August 5, 2024

Mortgage rates have plunged from 7.5% in April to 6.34% today, opening up a window of opportunity for buyers who should not wait.

A Window of Opportunity

Since rates have dropped in anticipation of future Federal Reserve rate cuts, now is the ideal time, and waiting will prove to be the incorrect strategy.

Olympic gold medal winners perfect their game plans and execute precise timing and strategy to succeed. On the track, many runners wait too long for their final push and cross the finish line out of medal contention. The commentators exclaim that they “should have gone sooner.” The athletes are left second-guessing themselves, wishing they had not waited.

Many buyers have been sitting on the sidelines, waiting for rates to come down. Now that rates have plummeted from 7.5% in April to 6.34% today, according to Mortgage News Daily, many buyers wonder if they should pull the trigger and purchase now or wait for rates to fall further. Sitting on the fence and waiting will prove to be the incorrect strategy, leaving many to wish that they had bought sooner.

Long-term, 30-year mortgage rates move ahead of the Federal Reserve Rate cuts. The Federal Reserve (Fed) has not cut rates once since the historical increases from 2022 through 2023, yet mortgage rates have moved all over the place, even eclipsing 8% last October. The movement is based on where investors believe the direction that the Fed’s short-term Federal Funds rate policy will move.

With inflation continuing to ease, the job market cooling, and unemployment rising, it is becoming increasingly clear that the FED is too restrictive, and they will need to cut rates when they meet in mid-September. As a result, in less than two weeks, mortgage rates have plunged from 6.91% to 6.34% today. September’s rate cut, currently projected to be a 0.5% snip by Wall Street, is already baked into today’s mortgage rates. When they do trim the Federal Funds rate in September, do NOT expect mortgage rates to drop another 0.5%. This is where buyers sitting on the sidelines are mistaken. They hear that the Fed will cut, but the headlines and news refer to the short-term Federal Funds rate, not long-term mortgage rates. When they do cut, expect credit card, automobile, and equity lines of credit rates to all drop, which are all tied to the Federal Funds rate, but NOT long-term rates utilized in purchasing homes.

Can long-term rates go lower? Yes, they can. But today’s mortgage rates are already factoring in future cuts totaling 1.25%. If the economy cools even more, which the trends in the data currently support, expect rates to fall further next year. Yet, with the recent plunge, affordability has improved dramatically. More potential buyers qualify. Buyers already in the marketplace have witnessed their purchasing power increase; they can now afford a much higher-priced home. With improving affordability, demand will rise just as the inventory is about to reach its summer peak and begin to fall. As demand increases and supply falls, market times will drop. There will be more buyer competition, and values will rise again from here.

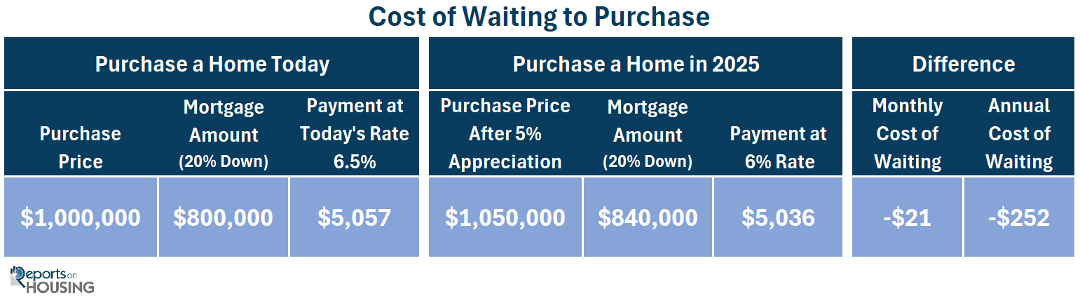

For a buyer looking to purchase a $1 million home today with 20% down and a 6.5% rate, the principal and interest payment would be $5,057. Due to a further constrained inventory and increased demand, values are anticipated to rise at least 5%. That $1 million home would appreciate to $1,050,00. Even if rates drop to 6%, the monthly payment would be

$5,036, nearly identical to today’s payment at 6.5%. It is only $21 less per month or $252 annually. In waiting, the buyer loses out on $50,000 appreciation and is looking at a $10,000 additional down payment.

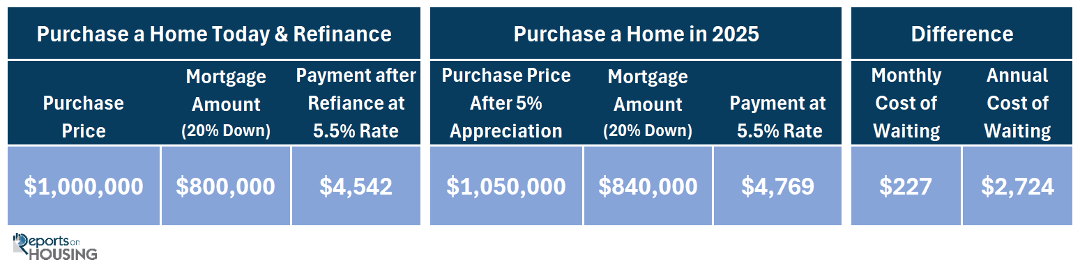

What if 30-year rates drop to 5.5%? Isn’t it better to wait until that occurs? There is a rule of thumb when it comes to refinancing: when mortgage rates drop by 1% or more from the current locked-in, fixed rate, then it is an excellent time to refinance. The buyer that purchases a $1 million home today could refinance next year if rates fall to 5.5%. The monthly payment would drop from $5,057 to $4,542, a savings of $515 every month or $6,180 annually.

For the buyer who waits to purchase until next year, the $1 million home is anticipated to appreciate at least 5% to $1,050,000. The monthly payment would be $4,769. That is $227 per month higher or $2,724 annually compared to purchasing now and refinancing once rates drop to 5.5%. In addition, waiting requires an extra $10,000 in down payment, and the buyer once again misses out on $50,000 in appreciation.

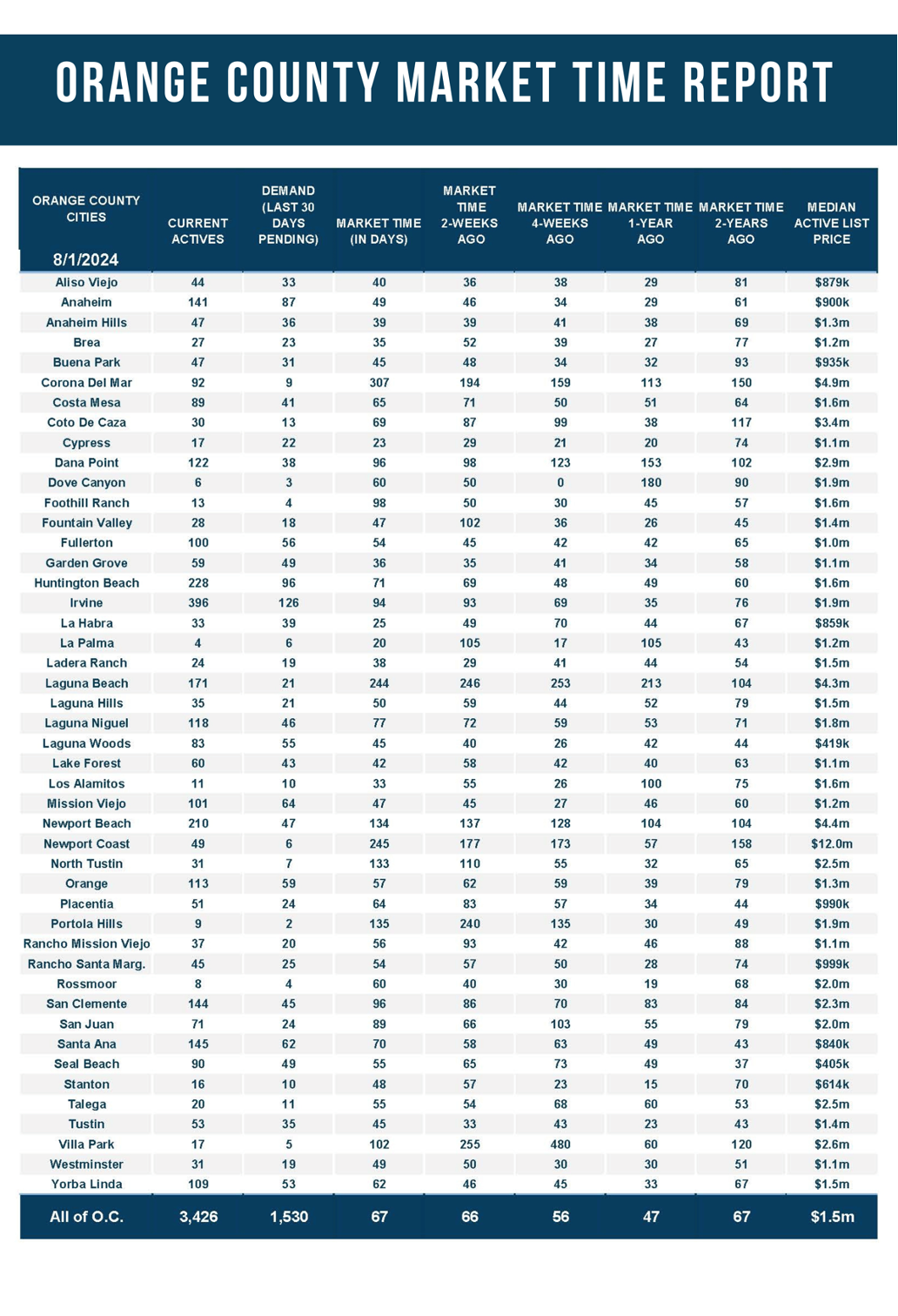

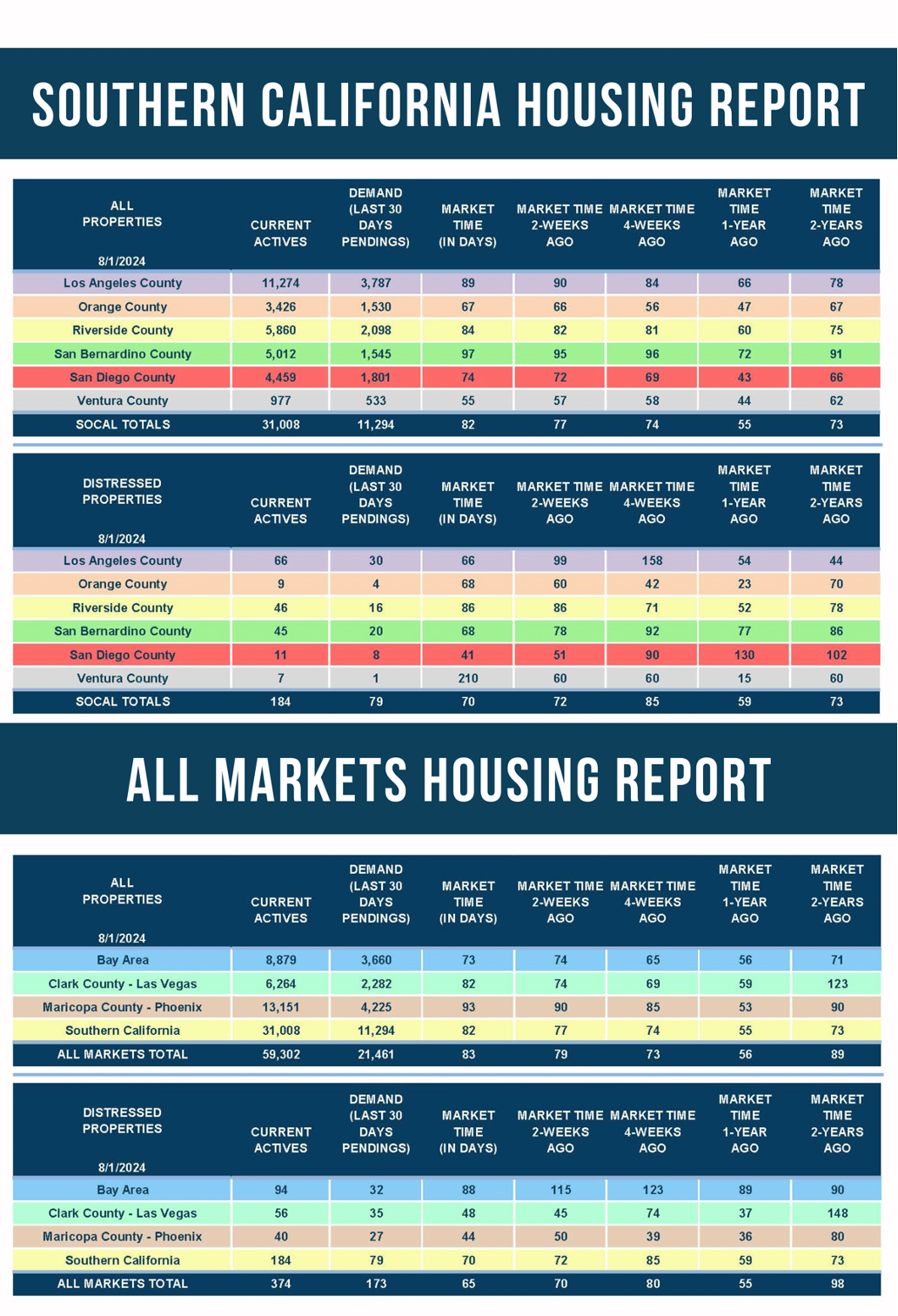

Today is already one of the best times to purchase in the past couple of years. The Orange County inventory is at 3,426, up 28% or 951 homes compared to last year. There are way more choices in every price range. Demand, a snapshot of the number of new pending sales over the prior month, is at 1,530, down 3% compared to last year, 50 fewer pending sales. With much higher inventory levels and demand on par with the previous year, the Expected Market Time, the number of days it takes to sell all Orange County listings at the current buying pace, is 67 days, much slower than last year’s 47-day speed. As rates remain at these low levels with duration, expect the inventory to fall, demand to rise, and the Expected Market Time to drop for the remainder of the year.

The most favorable condition for buyers is NOW. Just like so many Olympic athletes crossing the finish line first, it is time for buyers to make that gold medal decision and pull the trigger now. Do not wait.

Active Listings

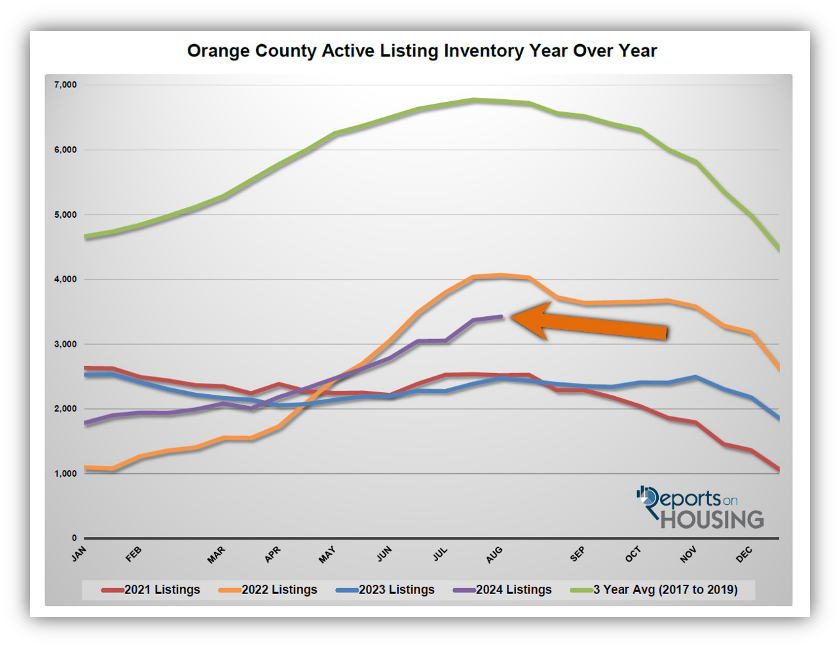

The active inventory increased by 2% in the past couple of weeks.

The active listing inventory increased by 55 homes in the past two weeks, up 2%, and now sits at 3,426, its highest level since November 2022. With rates dropping and demand anticipated to accelerate in the coming weeks, expect the Orange County inventory to reach its annual peak at its typical time between July and August. As the inventory is reaching its peak, the inventory climbs at a much slower pace. After reaching its peak, expect the inventory to fall slowly. As demand accelerates with easing rates, the inventory has a high likelihood of dropping at a faster pace than usual. Combine the Autumn Market drop with the end-of-the-year Holiday Market plunge, and 2024 inventory levels could reach very anemic levels upon ushering in a New Year.

Last year, the inventory was 2,475 homes, 28% lower, or 951 fewer. The 3-year average before COVID (2017 through 2019) was 6,753, an additional 3,327 homes, or 97% more, nearly double the current level. This difference illustrates that the inventory crisis is still impacting Orange County housing.

Homeowners continue to “hunker down” in their homes, unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. It became a crisis once rates skyrocketed higher in 2022. For July, 2,711 new sellers entered the market in Orange County, 996 fewer than the 3-year average before COVID (2017 to 2019), 27% less. Last July, there were 2,270 new sellers, 16% fewer than this year. More sellers are opting to sell compared to last year.

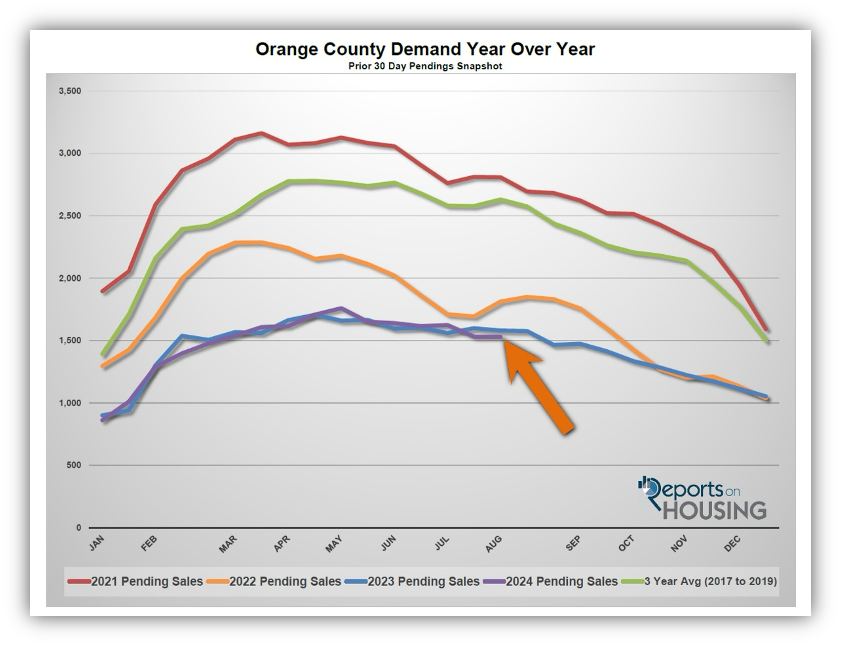

Demand

Demand remained unchanged in the past couple of weeks.

Demand, a snapshot of the number of new pending sales over the prior month, decreased from 1,531 to 1,530 in the past couple of weeks, down one pending sale, nearly unchanged. Demand has remained at incredibly anemic, inherent levels since October 2022. There are always buyers willing to purchase. With the high mortgage rate environment, rates stuck around 7% or higher for the better part of a year now, very few buyers have been willing to participate. That is why 2024 demand levels have remained very close to last year’s. Yet, since the end of July, rates have dropped from 6.91% to a low of 6.34% today, according to Mortgage News Daily. That is the lowest rate in 16 months since April 2023. A year ago, rates rose from 7% at the end of July to 8% in October. This year, mortgage rates are improving affordability and will ultimately drive more demand. Expect demand to rise in the coming weeks, instigated by more buyers who now qualify

and an increase in buyers’ purchasing power. Buyers who were already looking to purchase a home can suddenly purchase a higher priced home with no change in payment. Expect more buyer competition chasing a falling supply for the remainder of the year.

As the Federal Reserve has indicated, watching all economic releases for signs of slowing is essential. These releases can potentially move mortgage rates higher or lower, depending on how they stack up compared to market expectations. There are not too many economic releases until next week, when the Consumer Price Index will be released on Wednesday, and U.S. retail sales will be released on Thursday. Both have a high potential to move mortgage rates.

Last year, demand was 1,580, 3% more than today, or 50 additional pending sales. The 3-year average before COVID (2017 to 2019) was 2,630 pending sales, 72% more than today, or an additional 1,100.

With supply rising and demand unchanged, the Expected Market Time (the number of days it takes to sell all Orange County listings at the current buying pace) increased from 66 to 67 days in the past couple of weeks. Last year, it was 47 days, faster than today. The 3-year average before COVID was 78 days, a bit slower than today.

Luxury End

The luxury market has not changed much in the past couple of weeks.

In the past couple of weeks, the luxury inventory of homes priced above $2 million increased from 1,188 to 1,206 homes, up 18 or 2%, the highest level since October 2019. Luxury demand increased by six pending sales, up 3%, and now sits at 232. With demand rising slightly faster than demand, the Expected Market Time for luxury homes priced above $2 million decreased from 158 to 156 days. The luxury market feels exceptionally sluggish compared to the lower ranges. The higher the price, the longer it takes to secure success. Typically, financial market volatility impacts the velocity of luxury. If Wall Street does not recover quickly, expect the luxury market to slow further.

Year over year, the active luxury inventory is up by 413 homes or 52%, and luxury demand is up by 16 pending sales or 7%. Last year’s Expected Market Time was 110 days, much faster than today.

In the past two weeks, the expected market time for homes priced between $2 million and $4 million decreased from 116 to 114 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 156 to 170 days. For homes priced above $6 million, the Expected Market Time increased from 630 to 656 days. At 656 days, a seller would be looking at placing their home into escrow around May 2026.

Orange County Housing Summary

- The active listing inventory in the past couple of weeks increased by 55 homes, up 2%, and now sits at 3,426, its highest level since November 2022. In July, 27% fewer homes came on the market compared to the 3-year average before COVID (2017 to 2019), 996 less. Yet, 441 more sellers came on the market this July compared to July 2023. Last year, there were 2,475 homes on the market, 951 fewer homes, or 28% less. The 3-year average before COVID (2017 to 2019) was 6,753, or 97% extra, nearly double.

- Demand, the number of pending sales over the prior month, decreased by one pending sale in the past two weeks, nearly unchanged, and now totals 1,530, still its lowest level since February. Last year, there were 1,580 pending sales, 3% more. The 3-year average before COVID (2017 to 2019) was 2,630, or 72% more.

- With supply climbing and demand unchanged, the Expected Market Time, the number of days to sell all Orange County listings at the current buying pace, increased from 66 to 67 days in the past couple of weeks. It was 47 days last year, faster than today. The 3-year average before COVID (2017 to 2019) was 78 days, a bit slower than today.

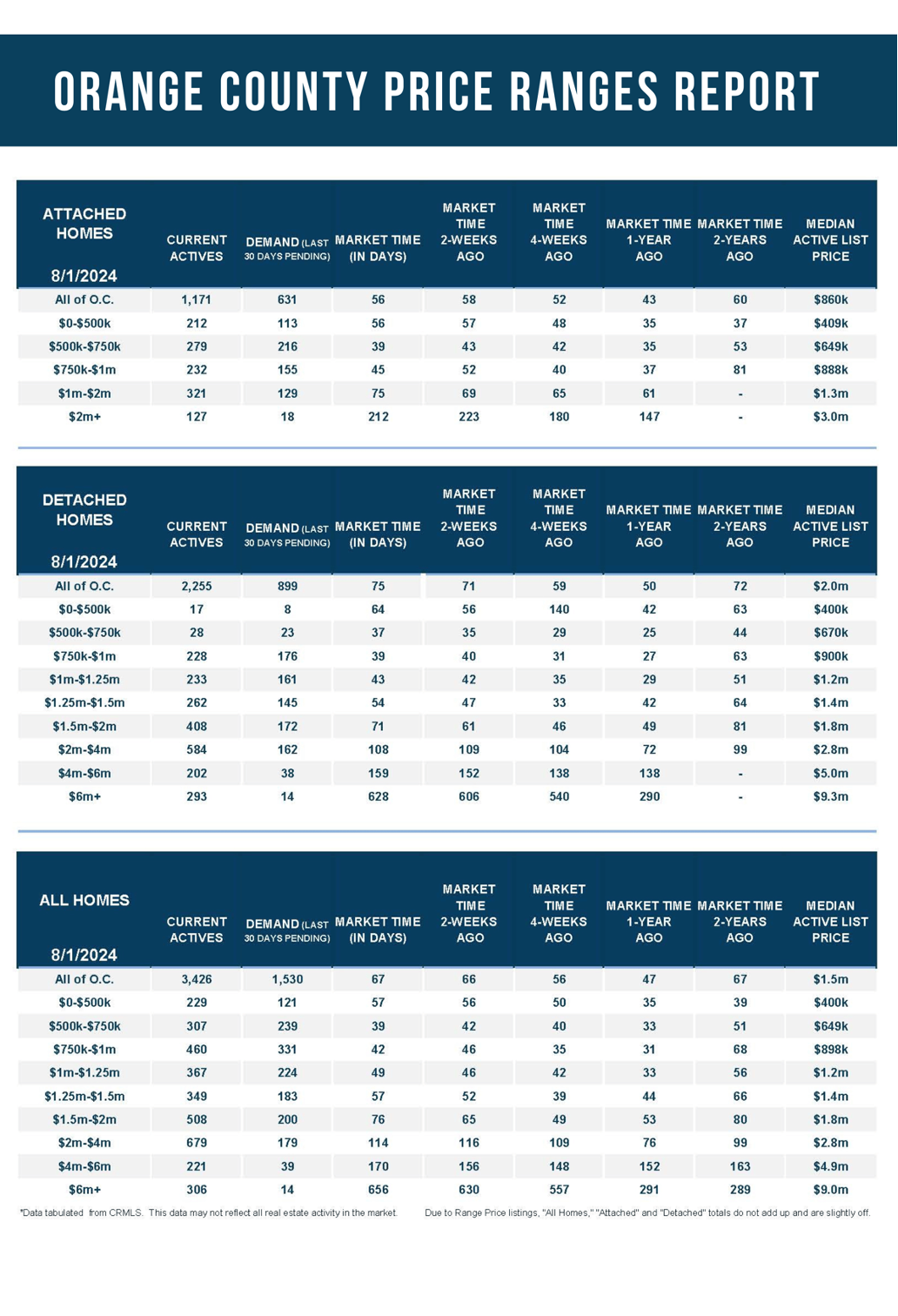

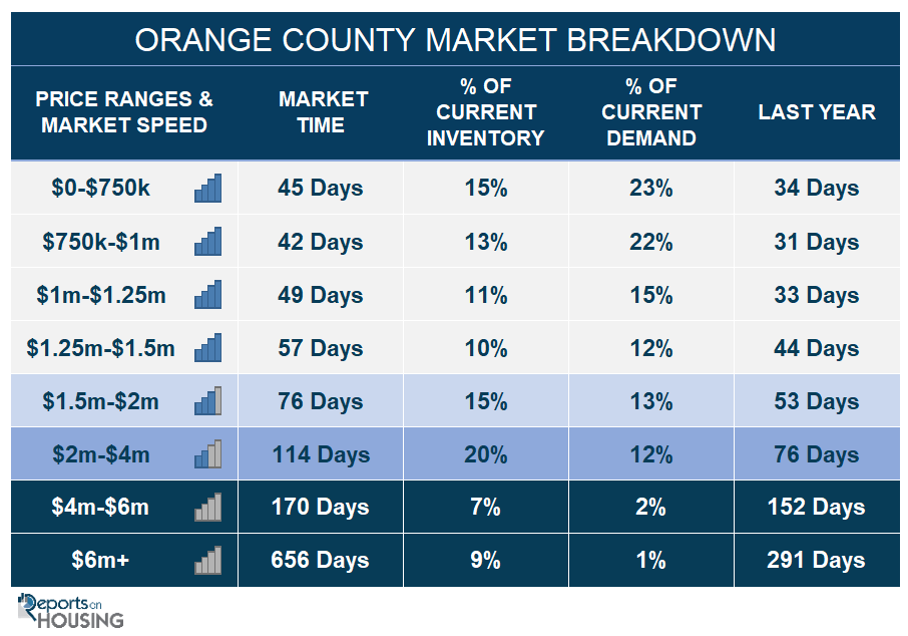

- In the past two weeks, the Expected Market Time for homes priced below $750,000 decreased from 47 to 45 days. This range represents 15% of the active inventory and 23% of demand.

- The Expected Market Time for homes priced between $750,000 and $1 million decreased from 46 to 42 days. This range represents 13% of the active inventory and 22% of demand.

- The Expected Market Time for homes priced between $1 million and $1.25 million increased from 46 to 49 days. This range represents 11% of the active inventory and 15% of demand.

- The Expected Market Time for homes priced between $1.25 million and $1.5 million increased from 52 to 57 days. This range represents 10% of the active inventory and 12% of demand.

- The Expected Market Time for homes priced between $1.5 million and $2 million increased from 65 to 76 days. This range represents 15% of the active inventory and 13% of demand.

- In the past two weeks, the expected market time for homes priced between $2 million and $4 million decreased from 116 to 114 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 156 to 170 days. For homes priced above $6 million, the Expected Market Time increased from 630 to 656 days.

- The luxury end, all homes above $2 million, account for 36% of the inventory and 15% of demand.

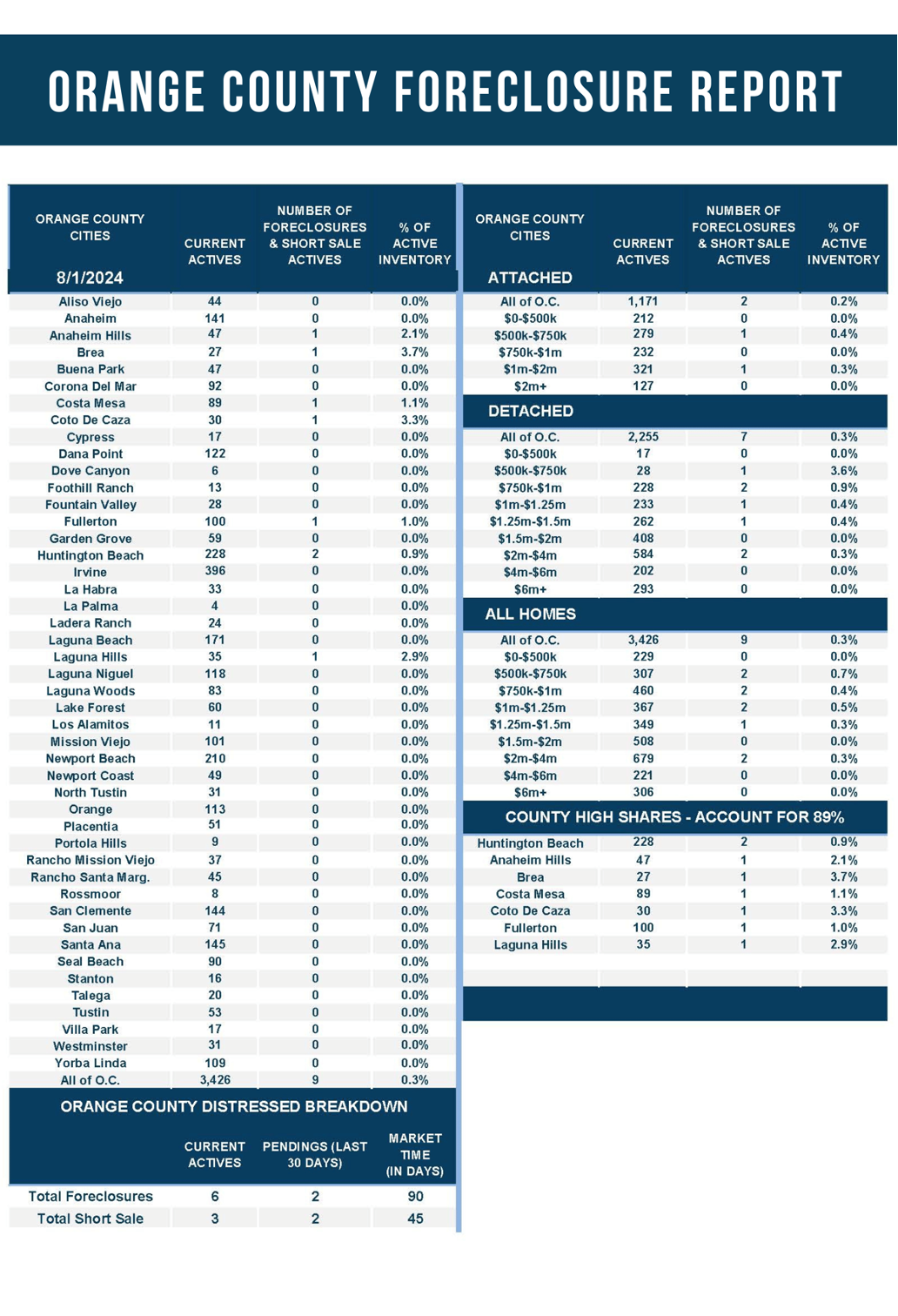

- Distressed homes, both short sales and foreclosures combined, comprised only 0.3% of all listings and 0.3% of demand. Only six foreclosures and three short sales are available today in Orange County, with nine total distressed homes on the active market, up one from two weeks ago. Last year, seven distressed homes were on the market, similar to today.

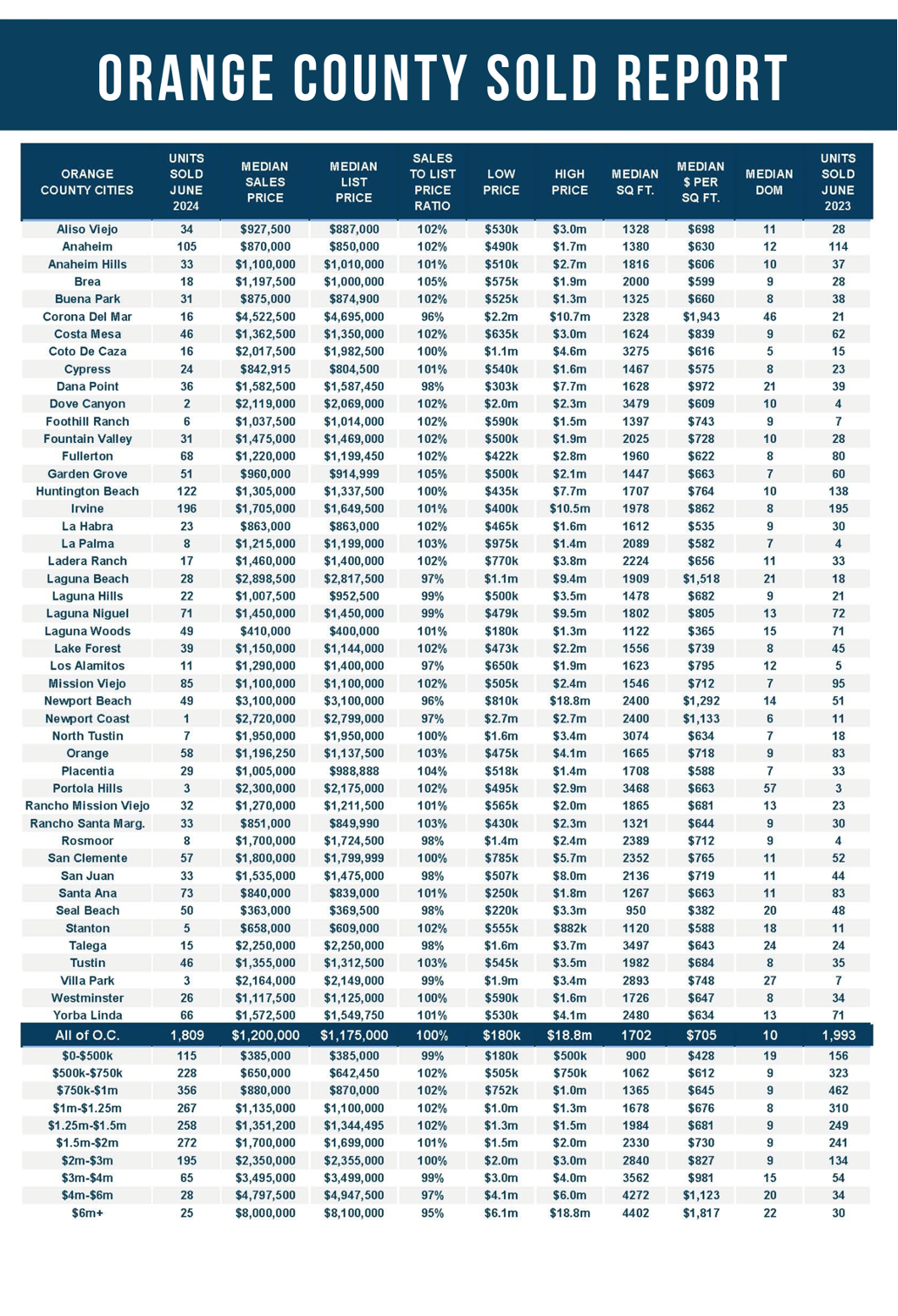

- There were 1,809 closed residential resales in June, down 9% compared to June 2023’s 1,993 and down 15% from May 2024. The sales-to-list price ratio was 100.3% for Orange County. Short sales accounted for 0.1% of all closed sales and no foreclosures. That means that 99.89% of all sales were good ol’ fashioned sellers with equity.

Have a great week.

Sincerely,

Steven Thomas

Quantitative Economics and Decision Sciences

Copyright 2024—Steven Thomas, Reports On Housing—All Rights Reserved. This report may not be reproduced in whole or in part without express written permission from the author.