April 29, 2024

It is best to step back from all the narratives, opinions, and noise whirling around the housing market and focus on the trends.

Housing Market Trends

With a third of the year in the rearview mirror, definitive trends have emerged in 2024.

Driving a car in the middle of the night on an unfamiliar road without headlights would be challenging. For buyers and sellers stepping into the real estate scene, the countless YouTube videos, headlines, and neighborhood chatter make it as daunting as driving that car in the dark with no lights. To properly shed light on the current state of the housing market, ignoring the noise and turning to the 2024 trends backed by statistics and data will allow buyers and sellers to navigate the real scene properly.

Here is a breakdown of the “Top 5” Orange County housing trends:

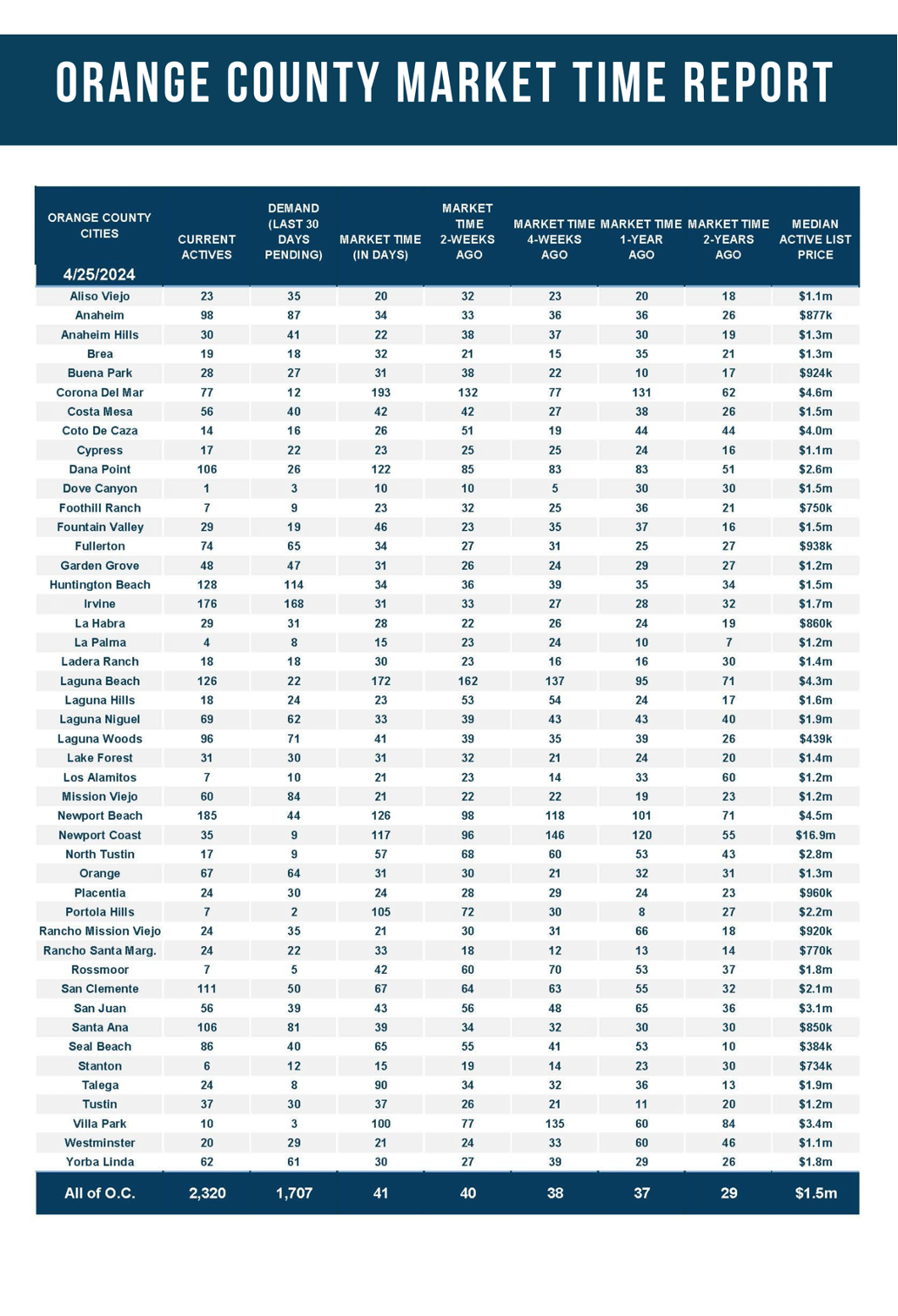

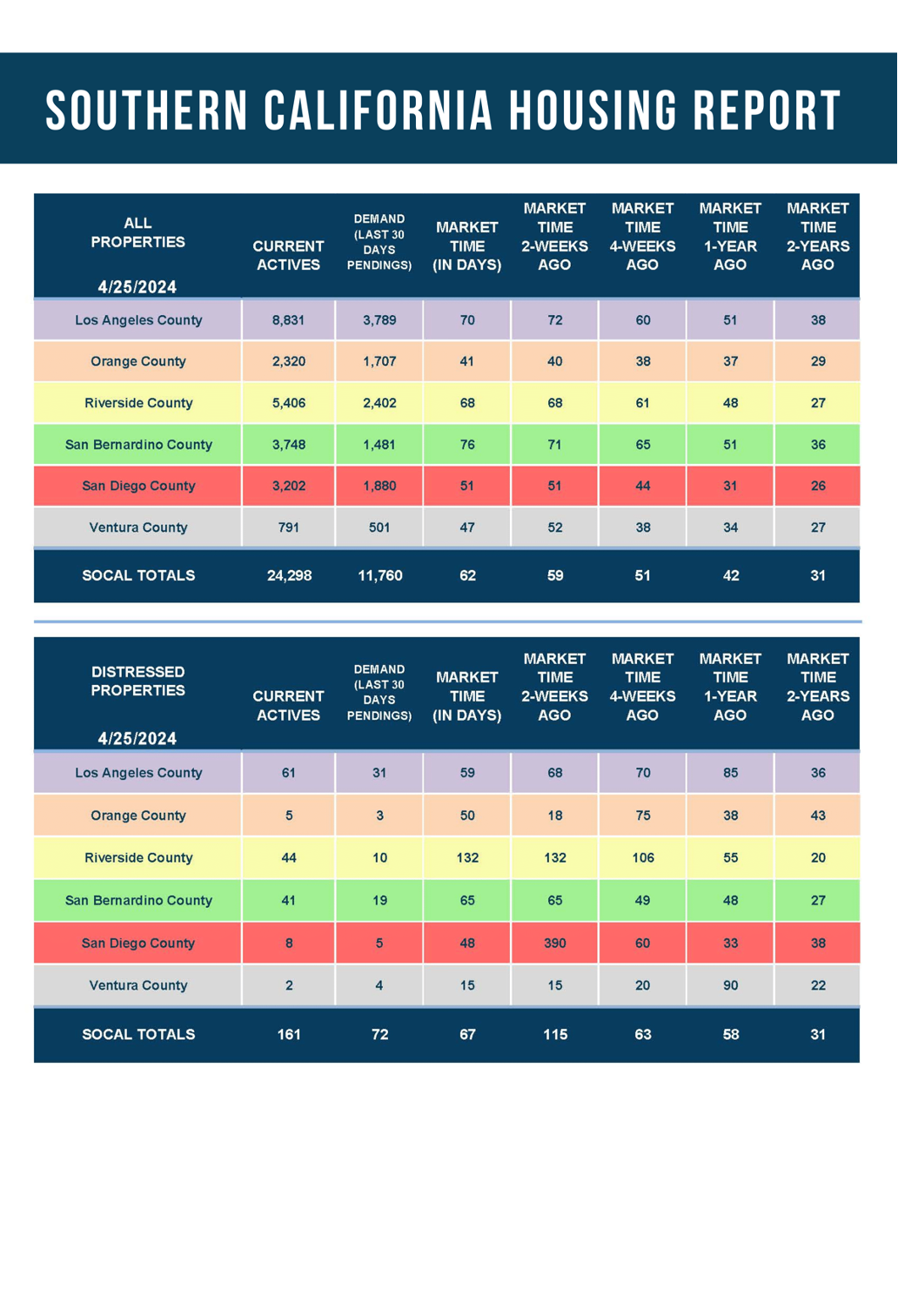

- After bouncing along a record-low number of homeowners willing to sell in the high mortgage rate environment, there are finally more new sellers in 2024. Most homeowners are “hunkering down,” unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. Since 84% of California homeowners with a mortgage have a fixed rate of 5% or lower, today’s nearly 7.5% mortgage rate prevents many would-be sellers from placing their homes on the market. In 2023, 41% fewer homeowners were willing to sell compared to the 3-year average before COVID (2017 to 2019), or 16,110 missing FOR-SALE signs. That is a large chunk of the market, considering the 3-year pre-pandemic average annual residential closed sales was 29,631. In 2024 through March, there were 37% fewer homeowners compared to the 3-year average. Yet, there were 13% more FOR-SALE signs than 2023, or an extra 720 sellers. It is a step in the right direction, and will dramatically improve once rates drop below 6.5%.

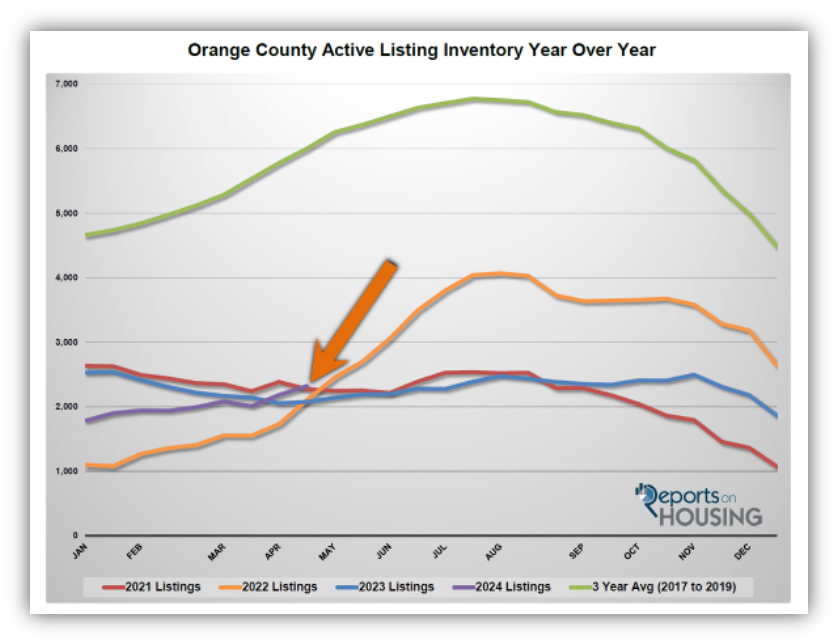

- With a rising inventory, more homes are on the market than last year. Last year, the active inventory continued to drop from January through mid-April. Before COVID, the inventory started to climb cyclically in January, not April. This year, the inventory began at 1,785 and has grown to 2,320 homes today, a rise of 30% or 535. On the surface, it appears to be a typical year. Yet, fewer homes are coming on the market. The low supply has been pitted against

low demand due to home affordability constraints. The growth in the inventory is a direct result of more homes coming on the market in the higher price ranges, which take a bit longer to sell compared to the lower ranges, starter homes. For homes priced below $1 million, from January through March, 8% fewer homes were placed on the market than last year. For homes above $1 million, there were 29% more homes. The higher the price range, the longer it takes to sell, which has allowed more homes to accumulate on the market and the inventory to rise.

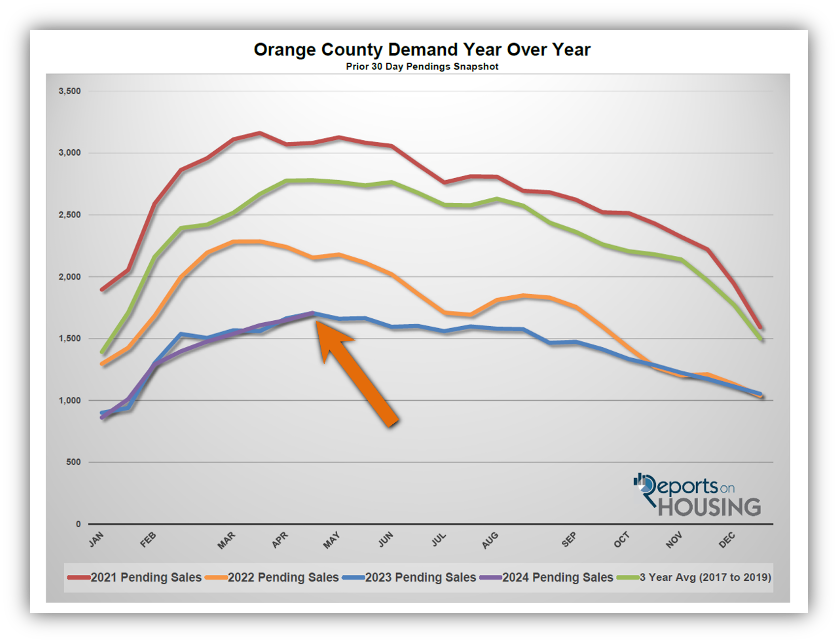

- Demand has been bouncing along a bottom like last year. The current demand trendline cannot get much lower than it currently stands. Demand in 2023 and 2024 has been subdued due to the high mortgage rate environment and the lack of homeowners willing to sell. Demand has remained at bare-bone, inherent levels. There are always buyers in every market. Year-over-year numbers have been nearly identical since ringing in the New Year. Currently, demand, a snapshot of the number of new pending sales over the prior month, is at 1,707 pending sales, nearly identical to last year’s 1,706 level. Demand will only break higher when rates drop substantially below the 7% threshold. Until then, demand will continue to bounce along a bottom.

- The market speed is a bit slower than last year. The Expected Market Time, the number of days it takes to sell all Orange County listings at the current buying pace, is a function of supply and demand. At the beginning of the year, fewer homes were on the market than at the start of 2023, and demand was similar. Due to the constrained inventory, the Expected Market Time was lower year-over-year. The market felt noticeably faster in January. The Expected Market time was 56 days at the end of January, much faster than last year’s 81 days. Demand has closely mirrored 2023 this year, yet the inventory has slowly but surely grown. There are now more homes available than last year. With more supply and similar demand to the previous year, the market is slower than in 2023. Today’s Expected Market time is 41 days compared to 37 days last year. As long as the inventory growth continues to outpace last year’s growth, the market will continue to slow faster than last year. In the trenches, the difference between 41 and 37 days is almost undetectable, yet if current trends continue, year-over-year comparisons will be much more noticeable.

- Higher mortgage rates are muffling the true potential of the Orange County housing market. While mortgage rates had surpassed 8% in October, they plunged to nearly 6.5% in mid-December. They started 2024 at just over 6.5%, close to January 2023. However, economic report after economic report exceeded expectations, which resulted in mortgage rates continuously climbing. In February and March, rates danced around 7%, the psychological barrier preventing many buyers from pursuing a home and some homeowners from listing their homes for sale. Rates have remained above 7% with duration since the start of April, similar to the second half of 2023. In January and February, closed sales were up 8% compared to last year. Yet, in March, sales were down by 0.5% due to climbing rates. Today’s 7.43% rate is much higher than 2023’s 6.59% level. As long as rates remain above the 7% threshold, activity will slow and impact the number of closed sales.

Active Listings

The active inventory climbed by 6% in the past couple of weeks.

The active listing inventory increased by 136 homes in the past two weeks, up 6%, and now sits at 2,320, its highest level since last year’s November peak. The inventory has surged by 15% in the past month, adding 310 homes. The inventory is at its highest level for the end of April since 2020. There are finally more choices for buyers, at least in the upper price ranges. Last year, the inventory had dropped by 3% in four weeks. A rising supply is a step in the right direction for an inventory starved for more choices. Expect the inventory to continue to grow at an elevated pace as long as mortgage rates remain above 7% with duration.

Last year, the inventory was 2,076 homes, 11% lower, or 244 fewer. The 3-year average before COVID (2017 through 2019) was 6,002, an additional 3,682 homes, or 159% more, more than double the current level.

Homeowners continue to “hunker down” in their homes, unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. For March, 2,285 new sellers entered the market in Orange County, 1,623 fewer than the 3-year average before COVID (2017 to 2019), 42% less. Last March, there were 2,136 new sellers, 7% fewer than this year. A few more sellers are opting to sell compared to the previous year.

Demand

Demand increased by 4% in the past couple of weeks.

Demand, a snapshot of the number of new pending sales over the prior month, increased from 1,648 to 1,707 in the past couple of weeks, up 59 pending sales, or 4%, its highest level since September 2022, surpassing last year’s peak in demand of 1,706 at the end of April, one fewer pending sale. Expect demand to peak shortly as demand closely resembles last year’s path. It will continue to closely mirror 2023 demand until rates drop to the mid-6s with duration. If that were to occur later this year, expect demand to reignite and potentially reach a much later peak. Only time will tell whether or not the U.S. economy cools from here and inflation resumes its downward path, which are the necessary components to an eventual easing in rates as prescribed by the Federal Reserve.

Last year, demand was 1,706, almost identical to today, or one fewer pending sale. The 3-year average before COVID (2017 to 2019) was 2,780 pending sales, 63% more than today, or an additional 1,073.

With supply rising faster than demand, the Expected Market Time (the number of days it takes to sell all Orange County listings at the current buying pace) increased from 40 to 41 days in the past couple of weeks. Last year, it was 37 days, similar to today. The 3-year average before COVID was 65 days, slower than today.

Luxury End

The luxury market continued to slow in the past couple of weeks.

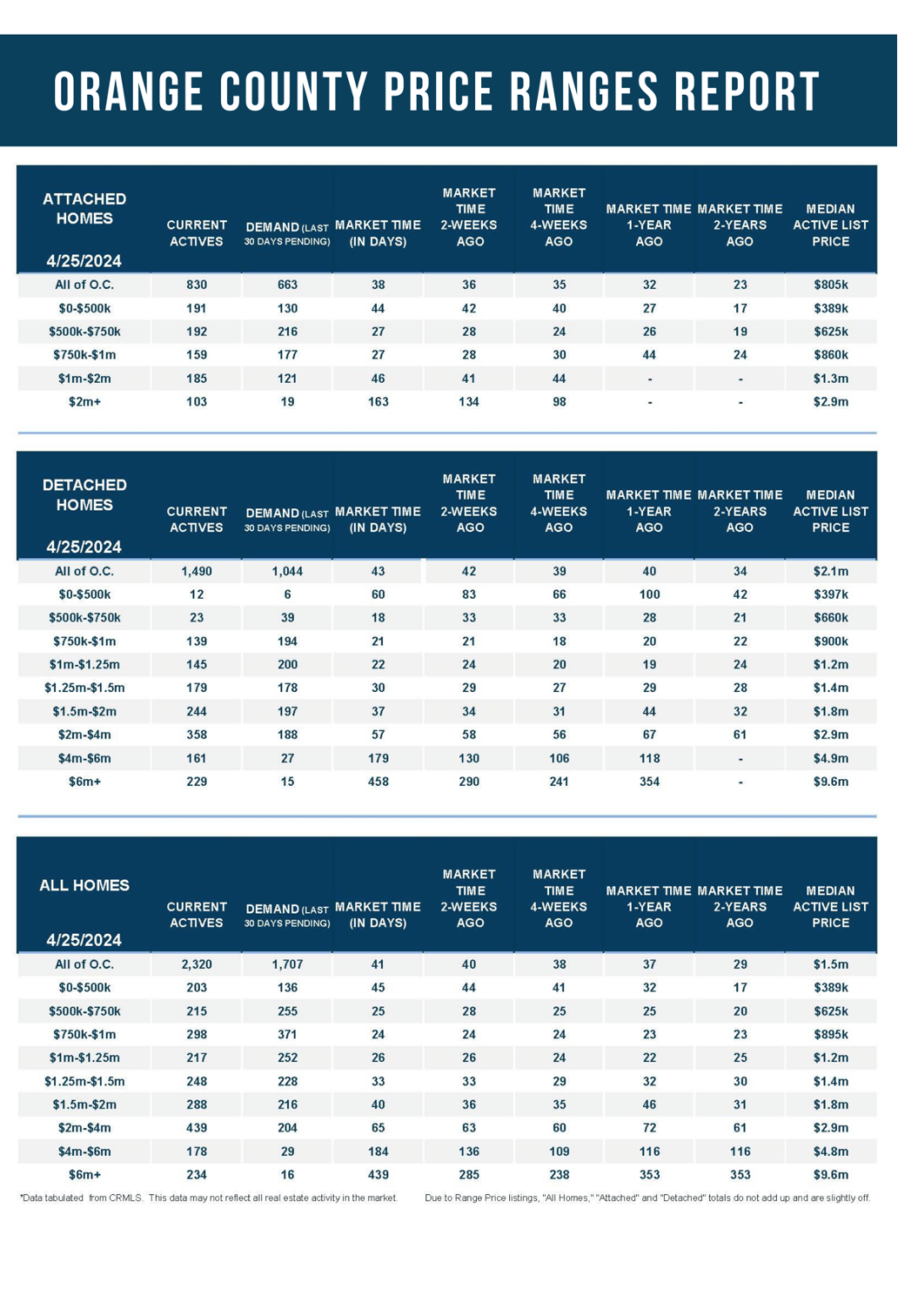

In the past couple of weeks, the luxury inventory of homes priced above $2 million increased from 787 to 851 homes, up 64 or 8%, the highest level since November 2020. Luxury demand decreased by five pending sales, down 2%, and now sits at 249. With supply rising and demand falling, the Expected Market Time for luxury homes priced above $2 million increased from 93 to 103 days, its highest level since the start of February. The 103-day level is still very hot for luxury, yet the trend for the past four weeks has indicated that luxury is cooling. The equity market has been more volatile recently due to sticky inflation and cooling GDP.

Year over year, the active luxury inventory is up by 174 homes or 26%, and luxury demand is up by 48 pending sales or 24%. Last year’s Expected Market Time was 101 days, similar to today.

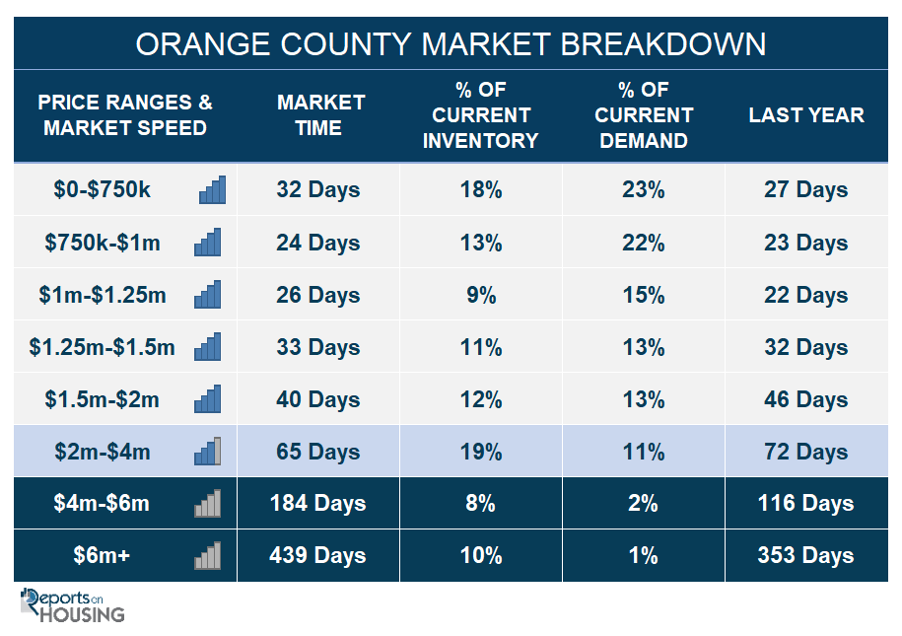

In the past two weeks, the expected market time for homes priced between $2 million and $4 million increased from 64 to 65 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 138 to 184 days. For homes priced above $6 million, the Expected Market Time increased from 247 to 439 days. At 439 days, a seller would be looking at placing their home into escrow around July 2025.

Orange County Housing Summary

- The active listing inventory in the past couple of weeks increased by 136 homes, up 6%, and now sits at 2,320. In March, 42% fewer homes came on the market compared to the 3-year average before COVID (2017 to 2019), 1,623 less. 149 more sellers came on the market this March compared to 2023. Last year, there were 2,076 homes on the market, 244 fewer homes, or 11% less. The 3-year average before COVID (2017 to 2019) was 6,002, or 159% extra, more than double.

- Demand, the number of pending sales over the prior month, increased by 59 pending sales in the past two weeks, up 4%, and now totals 1,707. Last year, there were 1,706 pending sales, nearly identical to today. The 3-year average before COVID (2017 to 2019) was 2,780, or 63% more.

- With supply rising faster than demand, the Expected Market Time, the number of days to sell all Orange County listings at the current buying pace, increased from 40 to 41 days in the past couple of weeks. It was 37 days last year, similar to today. The 3-year average before COVID (2017 to 2019) was 65 days, slower than today.

- The Expected Market Time for homes priced below $750,000 decreased from 33 to 32 days. This range represents 18% of the active inventory and 23% of demand.

- The Expected Market Time for homes priced between $750,000 and $1 million remained unchanged at 24 days. This range represents 13% of the active inventory and 22% of demand.

- The Expected Market Time for homes priced between $1 million and $1.25 million remained unchanged at 26 days. This range represents 9% of the active inventory and 15% of demand.

- The Expected Market Time for homes priced between $1.25 million and $1.5 million decreased from 34 to 33 days. This range represents 11% of the active inventory and 13% of demand.

- The Expected Market Time for homes priced between $1.5 million and $2 million increased from 36 to 40 days. This range represents 12% of the active inventory and 13% of demand.

- In the past two weeks, the expected market time for homes priced between $2 million and $4 million increased from 64 to 65 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 138 to 184 days. For homes priced above $6 million, the Expected Market Time increased from 247 to 439 days.

- The luxury end, all homes above $2 million, account for 37% of the inventory and 14% of demand.

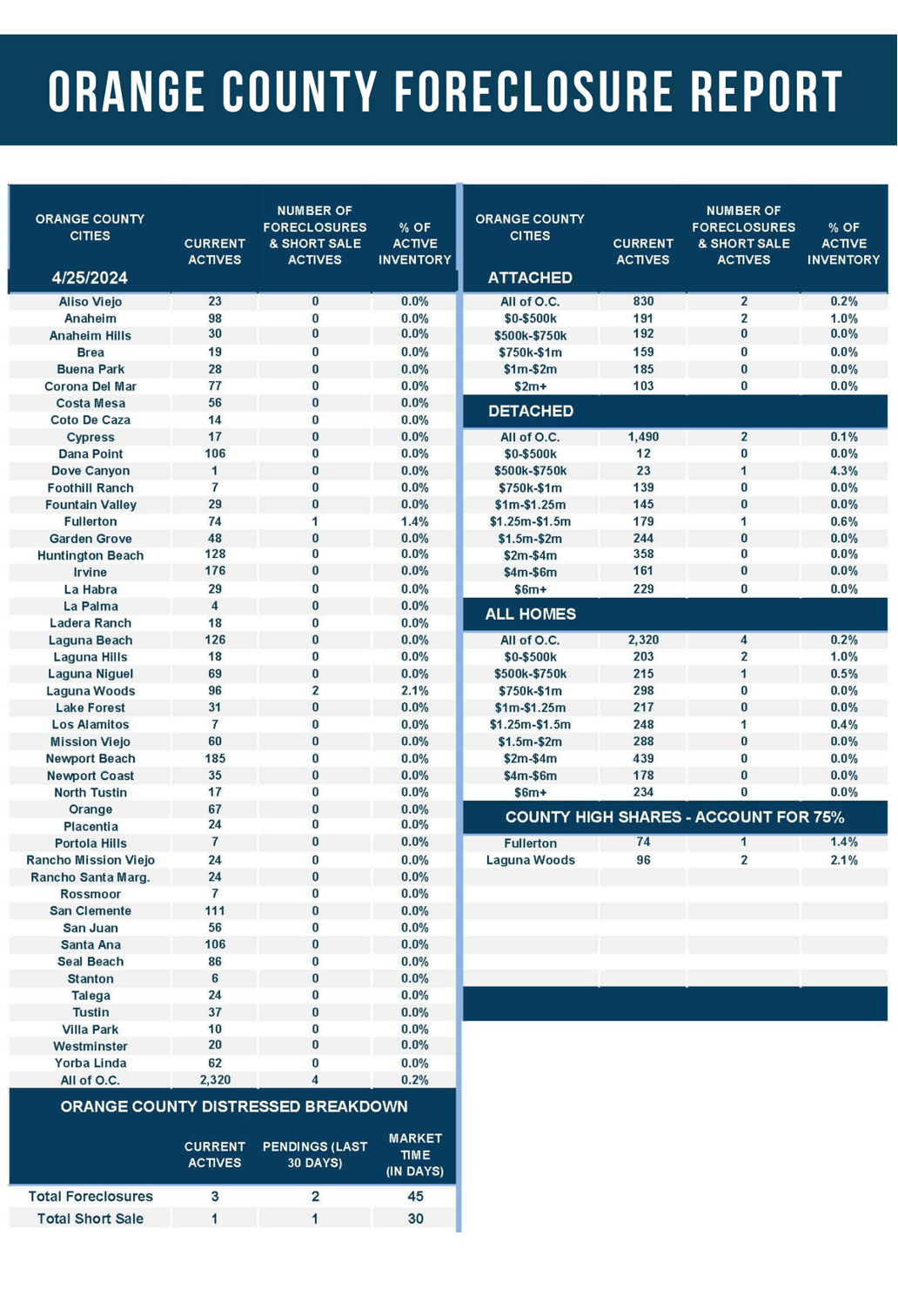

- Distressed homes, both short sales and foreclosures combined, comprised only 0.2% of all listings and 0.2% of demand. Only three foreclosures and one short sale are available today in Orange County, with four total distressed homes on the active market, down one from two weeks ago. Last year, 12 distressed homes were on the market, similar to today.

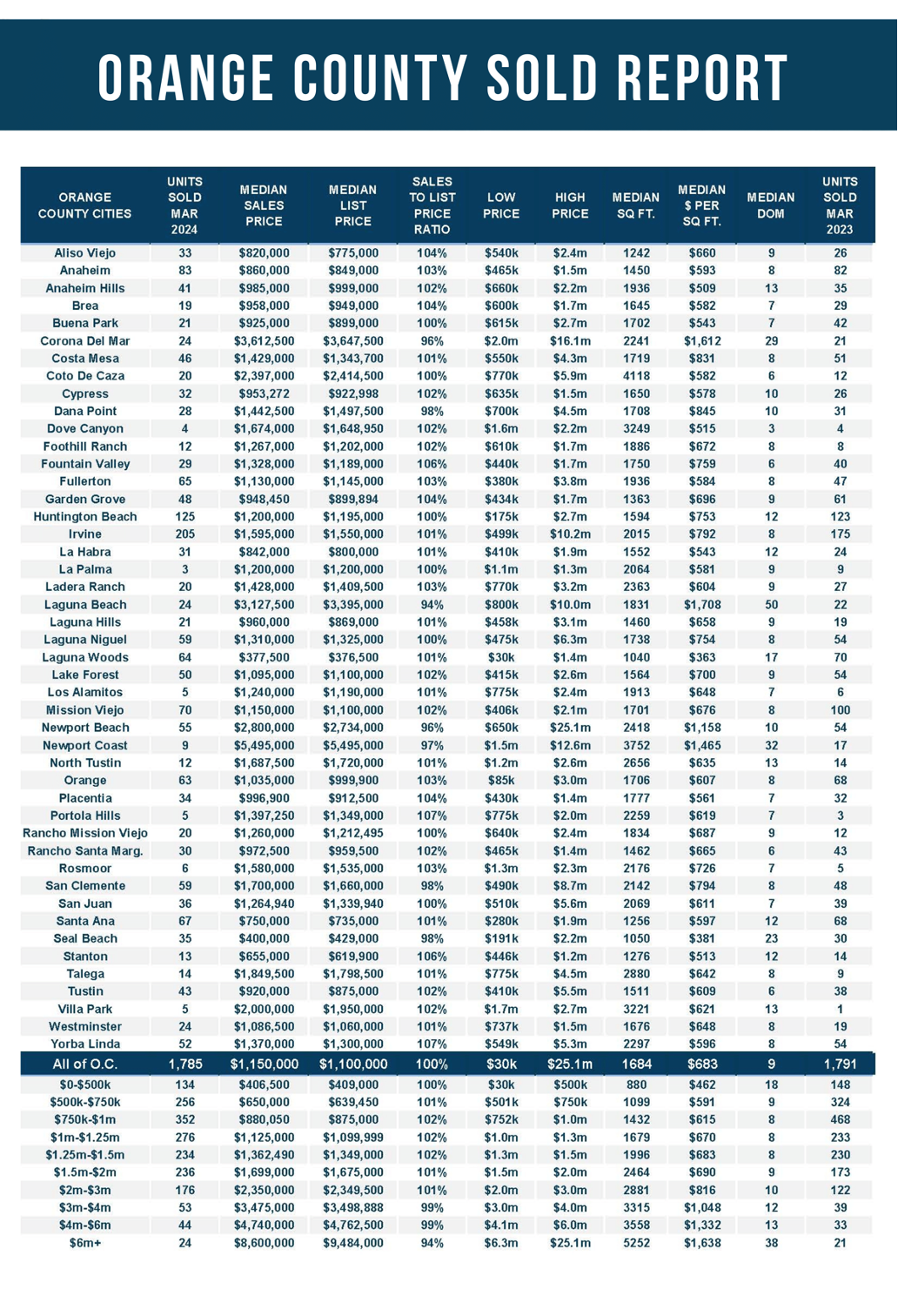

- There were 1,785 closed residential resales in March, nearly identical to March 2023’s 1,791, and up 41% from February 2024. The sales-to-list price ratio was 100.4% for Orange County. Foreclosures accounted for 0.1% of all closed sales, and short sales accounted for 0.1%. That means that 99.8% of all sales were good ol’ fashioned sellers with equity.

Have a great week.

Sincerely,

Steven Thomas

Quantitative Economics and Decision Sciences

Copyright 2024—Steven Thomas, Reports On Housing—All Rights Reserved. This report may not be reproduced in whole or in part without express written permission from the author.