June 23, 2025

It is official, the Orange County housing market has tipped in the buyer’s favor with the slowest June since 2011.

It’s the Buyer’s Turn

With inventory climbing 61% since last year and demand remaining almost unchanged, the market has slowed substantially.

Standing at the grocery store checkout on a busy afternoon, the lines can stretch on for what seems like forever. Upon looking around, there are inevitably several registers that are not open, despite the throngs of shoppers waiting for someone to ring them up. After waiting for several minutes, not one, but three registers open up, and all lanes are open. “Next in line,” the new cashiers announce. Suddenly, the lines move rapidly, and everyone is able to check out so that they can get home and put away their groceries.

Home buyers have been stuck in long checkout lines with a limited inventory that dates back to the start of 2020. Open houses have been crowded. Multiple offers were the norm. Throngs of buyers toured homes, wrote offers, and hoped that someday they too would be able to secure a home. Suddenly, with the highest June supply since 2019, buyers have a lot more choices, and negotiations are lining up in their favor. Buyers are finally able to “check out” and secure a place to call home.

The evolution of the buyer’s market was extremely slow, taking years to develop. It began in 2022, when rates surged higher, rising from 3.25% in January to 7.37% in October. To counter the low demand, the active inventory remained chronically low as very few homeowners participated in the housing market. Homeowners chose to “hunker down” in their homes, unwilling to move due to their underlying, locked-in, low fixed-rate mortgage. As of the start of 2025, 80% of Californians with a mortgage enjoy a fixed rate at or below 5%. In 2023, 41% fewer homes were placed on the market in Orange County compared to the 3-year pre-pandemic average (2017-2019), or 16,000 missing FOR SALE signs.

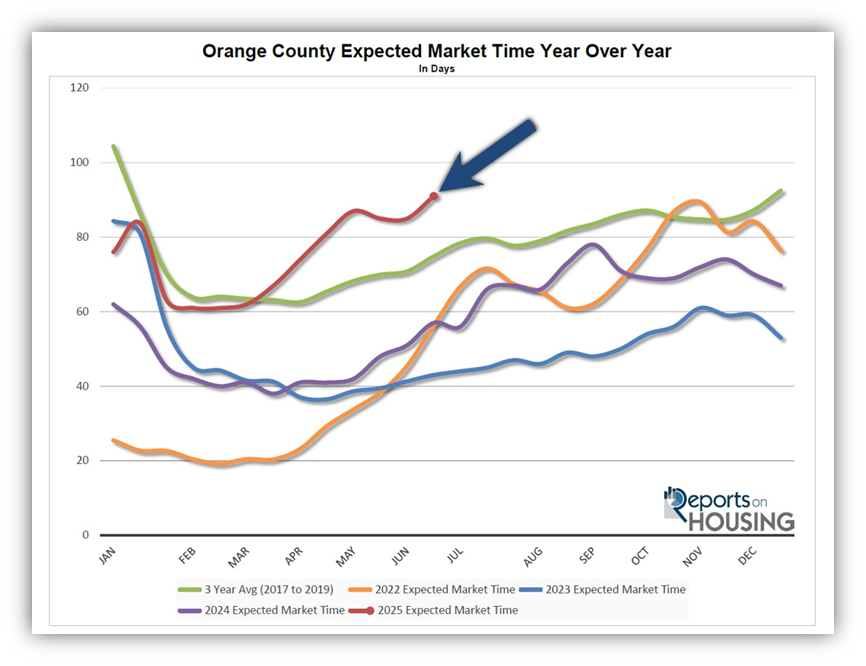

However, in 2024, with more homeowners participating, the number of missing signs dropped to 31%, or 12,300 fewer sellers. In 2025, it is only off by 25% through May. That’s an additional 1,908 sellers compared to last year, and 3,632 more than in 2023. In matching nearly identical demand compared to 2023 and 2024, the additional sellers have accumulated, and the inventory has grown substantially. With rising inventory and muted demand, the Expected Market Time (the number of days it takes to sell all Orange County listings at the current buying pace), the actual speed of the market, has grown to 91 days, its highest June level since 2011.

The active inventory currently stands at 4,894 homes, which is 61% higher than last year’s 3,048 homes and 115% higher than 2023’s 2,281 homes. Demand (a snapshot of the number of new pending sales over the prior month) is currently at 1,614 pending sales, one less than last year’s 1,615 reading, and 13 more than in 2023. Today’s 91-day Expected Market Time is 34 additional days compared to last year’s 57 days, and more than double 2023’s 43 days.

It is today’s longer market time that is tipping the Orange County housing market in the buyer’s favor. There are a lot more sellers competing against each other. A revealing 37% of the active inventory has reduced the asking price at least once. Through May, 2,860 unsuccessful sellers have pulled their homes off the market, up 96% compared to last year. Sellers are more willing to negotiate today than they have been for years.

ATTENTION BUYERS: Do not wait for prices to plunge before purchasing. Home values are up 4.6% year-over-year in May in Orange County, according to Zillow’s Home Value Index, yet they are down 0.4% month over month. It will continue to slowly decline through the end of the year as long as mortgage rates remain close to 7%. Home values will not plunge. There are very few sellers desperate to sell their homes. The housing stock, all homeowners combined, is the strongest it has ever been. Ever since the Great Recession, buyers have been purchasing homes with strict qualifications, strong credit, great jobs, and low fixed payments. There is record tappable equity (the amount of equity a homeowner can use for a loan while still retaining at least 20% equity), record equity-rich (50% or more equity), and a record number of homeowners who own their homes free and clear. Due to the homeowner’s strength, sellers will be unwilling to give up much equity. To achieve success, some sellers will be willing to take just a little bit less than the last successful seller; thus, home values will slowly drift down.

ATTENTION SELLERS: Accurate pricing is the most crucial step to achieving success in today’s highly competitive market. Methodically arrive at a home’s Fair Market Value by carefully scrutinizing the most recent pending and closed sales. Overpriced homes do not sell. Instead, it wastes valuable market time. The market is only slowing from week to week. Housing will be slower when a home’s price is adjusted down the road, and any price improvement does not receive the same fanfare as when it was initially listed for sale.

After many years lining up in favor of sellers, the Orange County housing market is finally a buyer’s market.

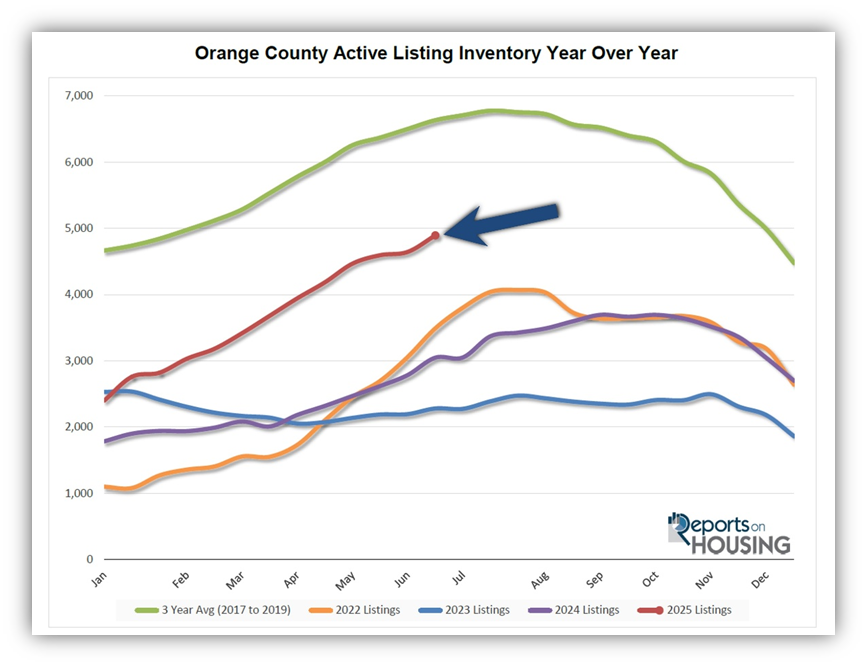

Active Listings

The inventory grew by 5% over the past couple of weeks.

The active listing inventory increased by 249 homes over the past two weeks, up 5%, and now stands at 4,894, its largest rise in six weeks and its highest level since June 2020. During the Summer Market, expect the inventory to rise unabated until it peaks. Over the last couple of years, the peak has arrived a bit late, between September and November. This year could be the same unless rates unexpectedly fall below 6.5% with duration. If that were to occur, increased demand would limit the increase in supply.

Last year, the inventory was at 3,048 homes, 38% lower, or 1,846 fewer. The 3-year average before COVID (2017-2019) was 6,633, an additional 1,739 homes, or 36% more.

Homeowners continue to “hunker down” in their homes, unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. This trend has been easing from the lows established in 2023. Through May, 13,694 homes were placed on the market in Orange County, 4,585 fewer than the 3-year average before COVID (2017-2019), 25% less. In 2024, only 11,786 homes entered the market, and in 2023, it was only 10,062. More sellers are opting to sell in 2025.

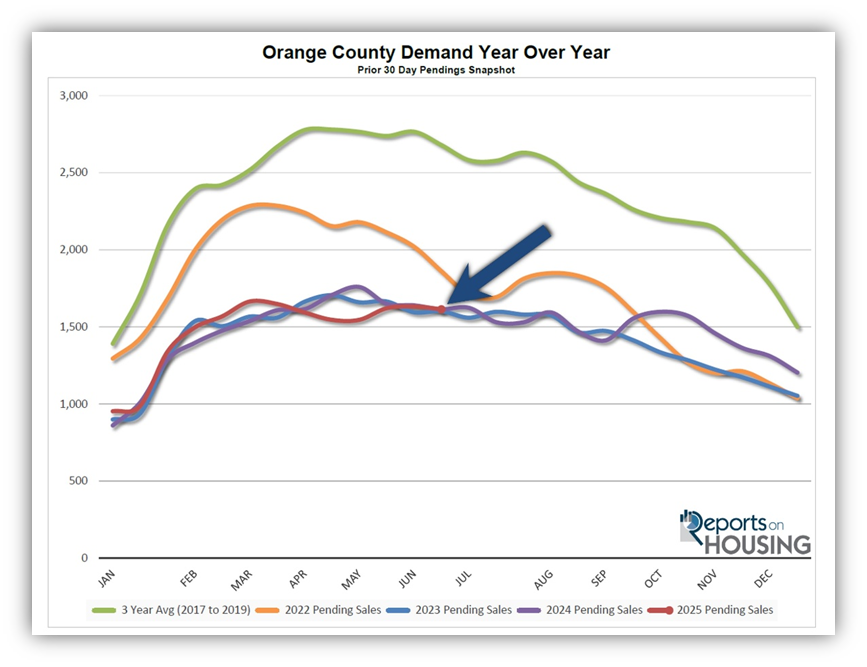

Demand

Demand decreased by 19 pending sales.

Demand, a snapshot of the number of new pending sales over the prior month, decreased from 1,633 to 1,614 in the past couple of weeks, representing a 19-pending-sale decline, or 1%. Buyer demand has remained at very similar levels since October 2022. The pace of demand is at the mercy of mortgage rates, which have been bouncing around 7% for nearly 32 months. Demand will break higher as soon as rates drop below 6.5% with duration. They were at that level for 47 days last year from late August through the start of October. When rates drop and stay there for months, buyer demand will rapidly accelerate, and closed sales will increase. Until then, it will remain the same.

Last year, demand was 1,615, with one additional pending sale, or nearly unchanged. The 3-year average before COVID (2017-2019) was 2,679 pending sales, 66% higher than today, representing an additional 1,065 sales.

As the Federal Reserve has indicated, watching all economic releases for signs of slowing is essential. That is the only path to lower mortgage rates at this time. These releases can cause mortgage rates to move higher or lower, depending on how they compare to market expectations. This week, the Personal Consumption Expenditures – Price Index (PCE), the Fed’s preferred inflation gauge, will be released on Friday. Next week is job’s week, which includes the number of job openings, wages, and the number of jobs created or lost – one of the month’s most important economic data points.

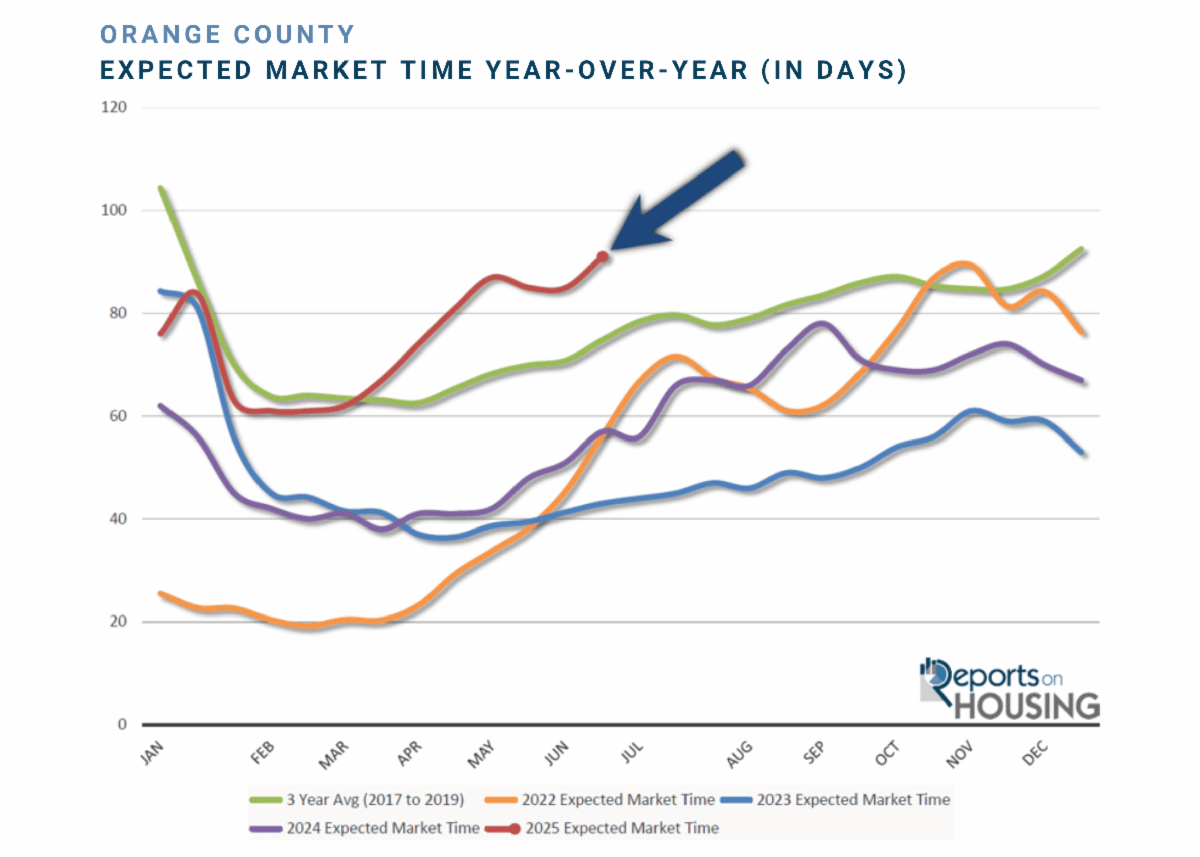

Expected Market Time

The Expected Market Time has grown by six days over the past couple of weeks.

With the supply of available homes rising by 249 homes, up 5%, and demand dropping by 19 pending sales, down 1%, the Expected Market Time (the number of days it takes to sell all Orange County listings at the current buying pace) increased from 85 to 91 days in the past couple of weeks, its highest June level since 2011.

Last year, it was 57 days, substantially faster than today. The 3-year average before COVID was 75 days, which is also much quicker than today.

The Expected Market Time for condominiums and townhomes increased from 77 to 81 days in the past two weeks. It was at 49 days last year. For detached homes, the Expected Market Time increased from 91 to 98 days. It was 62 days a year ago.

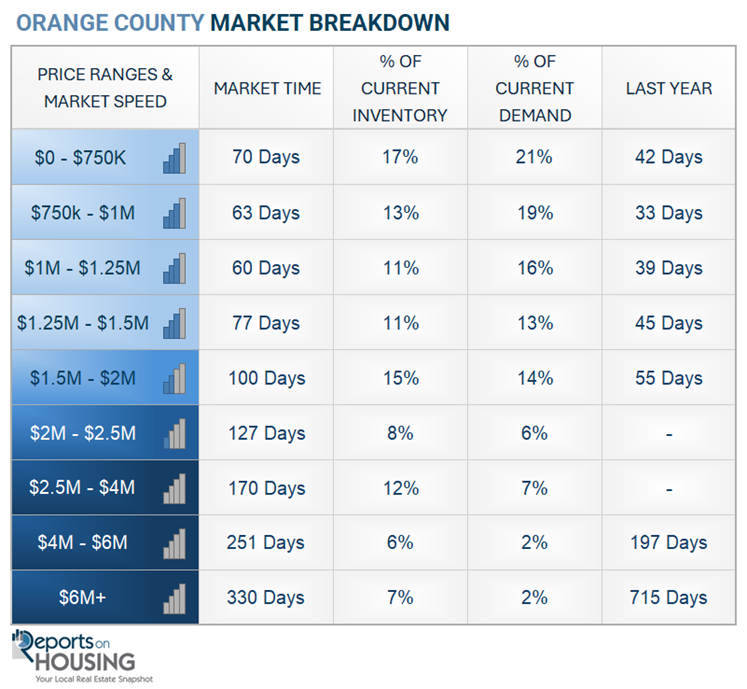

Luxury End

The luxury market slowed in the past couple of weeks.

The luxury inventory of homes priced above $2.5 million (the top 10% of the Orange County housing market) increased from 1,212 to 1,238 homes, a rise of 26 homes. Luxury demand decreased by 11 pending sales, down 6%, and now sits at 172. The Expected Market Time for luxury homes priced above $2.5 million increased slightly from 199 to 216 days, its highest reading since April. Expect the luxury market to continue to moderate and cool somewhat during the Summer Market.

In the past two weeks, the Expected Market Time for homes priced between $2.5 million and $4 million increased from 151 to 170 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 248 to 251 days. For homes priced above $6 million, the Expected Market Time increased from 324 to 330 days. At 330 days, a seller would be looking at placing their home into escrow around May 2026.

Orange County Housing Summary

- INVENTORY: The active listing inventory in the past couple of weeks increased by 249 homes, up 5%, and now sits at 4,894, its highest level since June 2020. Last year, there were 3,048 homes on the market, 1,846 fewer homes, or 38% less. The 3-year average before COVID (2017-2019) was 6,633, which is 36% higher. From January through May, 25% fewer homes came on the market compared to the 3-year average before COVID (2017-2019), 4,585 less. Yet, 1,908 more sellers came on the market this year than last, and 3,632 more compared to 2023.

- DEMAND: Buyer demand, the number of pending sales over the prior month, decreased from 1,633 to 1,614. Last year, there were 1,615 pending sales, nearly the same as today. The 3-year average before COVID (2017-2019) was 2,679, which is 66% higher.

- MARKET TIME: With supply rising and demand falling slightly, the Expected Market Time, the number of days to sell all Orange County listings at the current buying pace, increased from 85 to 91 days in the past couple of weeks. Last year, it was 57 days, substantially faster than today. The 3-year average before COVID (2017-2019) was 75 days, which is also significantly faster than today.

- LUXURY: In the past two weeks, the Expected Market Time for homes priced between $2.5 million and $4 million increased from 151 to 170 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 248 to 251 days. For homes priced above $6 million, the Expected Market Time increased from 324 to 330 days.

- DISTRESSED HOMES: Short sales and foreclosures combined, comprised only 0.2% of all listings and 0.2% of demand. Only seven foreclosures and five short sales are available today in Orange County, with a total of 12 distressed homes on the active market, up four from two weeks ago. Last year, five distressed homes were on the market, similar to today.

- CLOSED SALES: There were 1,819 closed residential resales in May, down 14% compared to May 2024’s 2,127 and down 2% from April 2025. The sales-to-list price ratio was 98.7% for Orange County. Foreclosures accounted for 0.2% of all closed sales, and short sales accounted for 0.1%. That means that 99.7% of all sales were sellers with equity.

Have a great week.

Sincerely,

Steven Thomas

Quantitative Economics and Decision Sciences

Copyright 2025—Steven Thomas, Reports On Housing—All Rights Reserved. This report may not be reproduced in whole or in part without express written permission from the author.