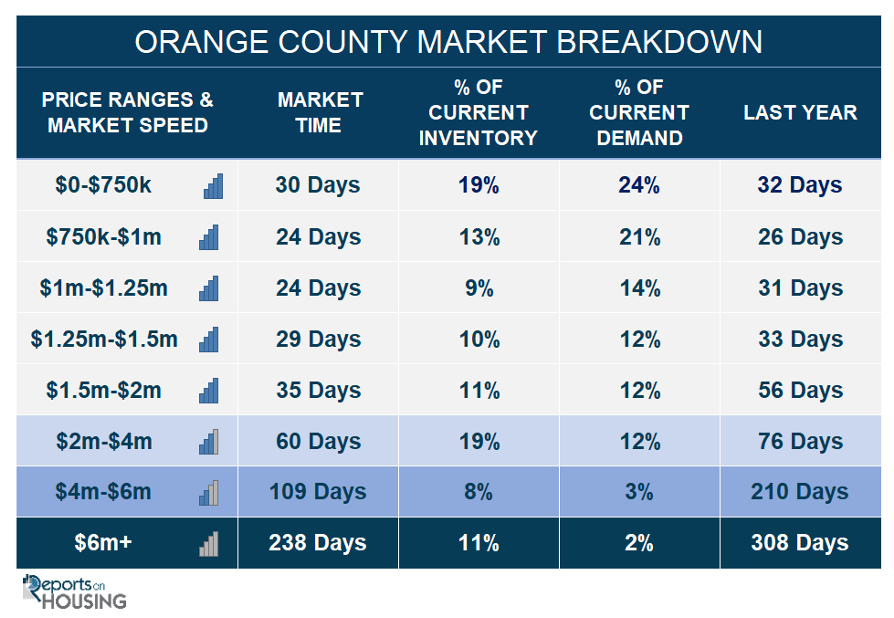

- The Expected Market Time for homes priced below $750,000 decreased from 31 to 30 days. This range represents 19% of the active inventory and 24% of demand.

- The Expected Market Time for homes priced between $750,000 and $1 million decreased from 27 to 24 days. This range represents 13% of the active inventory and 21% of demand.

- The Expected Market Time for homes priced between $1 million and $1.25 million decreased from 29 to 24 days. This range represents 9% of the active inventory and 14% of demand.

- The Expected Market Time for homes priced between $1.25 million and $1.5 million decreased from 33 to 29 days. This range represents 10% of the active inventory and 12% of demand.

- The Expected Market Time for homes priced between $1.5 million and $2 million remained unchanged at 35 days. This range represents 11% of the active inventory and 12% of demand.

- In the past two weeks, the expected market time for homes priced between $2 million and $4 million decreased from 66 to 60 days. For homes priced between $4 million and $6 million, the Expected Market Time decreased from 118 to 109 days. For homes priced above $6 million, the Expected Market Time decreased from 341 to 238 days.

- The luxury end, all homes above $2 million, account for 38% of the inventory and 17% of demand.

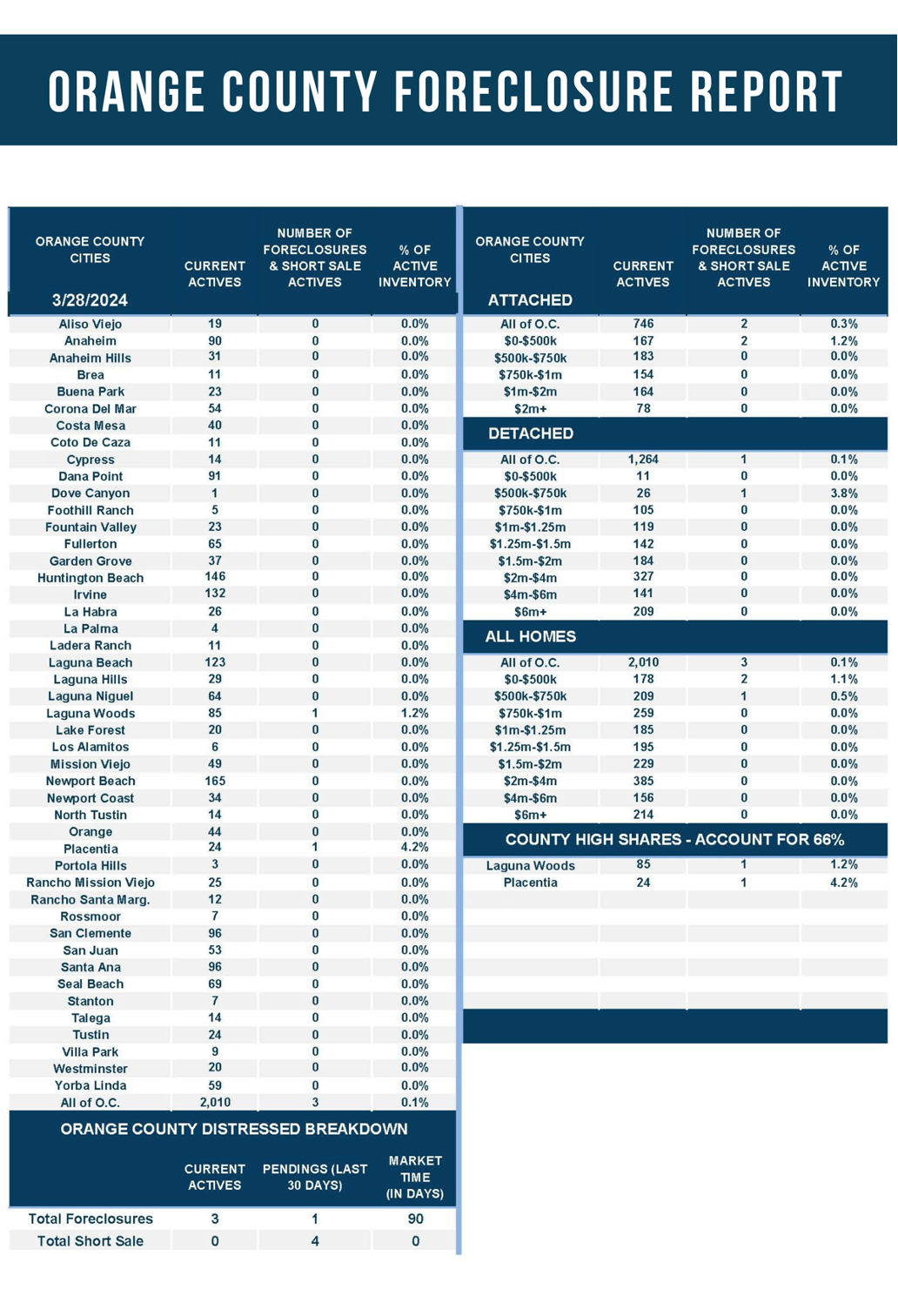

- Distressed homes, both short sales and foreclosures combined, comprised only 0.1% of all listings and 0.3% of demand. Only three foreclosures and no short sales are available today in Orange County, with three total distressed homes on the active market, down two from two weeks ago. Last year, ten distressed homes were on the market, similar to today.

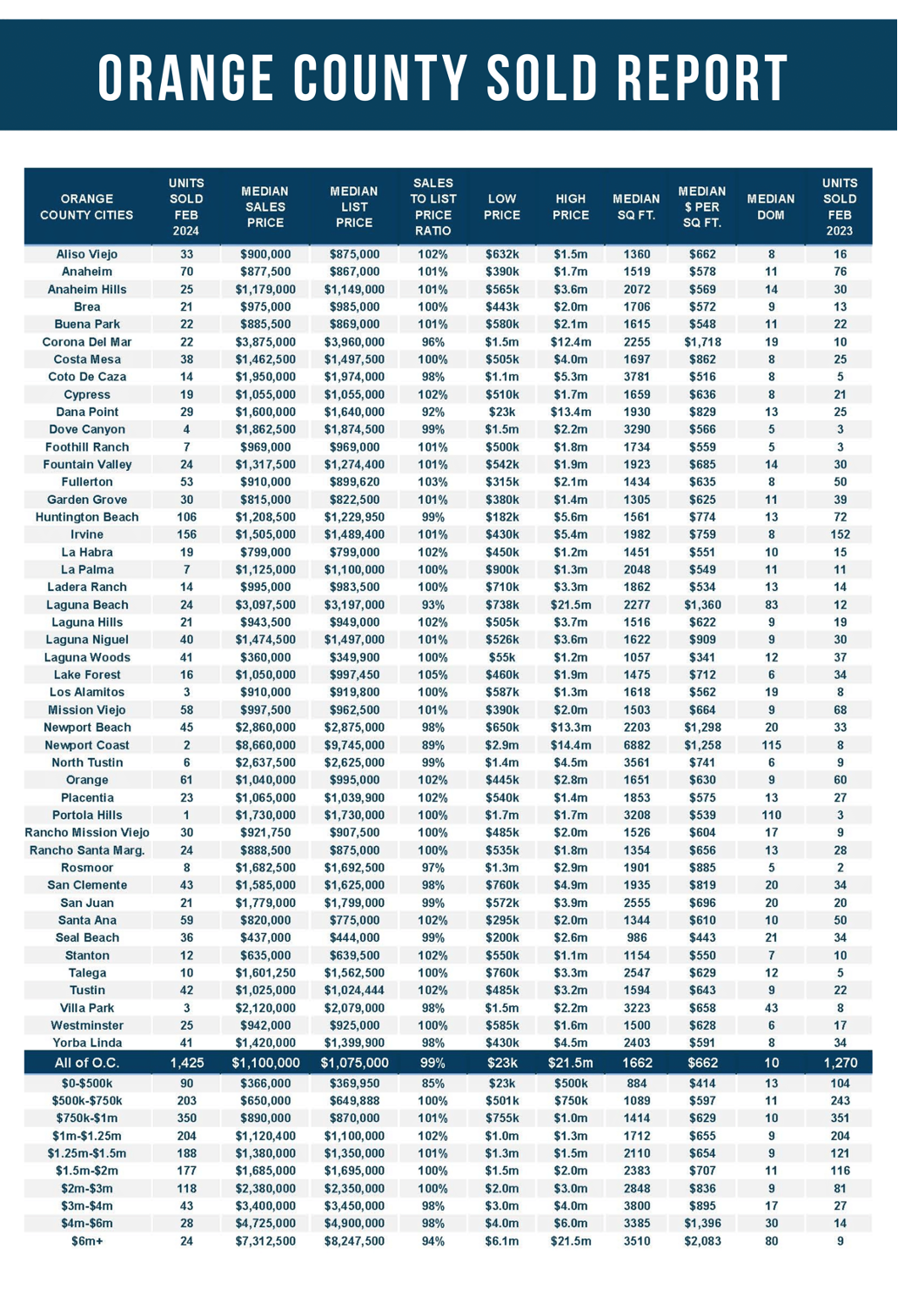

- There were 1,425 closed residential resales in February, up 12% from February 2023’s 1,270 and 21% from January 2024. The sales-to-list price ratio was 99.4% for Orange County. Foreclosures accounted for 0.4% of all closed sales, and there were no closed short sales. That means that 99.6% of all sales were good ol’ fashioned sellers with equity.

Have a great week.

Sincerely,

Steven Thomas

Quantitative Economics and Decision Sciences

Copyright 2024—Steven Thomas, Reports On Housing—All Rights Reserved. This report may not be reproduced in whole or in part without express written permission from the author.