November 12, 2024

With so many varying viewpoints and narratives swirling about the housing market, it is best to take a step back from the noise and focus on the latest trends.

Meticulously Arriving at Price

Setting an accurate, initial asking price is one of the most critical steps in a seller securing an interested buyer and achieving a successful outcome of the sale of their home.

It takes months of preparation and a detailed step-by-step approach for anyone looking to run a marathon for the first time. Most marathon training plans range from 12 to 20 weeks, with the weekly mileage ramping up steadily until peaking at 20+ mile runs. The long, arduous process includes proper nutrition, appropriate footwear, plenty of stretching, good rest, and putting in miles and miles of workouts three to five times per week. The occasional runner who opts to show up to the starting line of their first marathon with very little training and forethought will probably not finish, and the risks of injury are high.

For the homeowner looking to sell their home, it takes careful preparation and a step-by-step approach, just like the first-time marathoner. Addressing deferred maintenance, from a fresh coat of paint to new light fixtures to new flooring, is essential in enhancing a home’s allure. Sprucing up the curb appeal with topsoil, flowers, new plants, and a fresh coat of paint on the garage and front doors may be an additional necessary step. This attention to detail is often suggested by a seasoned, carefully chosen, professional REALTOR®. The goal is to maximize a seller’s net proceeds with a successful closed sale. The final and most important crucial step is to arrive at the asking price.

Arriving at the ultimate asking price is not guesswork. There is no need to pad the price for future negotiations, which will ultimately lead to becoming overpriced without success. Additionally, sellers wishing to “test the market” in today’s much slower-paced housing market will languish for quite some time, unable to cross the finish line. The best approach is to spend as much time as is needed to carefully consider all recent pending and closed sales.

Buyers are savvy. They will scrutinize every detail of a home before climbing in a car to take a closer look at a home: the pictures, virtual tours, condition, upgrades, amenities, style, curb appeal, age, location, and, most importantly, its price. Price is the most critical first impression. Sellers only get one shot at making that first impression. After the initial seven to ten days, most buyers have “seen” the home. Armed with their favorite real estate app, they initially tour the home electronically. They then decide to either schedule a showing appointment or move on and wait for the next home that pops up. The longer a home is on the market, the less fanfare and excitement it receives. Even if a seller reduces the asking price down the road, it is not met with eager buyer anticipation and enthusiasm like it does when it first hits the market. Currently, 35% of today’s active listing inventory has reduced the asking price at least once.

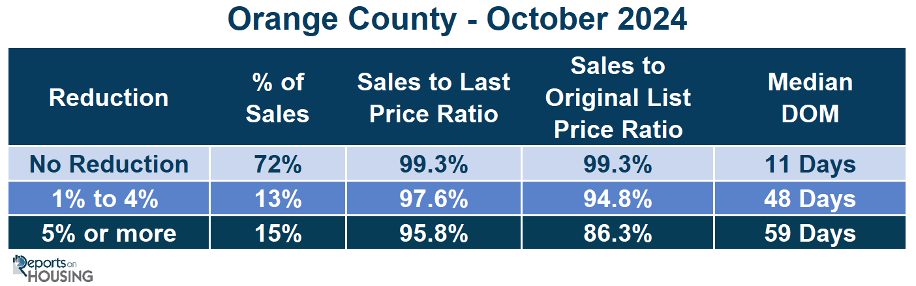

Yet, the data illustrates that starting overpriced, requiring a reduction to secure success, results in the seller walking away with a smaller net proceeds check. The sales price to last list price ratio is very revealing. This refers to the final list price before becoming a pending sale. These are averages, meaning there are exceptions, but the overall trend is eye-opening. In Orange County, 72% of all closed sales in October did not reduce the asking price. It was 88% in May. The sales price to last list price ratio for these homes was 99.3%, meaning, on average, a home appropriately priced sold close to its

initial asking price. A house listed at $1 million sold for $993,000, $7,000 below the asking price. The median days on the market before becoming a pending sale was only 11, indicating that accurate pricing also means considerably less time on the market.

13% of all closed sales reduced their asking prices between 1% and 4%. The sales-to-last list price ratio for these homes was 97.6%; on average, it took 48 days to become a pending sale. A house that reduced its list price to $1 million sold for $976,000, a substantial $17,000 less than homeowners with no reduction.

For homes that reduced their asking prices by 5% or more, 15% of closed sales in October, the sales-to-last list price ratio was 95.8% after being on the market for 59 days. A home that finally reduced its price to $1 million sold for $958,000, a staggering $35,000 less than homeowners who did not need to reduce the asking price.

The sales price to original list price ratio reveals how far off many sellers are in considering a home’s actual market value. This is the price of a home when it initially comes on the market before any price reductions. For homes that reduced the asking price between 1% to 4%, the sales price to original list price ratio was 94.8%. For example, a house initially listed at $1,030,000 had to reduce the asking price to $1 million to secure success and ultimately sold for $976,000, an astonishing $54,000 less the original price.

Homes that reduced the asking price by at least 5% had a sales-to-original list price ratio of 86.3%. A house initially listed at $1,110,000 had to lower the asking price, often more than once, to $1 million to find success, and ultimately sold for $958,000. That is an overwhelming $152,000 less than the original asking price.

The data is loud and clear. For sellers to net as much as possible at the closing table, it is essential to carefully arrive at a home’s Fair Market Value no matter how much time and effort it takes. It is wiser to spend hours sifting through all the most recent comparable pending and closed sales, carefully considering a home’s condition, upgrades, amenities, and location, than to linger on the market without success, left with a decision to reduce the asking price or throw in the towel and pull the home off the market. In other words, the most successful home-selling approach is meticulously arriving at the initial asking price.

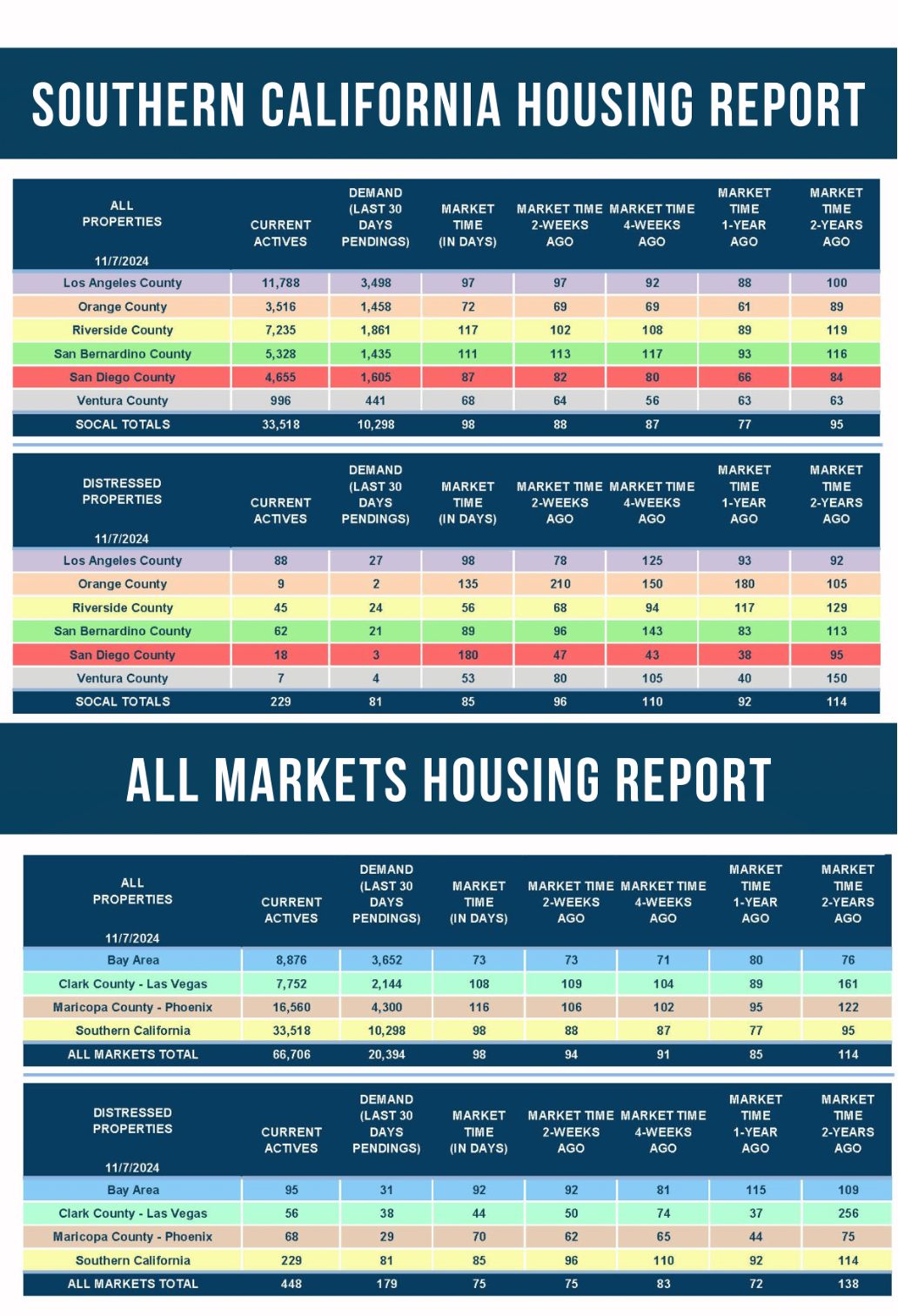

Active Listings

The inventory will continue to fall until the beginning of the New Year.

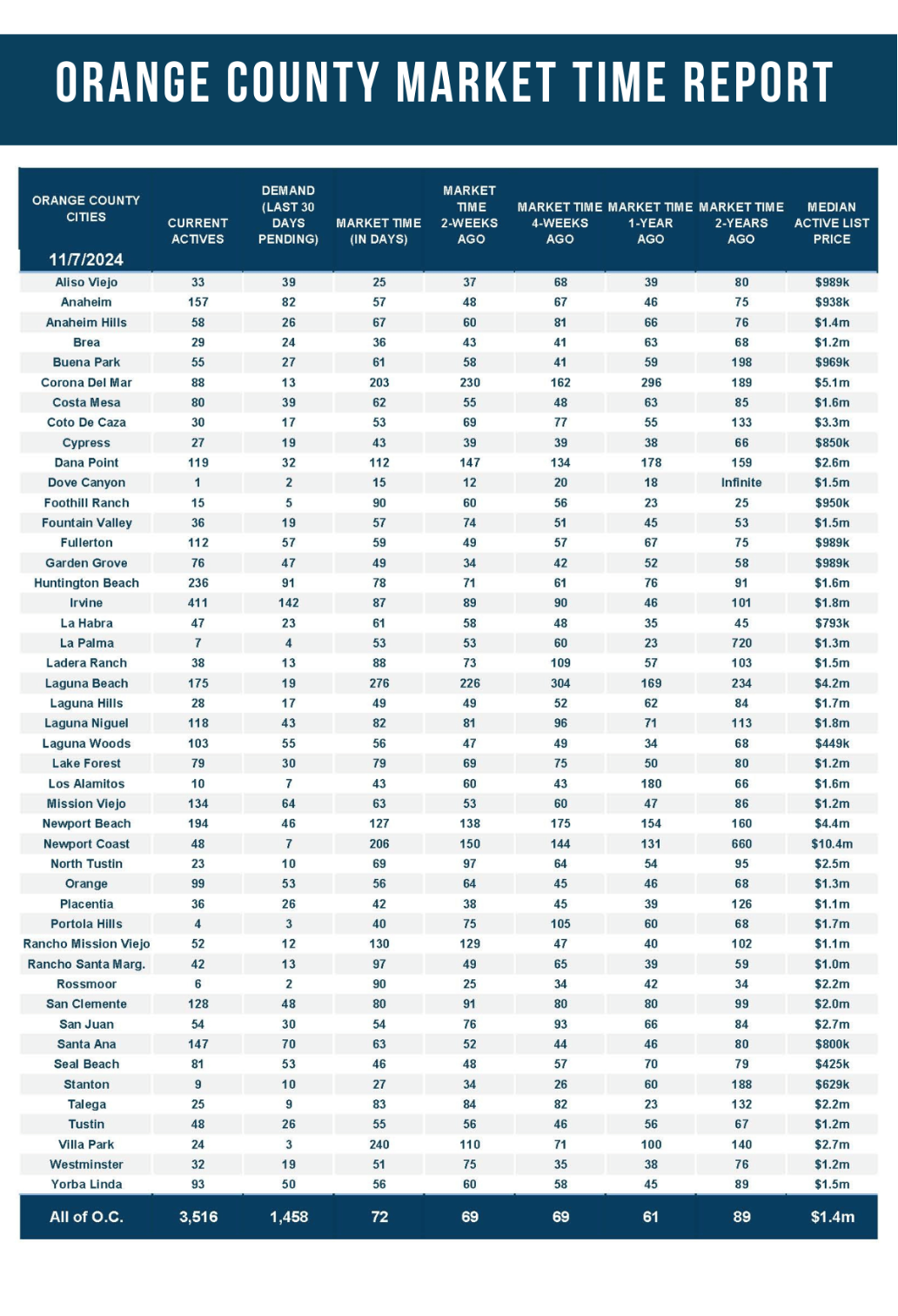

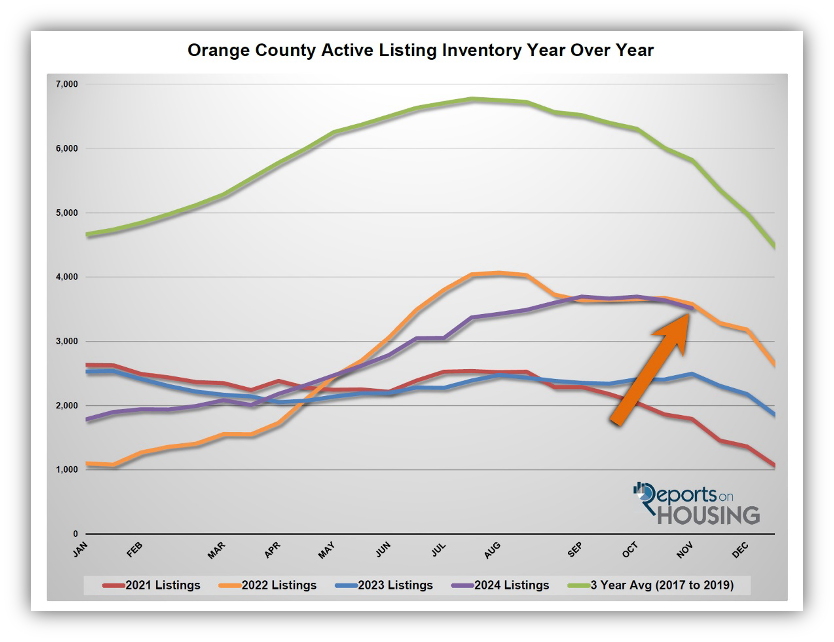

The active listing inventory decreased by 124 homes in the past two weeks, down 3%, and now sits at 3,516, its lowest level since mid-August and its largest drop of the year. The inventory peak in Orange County for 2024 occurred four weeks ago at 3,694, 48% higher than last year’s November 9th peak. Expect the inventory to continue to fall for the remainder of the year. It will fall faster starting next week, the start of the Holiday Market, just a week before Thanksgiving. The New Year will start similar to 2023, with around 2,400 homes. The three-year average start to the year before COVID (2017 to 2019) was 4,550.

Last year, the inventory was 2,496 homes, 29% lower, or 1,020 fewer. The 3-year average before COVID (2017 through 2019) was 5,822, an additional 2,306 homes, or 66% more.

Homeowners continue to “hunker down” in their homes, unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. It became a crisis once rates skyrocketed higher in 2022. For October, 2,377 new sellers entered the market in Orange County, 626 fewer than the 3-year average before COVID (2017 to 2019), 21% less. Last October, there were 1,891 new sellers, 20% fewer than this year. More sellers are opting to sell compared to the previous year.

Demand

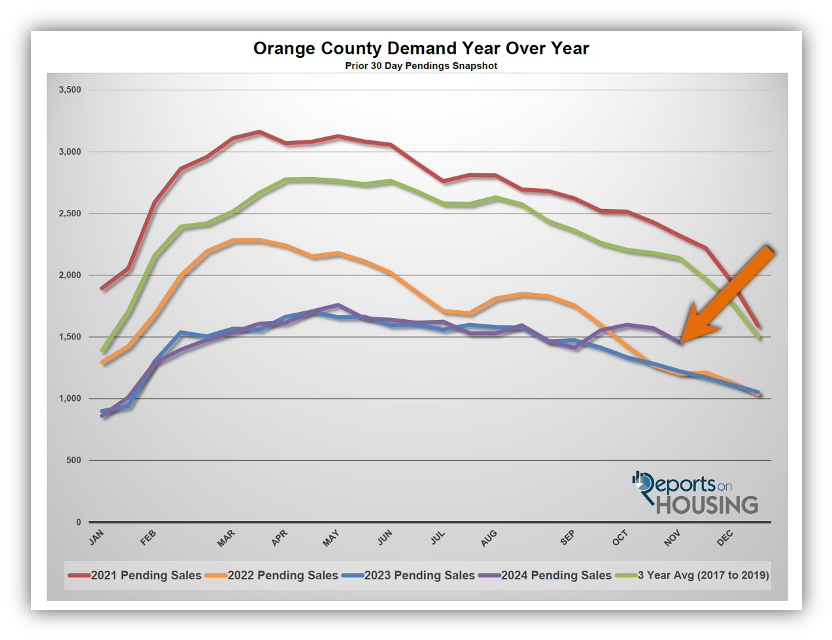

Demand plunged by 7% in the past couple of weeks.

Demand, a snapshot of the number of new pending sales over the prior month, plunged from 1,572 to 1,458 in the past couple of weeks, down 235 pending sales, or 7%. This reflects rates climbing from 6.1% in mid-September to 7.13% on November 6th, up more than 1%. This rise was due to economic readings that were stronger than expected, along with investors’ election positioning. The higher rate environment has eroded demand due to affordability issues. Rates were stuck above 7% again for 9 days. They have since retreated, falling below the 7% threshold, and currently sit at 6.92%. Expect demand to continue to fall through the end of the year. The speed of the drop totally depends upon what happens to mortgage rates from here.

As the Federal Reserve has indicated, it is essential to watch all economic releases for signs of slowing. These releases can potentially move mortgage rates higher or lower, depending on how they compare to market expectations. This week will include two different inflation prints, the Consumer Price Index (CPI) and the Producer Price Index (PPI). In addition, retail sales will be released on Friday.

Last year, demand was 1,223, down 235 pending sales or 16%. The 3-year average before COVID (2017 to 2019) was 2,139 pending sales, 47% more than today, or an additional 681.

With demand falling faster than supply, the Expected Market Time (the number of days it takes to sell all Orange County listings at the current buying pace) increased from 69 to 72 days in the past couple of weeks. Last year, it was 61 days, faster than today. The 3-year average before COVID was 85 days, slower than today.

Luxury End

The luxury market slowed in the past couple of weeks.

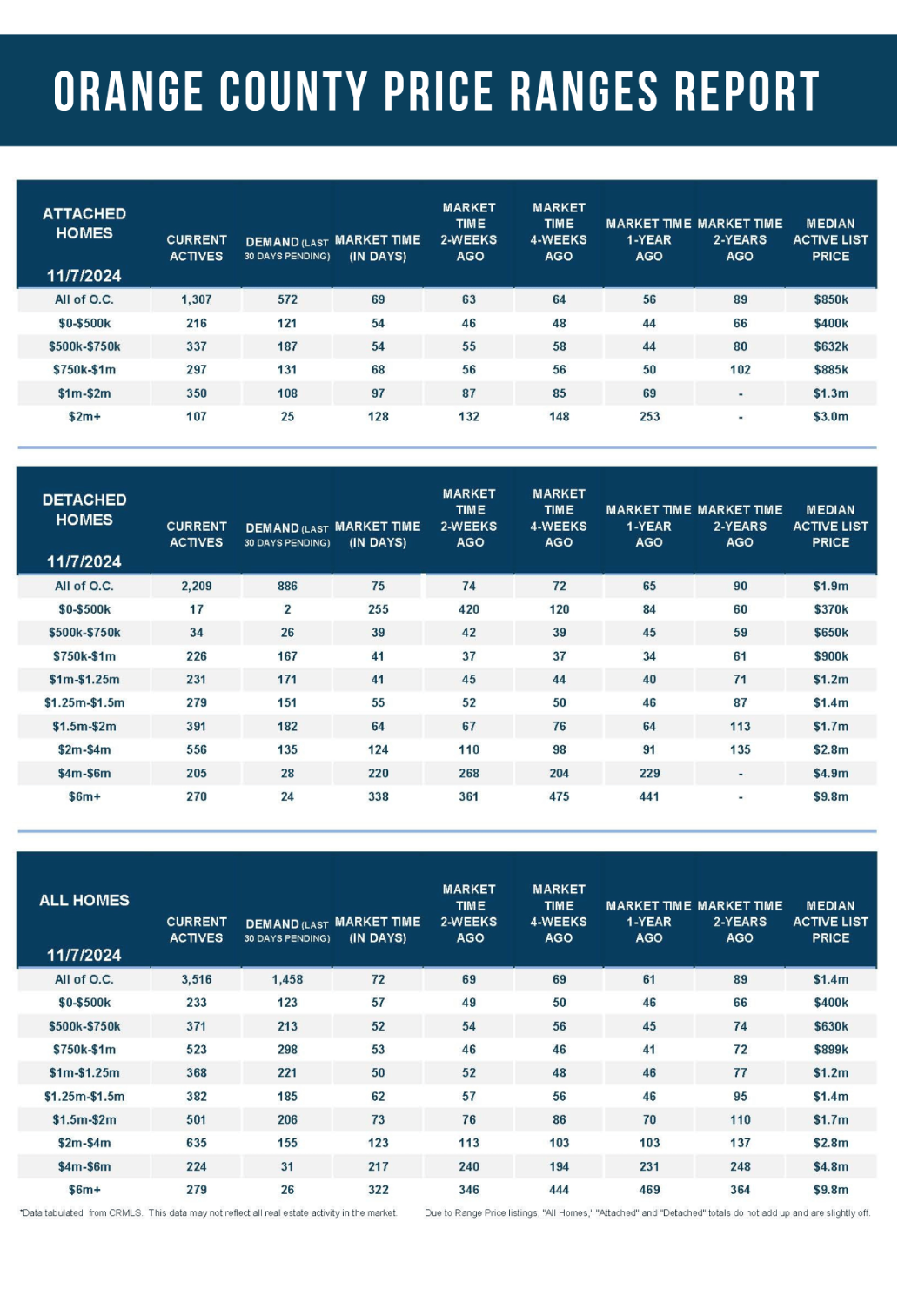

In the past couple of weeks, the luxury inventory of homes priced above $2 million (the top 10% of the Orange County housing market) decreased from 1,177 to 1,138 homes, down 39 or 3%. Luxury demand decreased by 16 pending sales, down 7%, and now sits at 212, its lowest reading since February. With demand dropping faster than supply, the Expected Market Time for luxury homes priced above $2 million increased from 155 to 161 days, its highest reading since the first week of January. The luxury market is sluggish and necessitates a careful, methodical approach to pricing.

Year over year, the active luxury inventory is up by 319 homes or 39%, and luxury demand is up by 50 pending sales or 31%. Last year’s Expected Market Time was 152 days, similar to today.

In the past two weeks, the expected market time for homes priced between $2 million and $4 million increased from 113 to 123 days. For homes priced between $4 million and $6 million, the Expected Market Time decreased from 240 to 217 days. For homes priced above $6 million, the Expected Market Time decreased from 346 to 322 days. At 346 days, a seller would be looking at placing their home into escrow around September 2025.

Orange County Housing Summary

- The active listing inventory in the past couple of weeks decreased by 124 homes, down 3%, and now sits at 3,516, its lowest level since mid-August and its largest drop of the year. Orange County reached its annual peak at 3,694 homes four weeks ago. In October, 21% fewer homes came on the market compared to the 3-year average before COVID (2017 to 2019), 743 less. Yet, 486 more sellers came on the market this September compared to September 2023. Last year, there were 2,496 homes on the market, 1,020 fewer homes, or 29% less. The 3-year average before COVID (2017 to 2019) was 5,822, or 66% extra.

- Demand, the number of pending sales over the prior month, decreased by 114 pending sales in the past two weeks, down 7%, and now totals 1,458. Last year, there were 1,223 pending sales, 16% fewer. The 3-year average before COVID (2017 to 2019) was 2,139, or 47% more.

- With demand falling faster than supply, the Expected Market Time, the number of days to sell all Orange County listings at the current buying pace, increased from 69 to 72 days in the past couple of weeks. The 3-year average before COVID (2017 to 2019) was 85 days, slower than today.

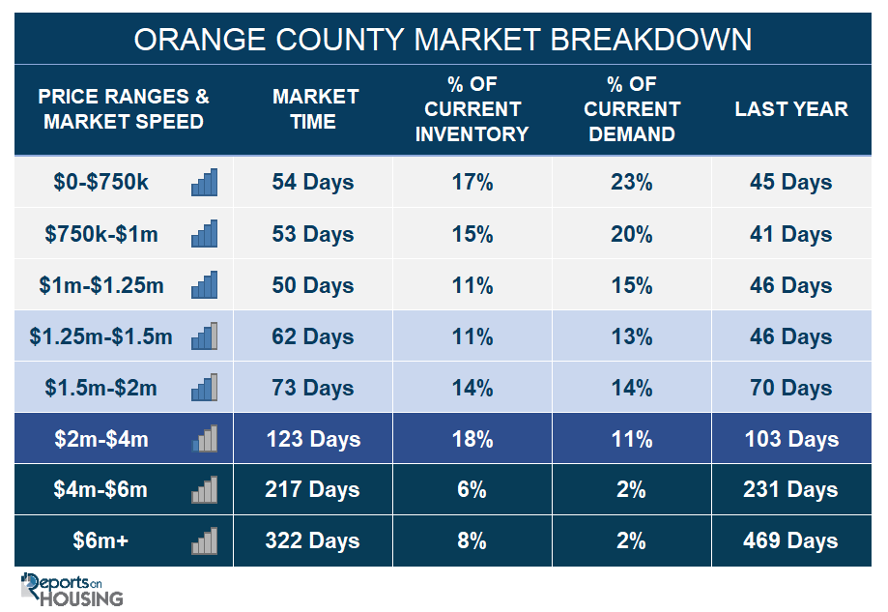

- In the past two weeks, the Expected Market Time for homes priced below $750,000 increased from 52 to 54 days. This range represents 17% of the active inventory and 23% of demand.

- The Expected Market Time for homes priced between $750,000 and $1 million increased from 46 to 53 days. This range represents 15% of the active inventory and 20% of demand.

- The Expected Market Time for homes priced between $1 million and $1.25 million decreased from 52 to 50 days. This range represents 11% of the active inventory and 15% of demand.

- The Expected Market Time for homes priced between $1.25 million and $1.5 million increased from 57 to 62 days. This range represents 11% of the active inventory and 13% of demand.

- The Expected Market Time for homes priced between $1.5 million and $2 million decreased from 76 to 73 days. This range represents 14% of the active inventory and 14% of demand.

- In the past two weeks, the expected market time for homes priced between $2 million and $4 million increased from 113 to 123 days. For homes priced between $4 million and $6 million, the Expected Market Time decreased from 240 to 217 days. For homes priced above $6 million, the Expected Market Time decreased from 346 to 322 days.

- The luxury end, all homes above $2 million, account for 32% of the inventory and 15% of demand.

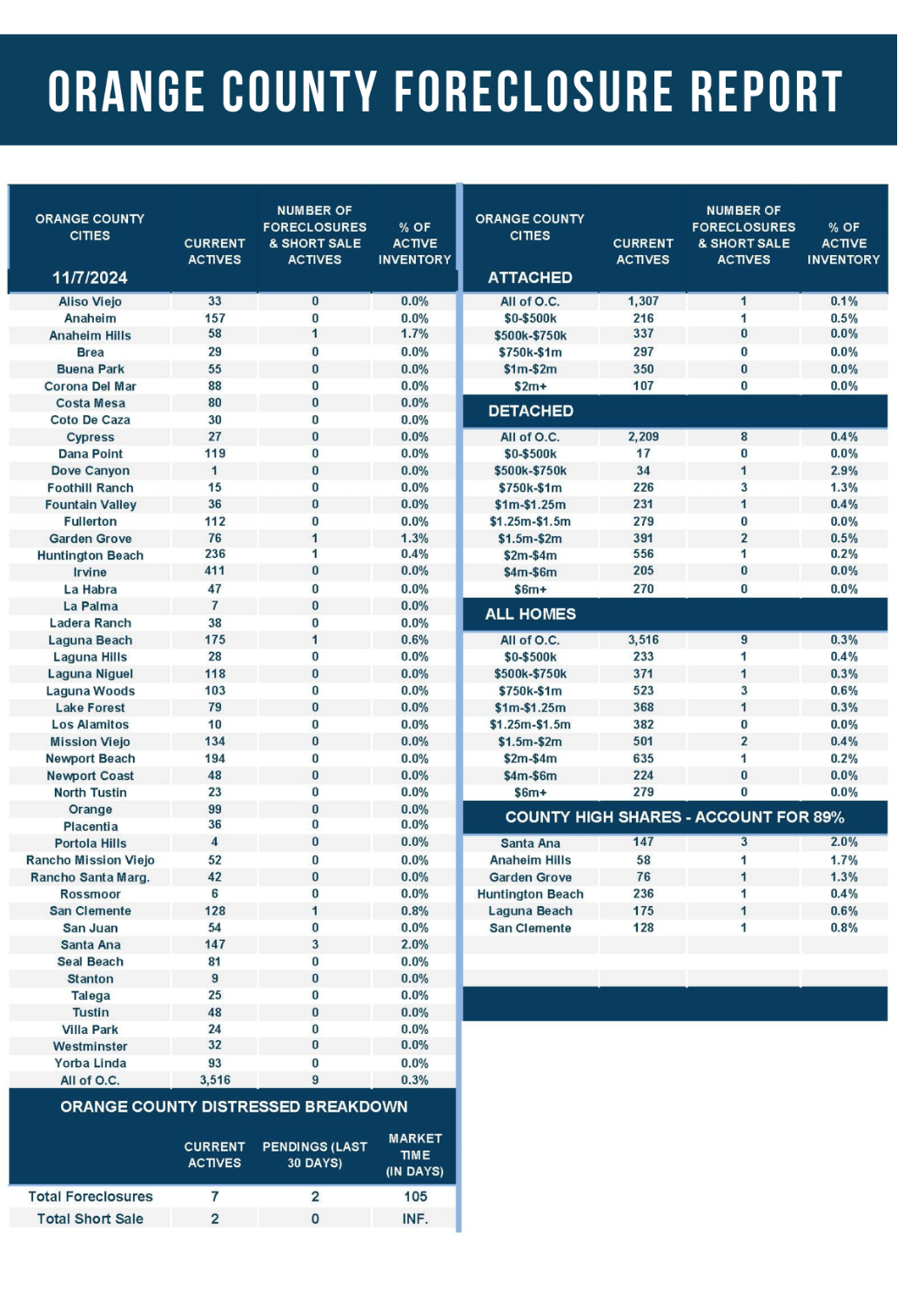

- Distressed homes, both short sales and foreclosures combined, comprised only 0.3% of all listings and 0.1% of demand. Only seven foreclosures and two short sales are available today in Orange County, with nine total distressed homes on the active market, up two from two weeks ago. Last year, six distressed homes were on the market, similar to today.

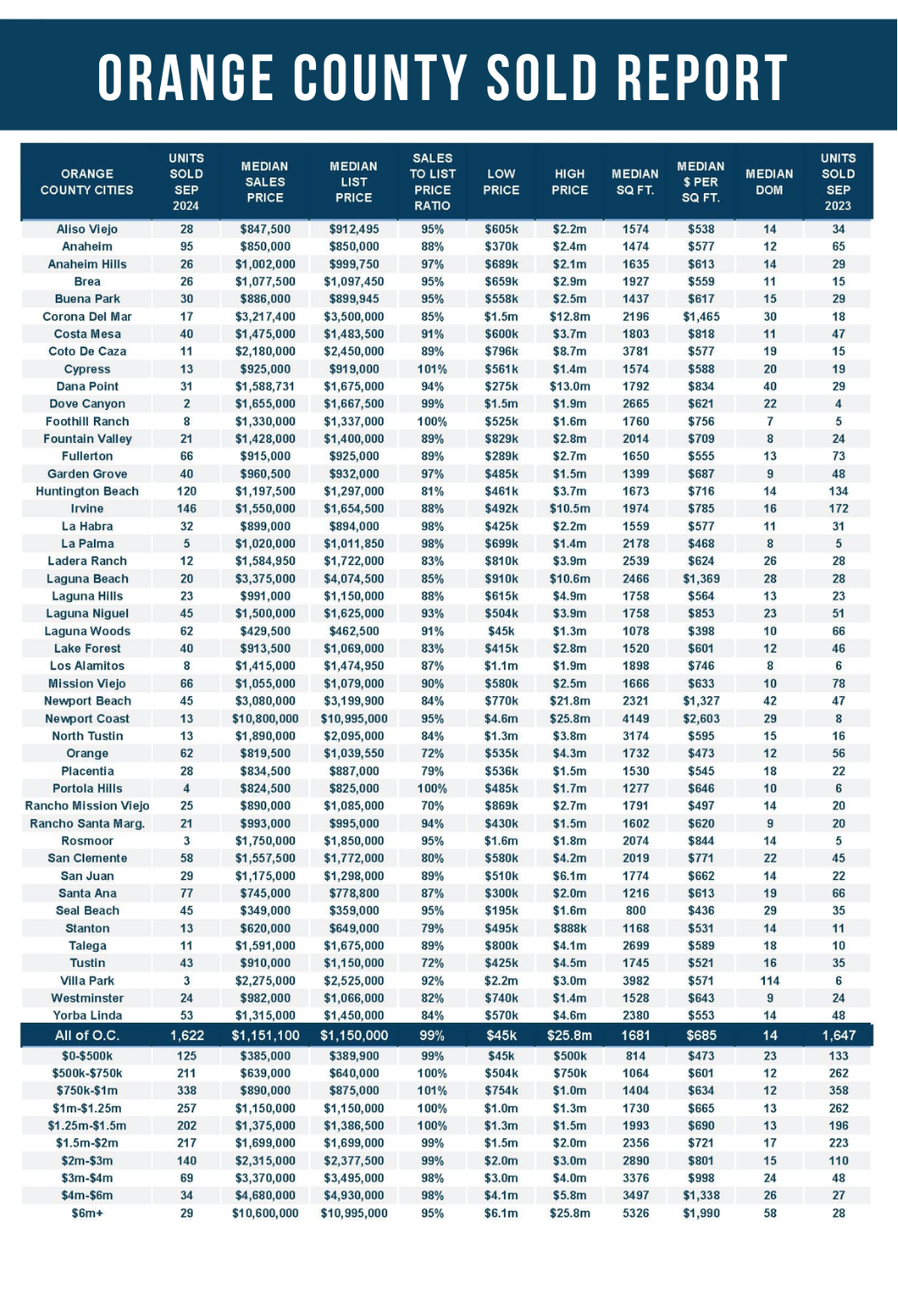

- There were 1,622 closed residential resales in September, down 2% compared to September 2023’s 1,647 and down 14% from August 2024. The sales-to-list price ratio was 98.9% for Orange County. Foreclosures accounted for 0.1% of all closed sales, and there were no short sales. That means that 99.9% of all sales were good ol’ fashioned sellers with equity.

Have a great week.

Sincerely,

Steven Thomas

Quantitative Economics and Decision Sciences

Copyright 2024—Steven Thomas, Reports On Housing—All Rights Reserved. This report may not be reproduced in whole or in part without express written permission from the author.