October 28, 2024

With so many varying viewpoints and narratives swirling about the housing market, it is best to take a step back from the noise and focus on the latest trends.

Housing Market Trends

It is the home stretch of the 2024 housing market, and definitive trends have emerged.

Everyone seems to have an opinion about real estate. With so many differing viewpoints, from doom and gloom to surging markets, it is difficult to make heads or tails of the direction of the housing market. News articles with catchy headlines and YouTube channels devoted to negative narratives make understanding the current market even more confusing.

It is time to step aside from the constant buzz and look at the trends that have developed to wrap up 2024.

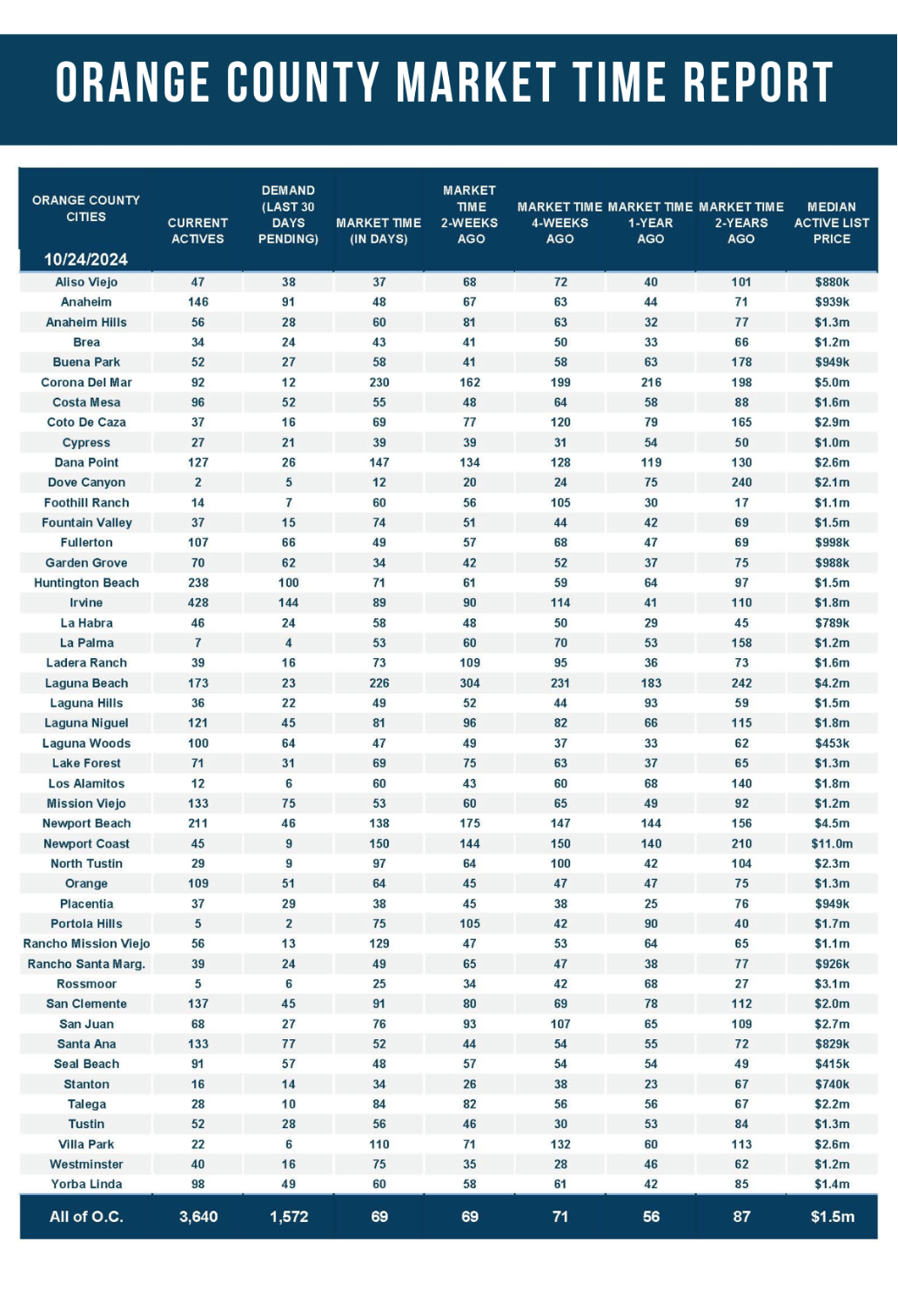

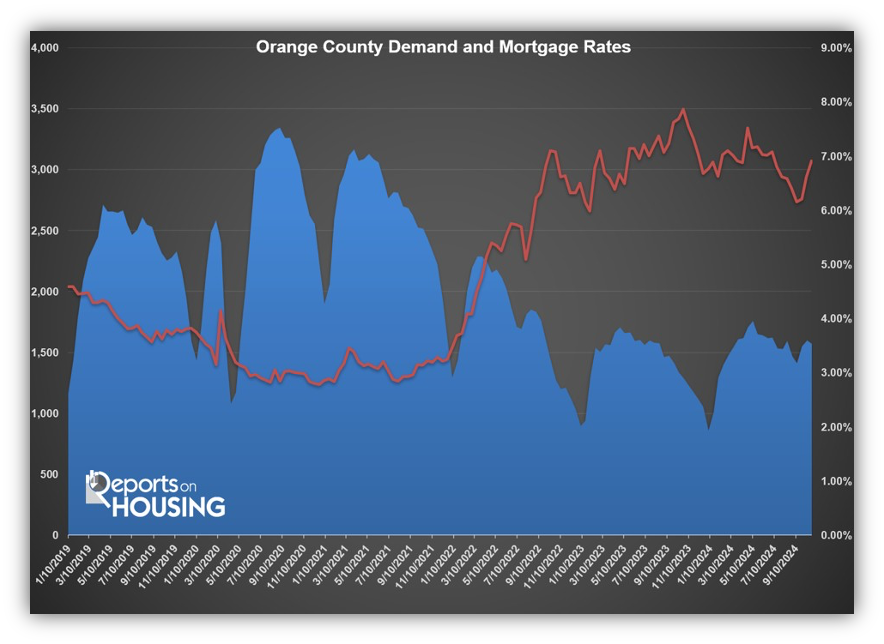

- When mortgage rates drop below 6.5% with duration, demand will rise and market times will drop. The housing market is very sensitive to rates. From April through the start of July, they were hopelessly stuck above 7%. Home affordability diminishes further at that level, taxing buyer demand and preventing homeowners from selling their homes. Fewer buyers can afford a home, and homeowners are unwilling to trade in their low, fixed-rate mortgage for a much higher 30-year rate. Even with the accumulation of more homes on the market and more choices for buyers, demand did not budge from last year’s levels. Year-over-year demand readings were nearly identical through mid-September. Yet, that changed as rates finally slipped below 6.5% at the end of August. In mid-September, they bottomed out for the year at 6.11%, the lowest level since February 2023.

Those low rates eroded in October with stronger-than-expected economic releases, from jobs to retail sales. They remained below 6.5% for 42 days, long enough to see a noticeable change in demand and the Expected Market Time, the speed of the market. When rates drop, they slowly work their way through the housing market. The longer they remain, the more significant the impact. From September 12th through October 10th, four weeks, demand (a snapshot of the number of new pending sales over the prior month) increased from 1,413 to 1,598, up 13%. The Expected Market Time (the number of days it takes to sell all Orange County listings at the current buying pace) decreased from 78 to 69 days. Typically, demand slowly declines, and the Expected Market Time does not change much during the Autumn Market.

According to Mortgage News Daily, October has seen a reversal in mortgage rates, increasing from 6.2% on October 1st to 7% today. The rise comes from strong economic readings, speculation, and post-election positioning. The path of rates will continue to be volatile. Nonetheless, once rates drop below 6.5% with duration, the housing market will heat up with an increase in pending sales, more homeowners opting to sell, and a rise in closed sales.

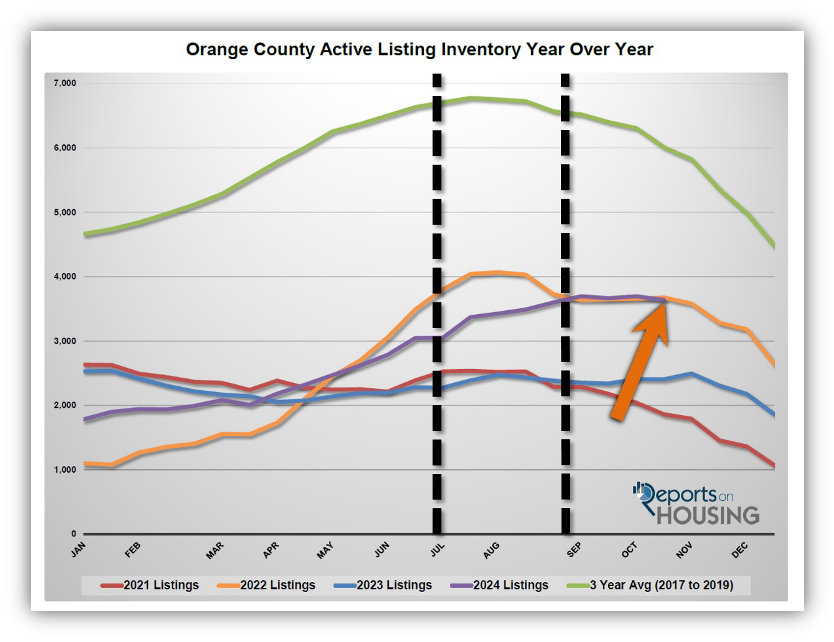

- The 2024 inventory peak has been delayed yet again. The higher mortgage rate environment has not allowed enough pending sales activity to cut into the active inventory. Typically, the Orange County inventory peak occurs between July and August. Once the kids go back to school, the supply of available homes slowly drops for the remainder of the year. It plunges lower from Thanksgiving through New Year’s Day. This year, the inventory grew from 3,052 on July 4th to 3,694 on October 10th, up 21% or 642 homes. The rise in mortgage rates during October, just like 2022 and 2023, has cut back on demand. When fewer pending sales occur, the inventory accumulates and does not properly descend. The fewest number of homes are placed on the market in November and December. With fewer homes coming on the market, and a rush of unsuccessful sellers throwing in the towel just in time to enjoy the holidays, the inventory finally falls to finish up the year.

It appears the inventory finally peaked two weeks ago after falling by 54 homes in the past two weeks, the second largest drop this year behind the end of March. Expect the inventory to fall along the same trajectory as 2022 and start 2025 similar to the January 1, 2023 level.

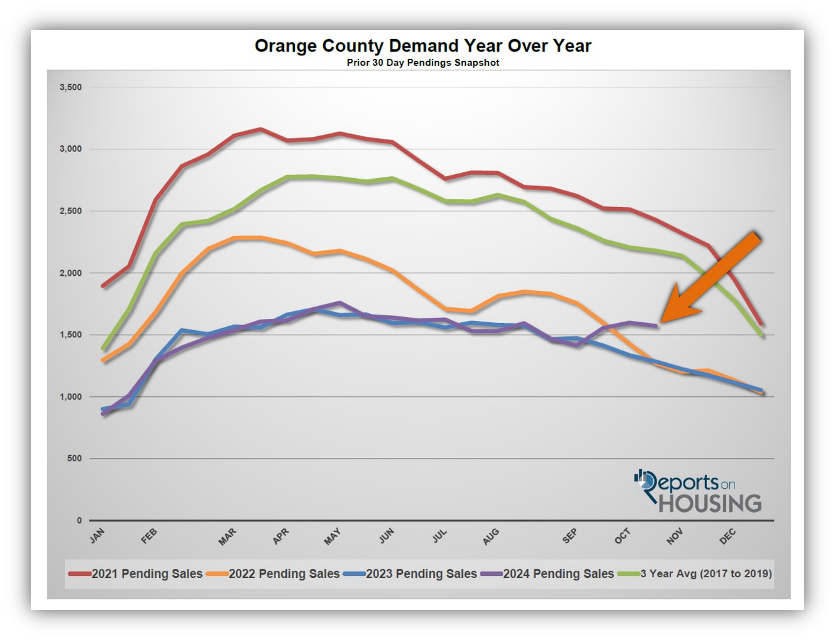

- Negotiations have shifted more toward the buyer’s favor as the year winds down. The Expected Market Time dropped to 37 days at the end of March. Back then, homes flew off the market with multiple offers and plenty of showing activity. Flash forward to today, and the Expected Market Time has risen to 69 days. It was 78 days in September but improved as the sub-6.5% mortgage rates worked through the market. Yet, with rates back up to 7%, expect the market to slow a bit from here.

Since the end of March, the inventory has increased from 2,010 homes to 3,640 today, up 81% or 1,630 additional homes. At the same time, demand has fallen from 1,617 pending sales to 1,572 today, down 3%. With the inventory surging higher and demand slowly falling, the speed of the market has slowed substantially since spring. As a result, many homes are languishing on the market without success. An eye-opening 35% of the active inventory has reduced the asking price at least once. The median price drop is 4.43%. That is equivalent to a reduction from $1,000,000 to $955,700. The number of sellers who have thrown in the towel and pulled their homes off the market due to a lack of success is up 27% through today, an additional 900.

This is the most buyer-friendly market since the end of 2022 when rates were screaming higher. There are more choices, along with sellers who have been on the market for much longer. The longer sellers remain on the market, the more apt they are to negotiate and accept a buyer’s terms.

The bottom line: steer clear of all the hype, narratives, and differing market views. Instead, lean in on data, statistics, and trendlines and continue to look for changes. Let the data speak for itself and allow it to set market expectations properly.

Active Listings

It appears as if the inventory finally peaked.

The active listing inventory decreased by 54 homes in the past two weeks, down 1%, and now sits at 3,640, its lowest level since August. Last year’s peak did not come until November 9th, four weeks later than this year, at 2,496 homes. The big difference is that mortgage rates were much higher last year, eclipsing 8% in October. This year’s peak of 3,694 is 48% higher than last year. Expect the inventory to plunge until New Year’s Day, like last year. The start of 2025 will be similar to 2023, with around 2,400 homes, 48% higher than the start of this year. The inventory will fall due to the fewest homes placed on the market in November and December, along with many unsuccessful sellers pulling their homes off the market to enjoy the holiday season.

Last year, the inventory was 2,406 homes, 34% lower, or 1,234 fewer. The 3-year average before COVID (2017 through 2019) was 6,010, an additional 2,370 homes, or 65% more.

Homeowners continue to “hunker down” in their homes, unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. It became a crisis once rates skyrocketed higher in 2022. For September, 2,286 new sellers entered the market in Orange County, 743 fewer than the 3-year average before COVID (2017 to 2019), 25% less. Last September, there were 1,963 new sellers, 14% fewer than this year. More sellers are opting to sell compared to the previous year.

Demand

Demand decreased by 2% in the past couple of weeks.

Demand, a snapshot of the number of new pending sales over the prior month, decreased from 1,598 to 1,572 in the past couple of weeks, down 26 pending sales, or 2%. October has not been a good month for rates for the past couple of years. Rates peaked in October 2022 at 7.37% after starting the year at 3.25%. Last year, they eclipsed 8% on hotter-than-expected economic readings similar to this October. Expect demand to continue to erode, as is customary for this time of year, unless there is a sudden change in the economic data and rates unexpectedly dip to close out the year. If rates were to return to below 6.5% with duration sometime in the future, the market would finally thaw. Until then, expect continued sluggish demand.

As the Federal Reserve has indicated, it is essential to watch all economic releases for signs of slowing. These releases can potentially move mortgage rates higher or lower, depending on how they compare to market expectations. This week is a very important week for rates. It is jobs week, with readings on the number of job openings, jobs created, and the current unemployment rate. In addition, another inflation gauge, the Personal Consumption Expenditures Index, will be released on Wednesday.

Last year, demand was 1,284, down 288 pending sales or 18%. The 3-year average before COVID (2017 to 2019) was 2,180 pending sales, 39% more than today, or an additional 608.

With supply and demand falling at similar rates, the Expected Market Time (the number of days it takes to sell all Orange County listings at the current buying pace) remained unchanged at 69 days in the past couple of weeks. Last year, it was 56 days, faster than today. The 3-year average before COVID was 85 days, slower than today.

Luxury End

The luxury market slowed in the past couple of weeks.

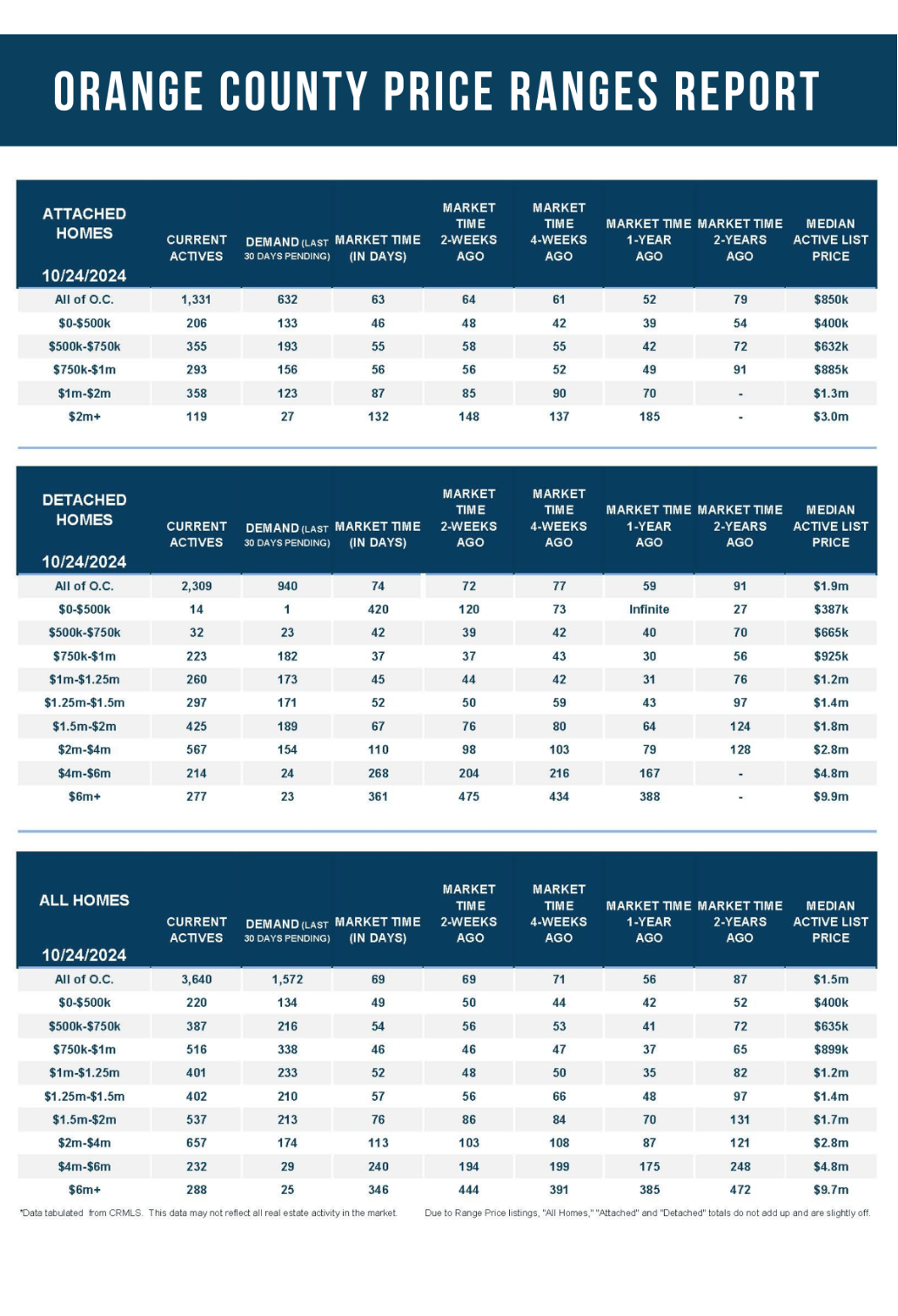

In the past couple of weeks, the luxury inventory of homes priced above $2 million (the top 10% of the Orange County housing market) decreased from 1,192 to 1,177 homes, down 15 or 1%. Luxury demand decreased by 22 pending sales, down 9%, and now sits at 228, its lowest reading since mid-July. With demand plunging compared to the slight drop in the inventory, the Expected Market Time for luxury homes priced above $2 million increased from 143 to 155 days. The luxury market is sluggish and necessitates a careful, methodical approach to pricing.

Year over year, the active luxury inventory is up by 370 homes or 46%, and luxury demand is up by 36 pending sales or 19%. Last year’s Expected Market Time was 126 days, faster than today.

In the past two weeks, the expected market time for homes priced between $2 million and $4 million increased from 103 to 113 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 194 to 240 days. For homes priced above $6 million, the Expected Market Time decreased from 444 to 346 days. At 346 days, a seller would be looking at placing their home into escrow around October 2025.

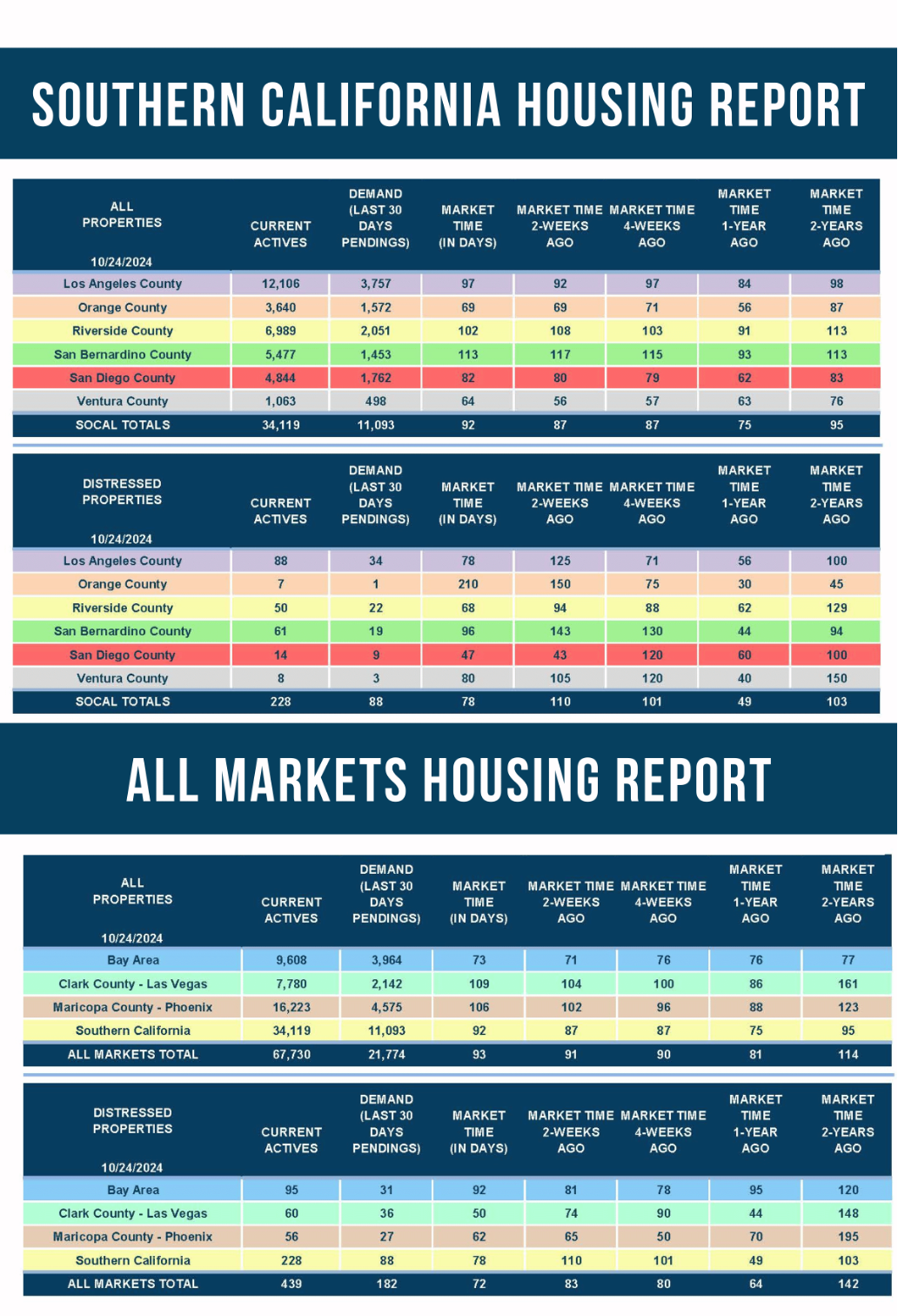

Orange County Housing Summary

- The active listing inventory in the past couple of weeks decreased by 54 homes, down 1%, and now sits at 3,640, its lowest level since August. It appears as if Orange County reached its annual peak at 3,694 homes two weeks ago. In September, 25% fewer homes came on the market compared to the 3-year average before COVID (2017 to 2019), 743 less. Yet, 323 more sellers came on the market this September compared to September 2023. Last year, there were 2,406 homes on the market, 1,234 fewer homes, or 34% less. The 3-year average before COVID (2017 to 2019) was 6,010, or 65% extra.

- Demand, the number of pending sales over the prior month, decreased by 26 pending sales in the past two weeks, down 2%, and now totals 1,572. Last year, there were 1,284 pending sales, 18% fewer. The 3-year average before COVID (2017 to 2019) was 2,180, or 39% more.

- With supply and demand falling at a similar pace, the Expected Market Time, the number of days to sell all Orange County listings at the current buying pace, remained unchanged at 69 days in the past couple of weeks. The 3-year average before COVID (2017 to 2019) was 85 days, slower than today.

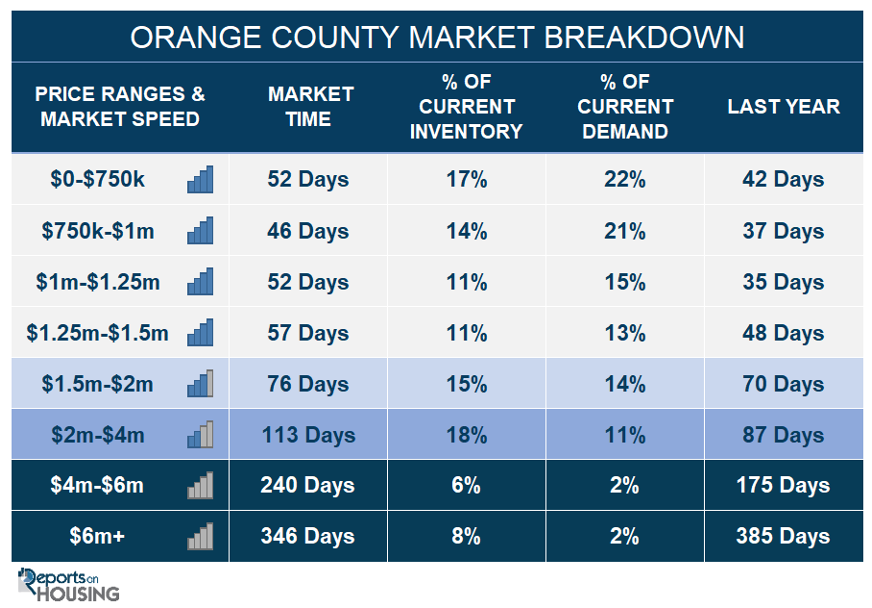

- In the past two weeks, the Expected Market Time for homes priced below $750,000 decreased from 53 to 52 days. This range represents 17% of the active inventory and 22% of demand.

- The Expected Market Time for homes priced between $750,000 and $1 million remained unchanged at 46 days. This range represents 14% of the active inventory and 21% of demand.

- The Expected Market Time for homes priced between $1 million and $1.25 million increased from 48 to 52 days. This range represents 11% of the active inventory and 15% of demand.

- The Expected Market Time for homes priced between $1.25 million and $1.5 million increased from 56 to 57 days. This range represents 11% of the active inventory and 13% of demand.

- The Expected Market Time for homes priced between $1.5 million and $2 million decreased from 86 to 76 days. This range represents 15% of the active inventory and 14% of demand.

- In the past two weeks, the expected market time for homes priced between $2 million and $4 million increased from 103 to 113 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 194 to 240 days. For homes priced above $6 million, the Expected Market Time decreased from 444 to 346 days.

- The luxury end, all homes above $2 million, account for 32% of the inventory and 15% of demand.

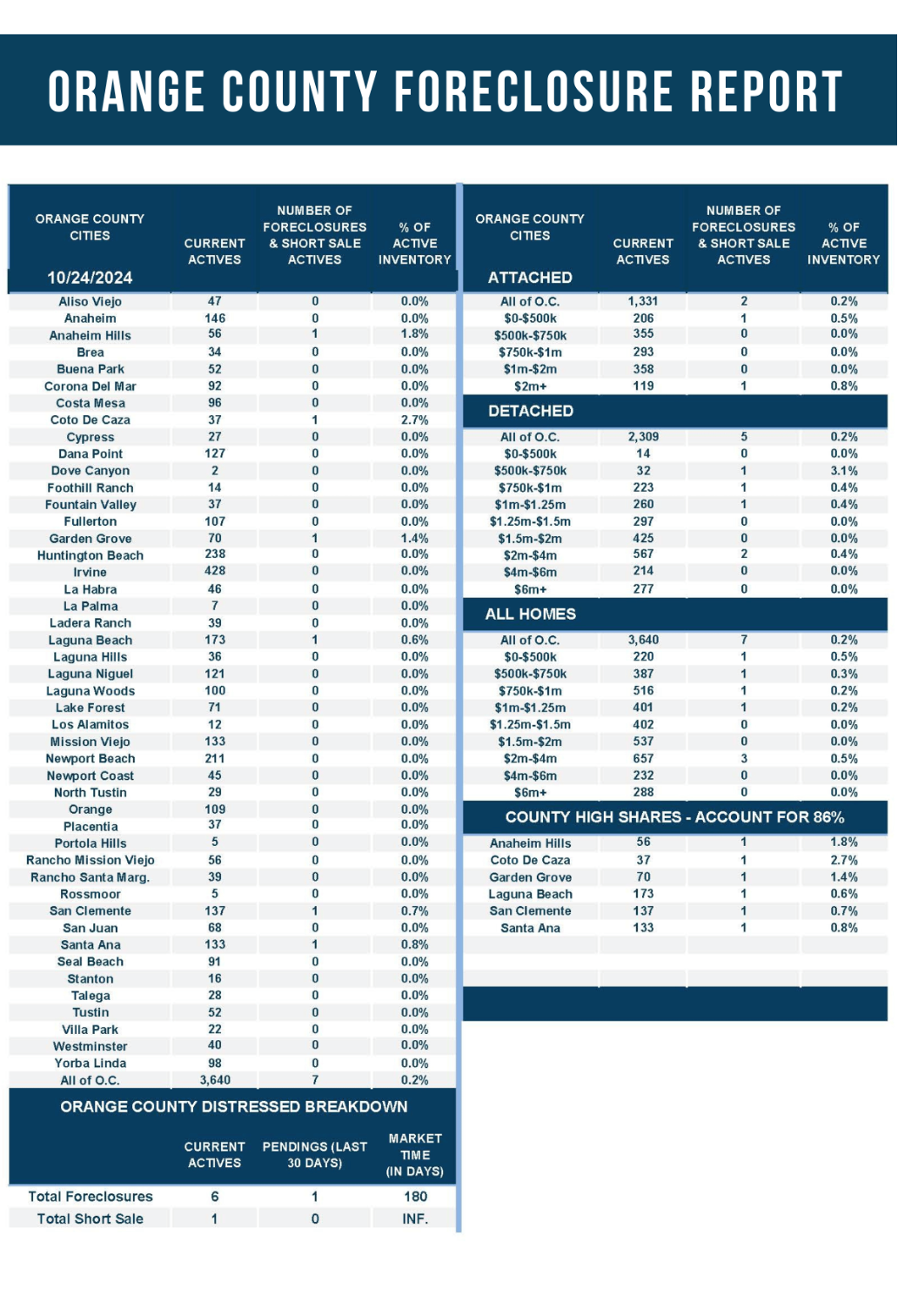

- Distressed homes, both short sales and foreclosures combined, comprised only 0.2% of all listings and 0.1% of demand. Only six foreclosures and one short sale are available today in Orange County, with seven total distressed homes on the active market, up two from two weeks ago. Last year, four distressed homes were on the market, similar to today.

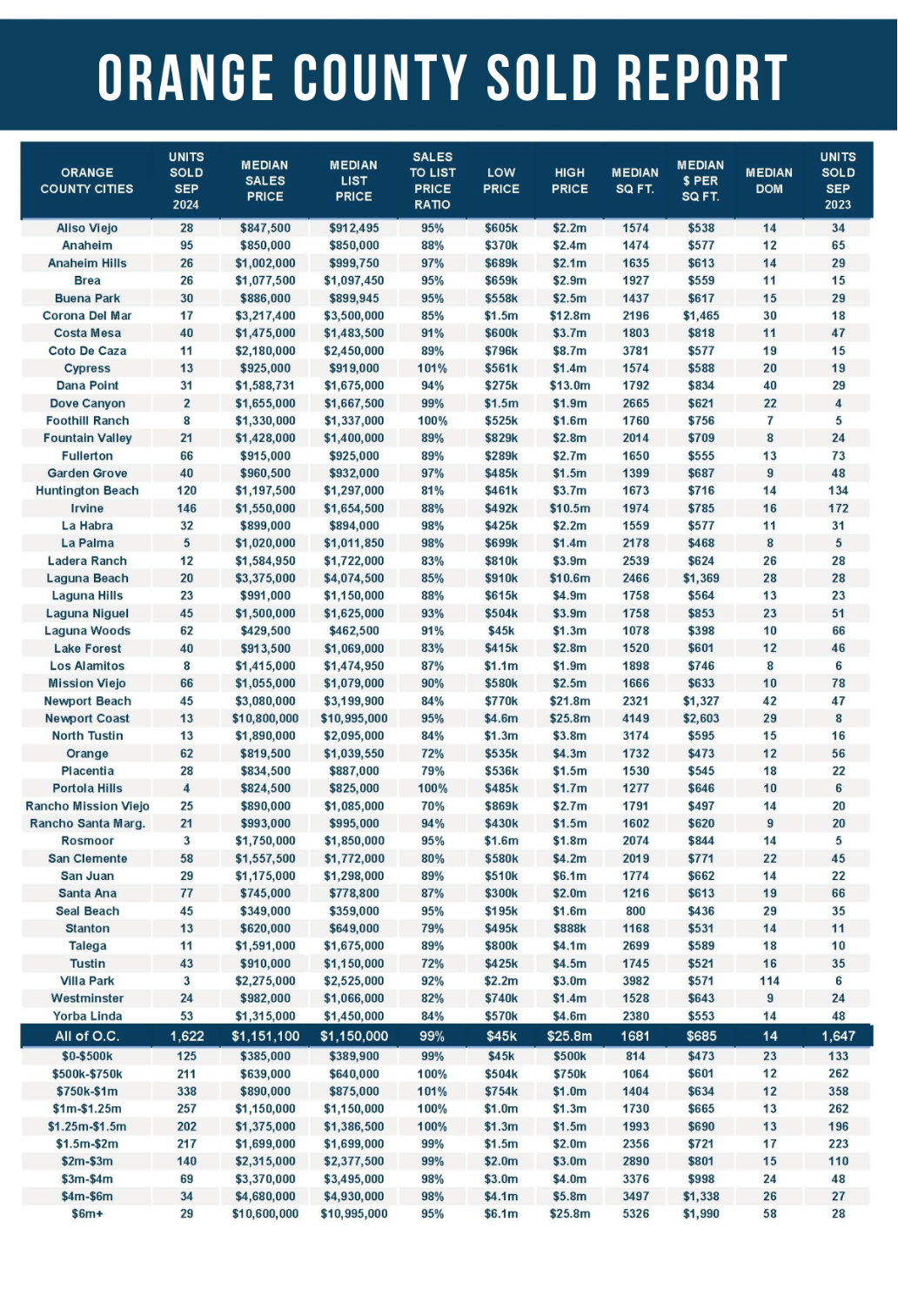

- There were 1,622 closed residential resales in September, down 2% compared to September 2023’s 1,647 and down 14% from August 2024. The sales-to-list price ratio was 98.9% for Orange County. Foreclosures accounted for 0.1% of all closed sales, and there were no short sales. That means that 99.9% of all sales were good ol’ fashioned sellers with equity.

Have a great week.

Sincerely,

Steven Thomas

Quantitative Economics and Decision Sciences

Copyright 2024—Steven Thomas, Reports On Housing—All Rights Reserved. This report may not be reproduced in whole or in part without express written permission from the author.